1/n Alright, so what happened at this track yesterday that was so interesting? I'll try and summarize in this thread.

2/n Just for reference, if you have no idea what this is about and want to read up, this thread might help. If you speak Dutch, the @BitcoinMagNL article in my pinned tweet does the trick as well.

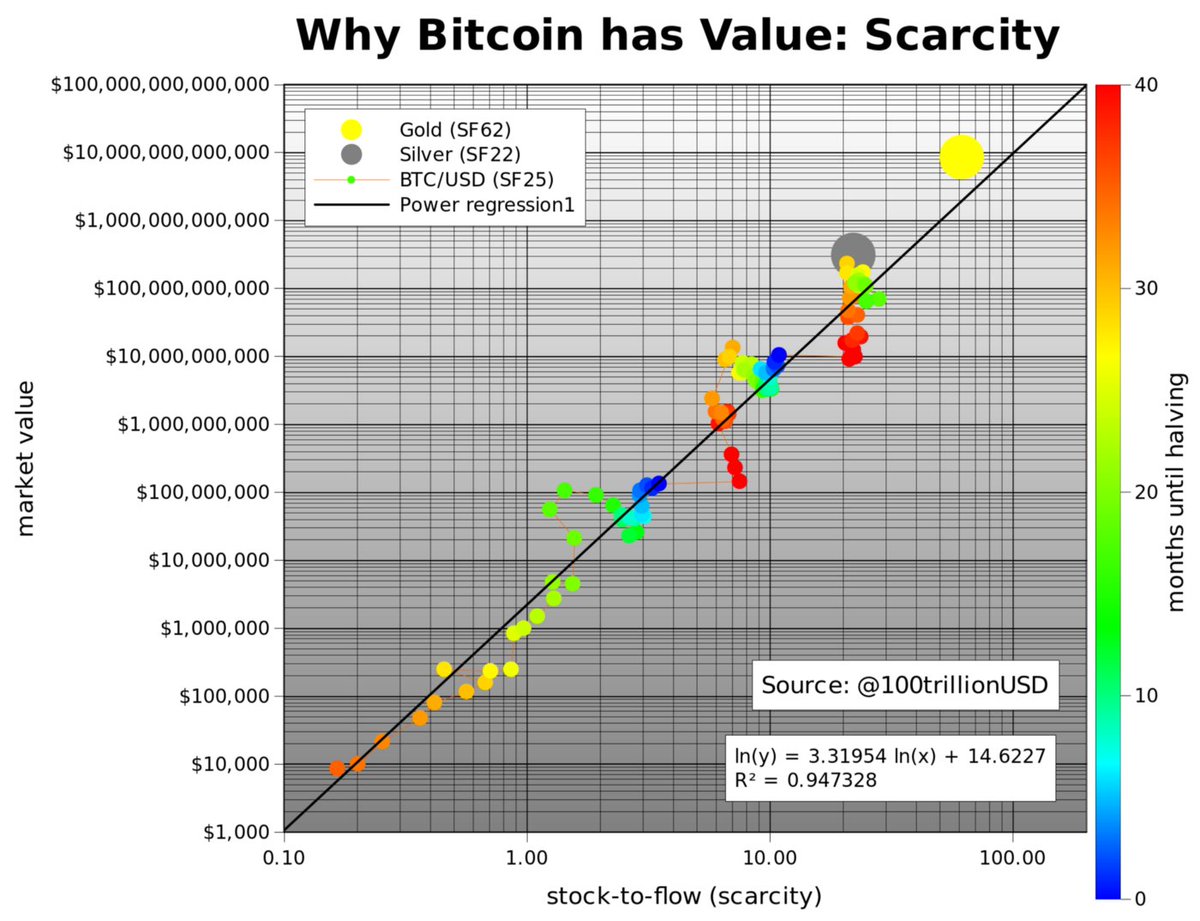

3/n After @moneymanolis gave an explanation of the fundamentals behind the #Bitcoin S2F model, @Kripfganz took the @ValueOfBitcoin stage.

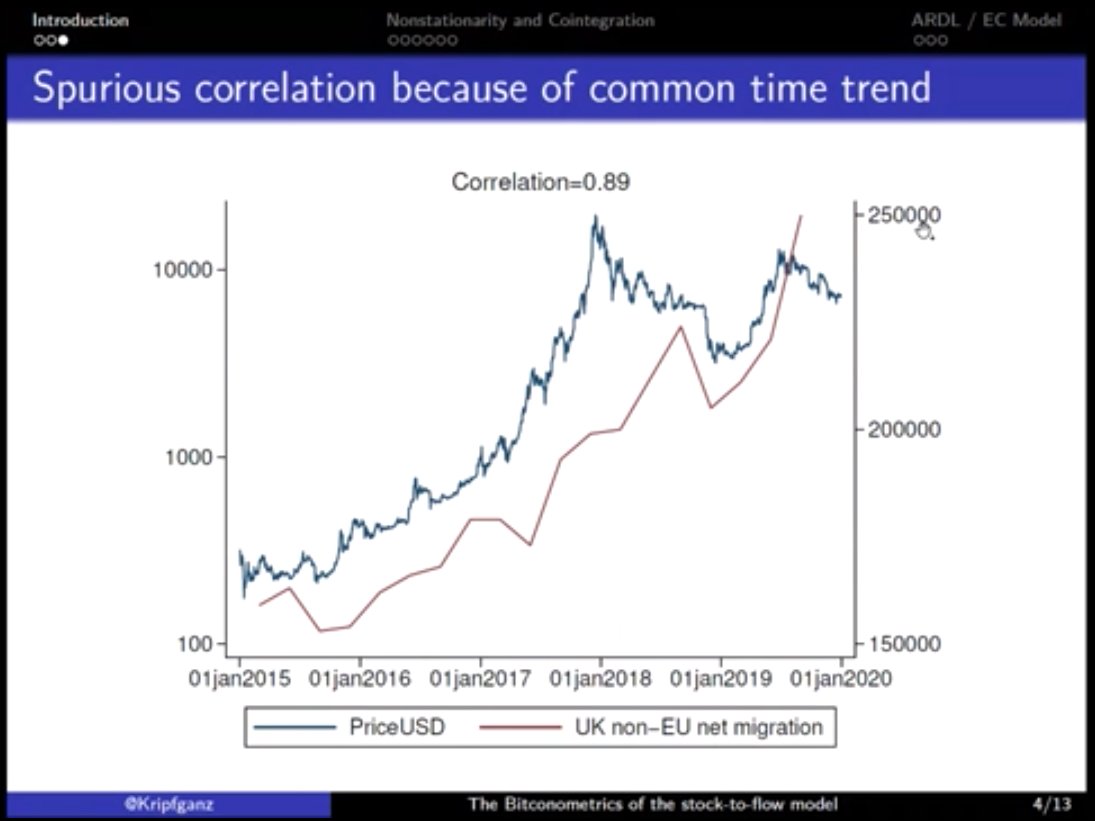

One of the first things he did was give an example of a spurious regression: Bitcoin is correlated (r=.89) with UK non-EU net migration! 😄

One of the first things he did was give an example of a spurious regression: Bitcoin is correlated (r=.89) with UK non-EU net migration! 😄

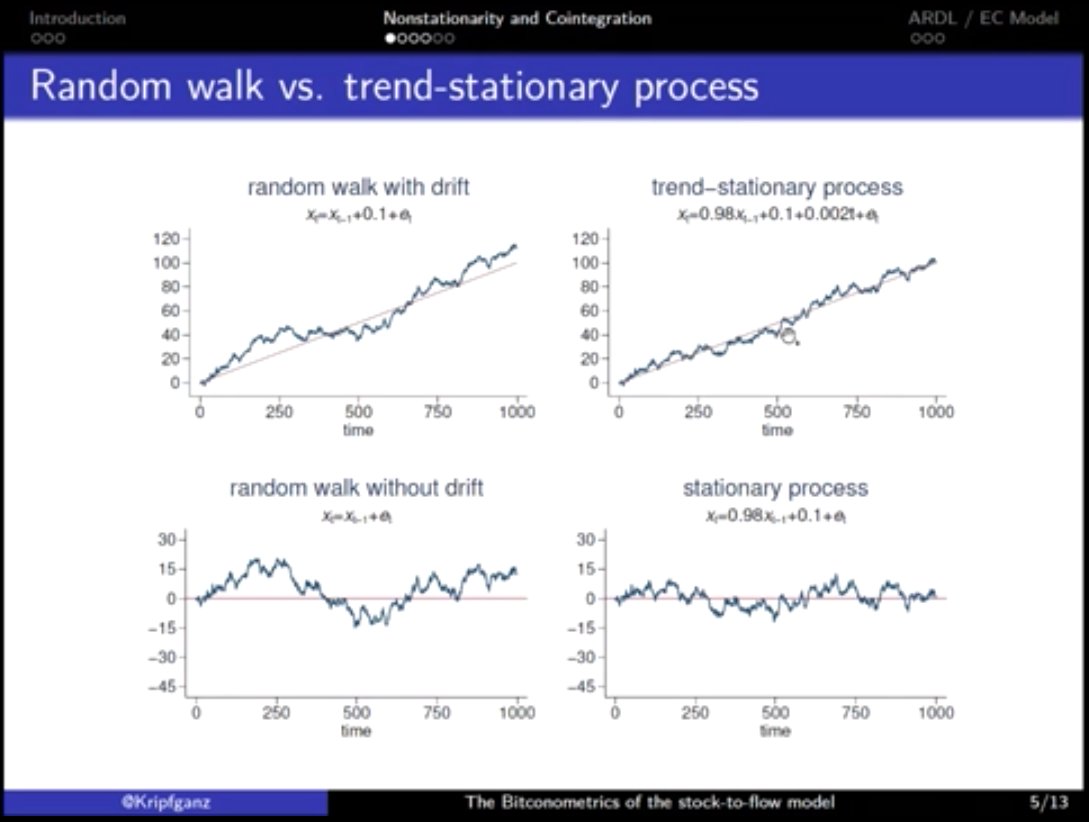

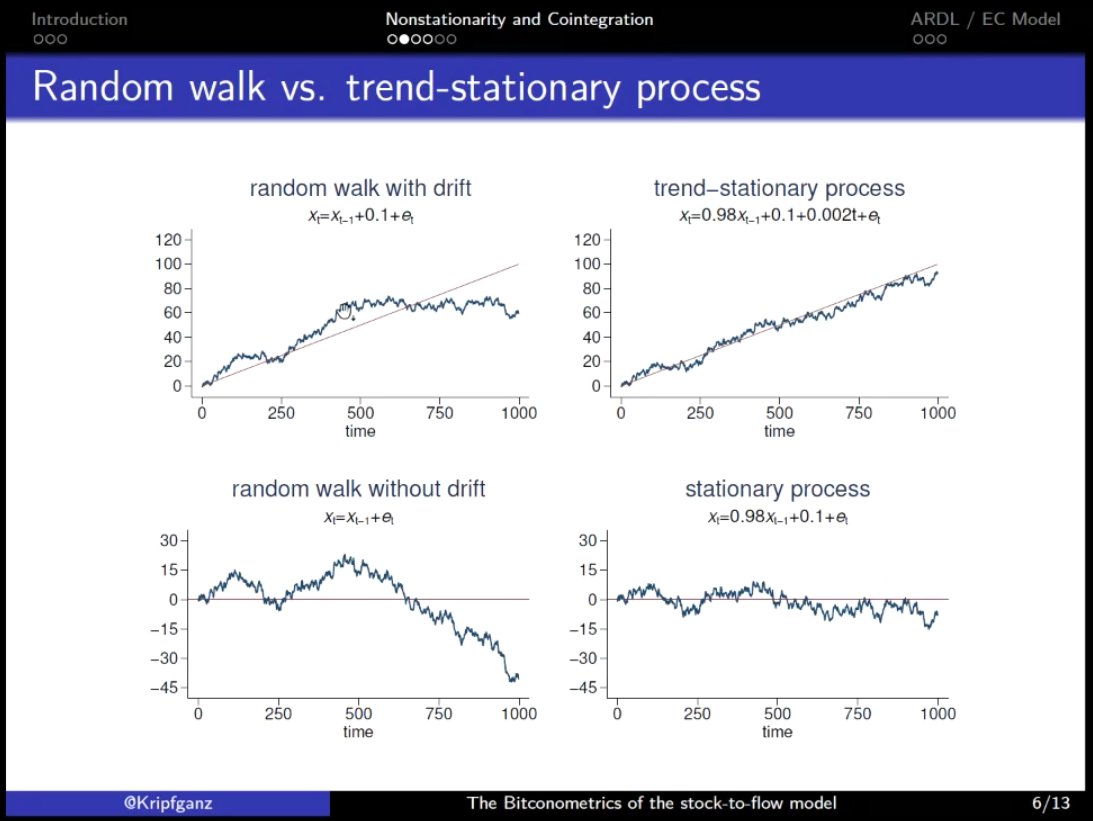

4/n Since #Bitcoin price & S2F are time series, you need to look at the time series' properties before doing further analysis.

@Kripfganz showed examples of time series that are not stationary (random walks) & some that are.

The key question; which of these applies to Bitcoin?

@Kripfganz showed examples of time series that are not stationary (random walks) & some that are.

The key question; which of these applies to Bitcoin?

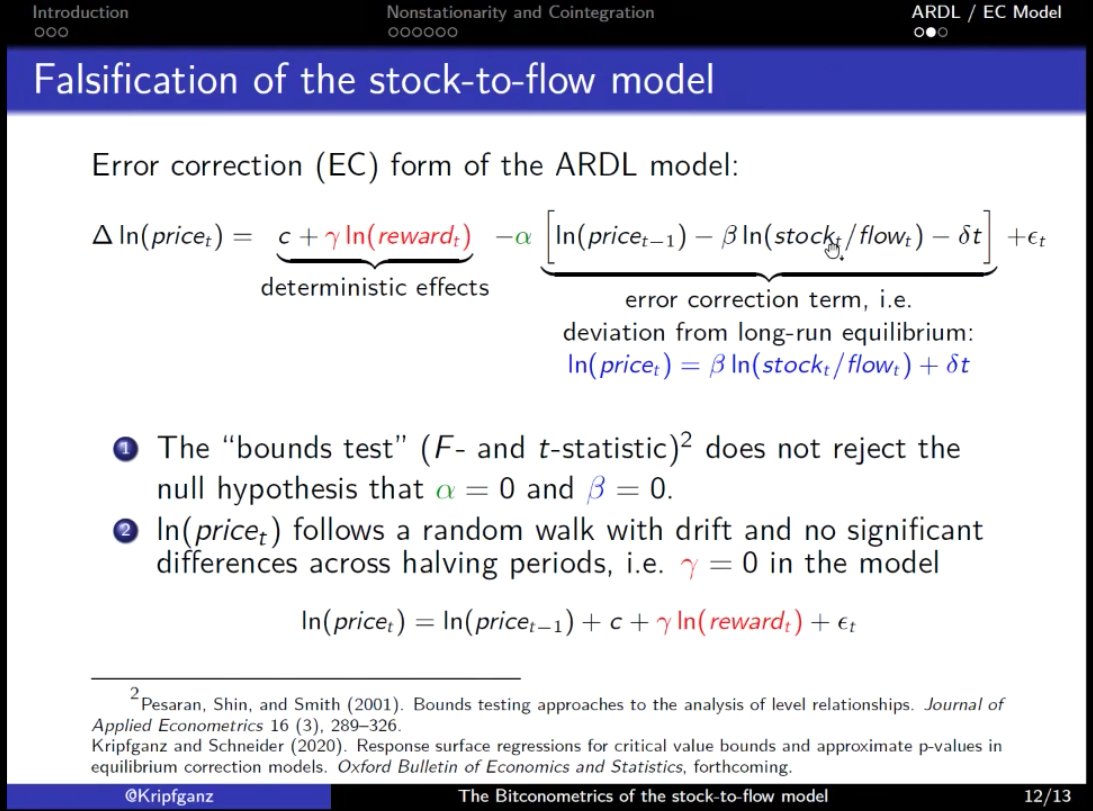

5/n Like @btconometrics did in his March 27th article, @Kripfganz used an ARDL model.

His conclusion: the (log) #Bitcoin price follows a random walk with drift (top left figures in the previous tweet) and has no significant differences across halving periods.

His conclusion: the (log) #Bitcoin price follows a random walk with drift (top left figures in the previous tweet) and has no significant differences across halving periods.

6/n These findings imply that there is no cointegration between the #Bitcoin price and S2F ratio like we thought before, and that while the price drifts upwards, the time series is basically a random walk, which means it could go anywhere.

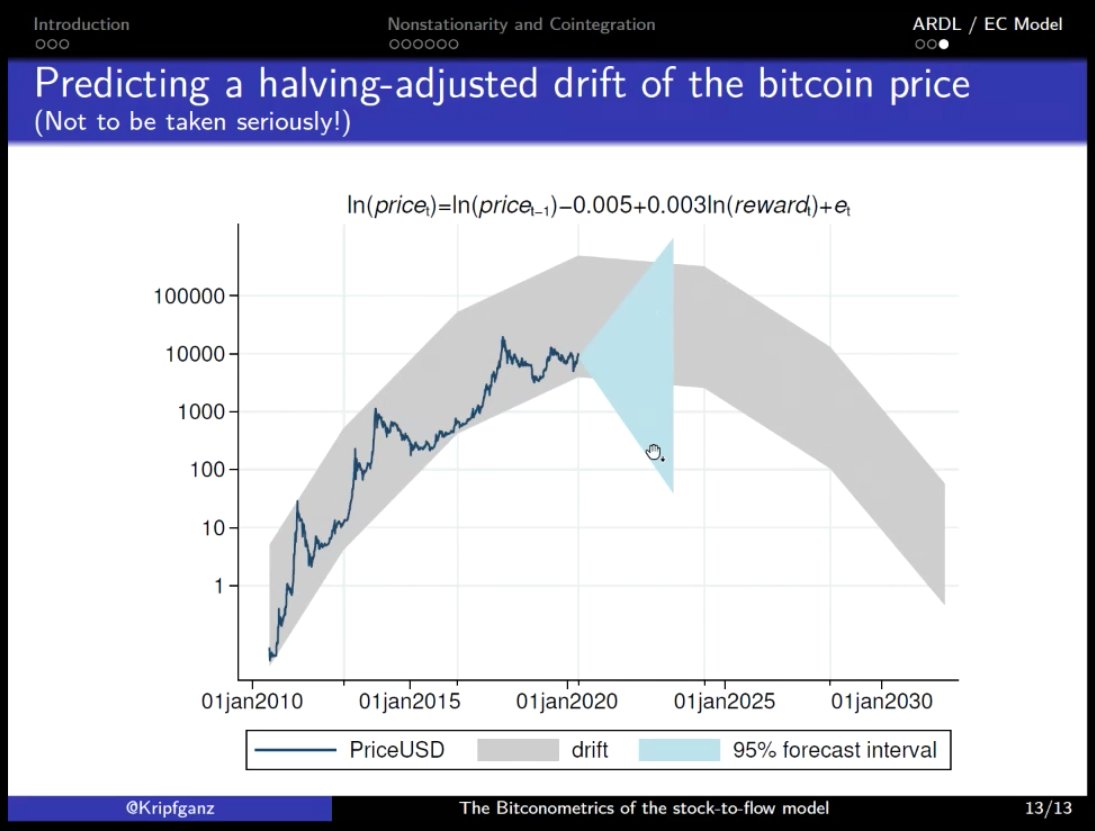

7/n To illustrate the point that the #Bitcoin price can go anywhere, @Kripfganz introduced (with playful banter) what I'd like to call the 'Grey Rainbow of Doom'.

This graph puts the 🌈-chart by @ercwl & @rohmeo_de in a different light! 😅

I guess there's always a bigger fish.

This graph puts the 🌈-chart by @ercwl & @rohmeo_de in a different light! 😅

I guess there's always a bigger fish.

8/n So what does this mean for @100trillionUSD's S2F model?

@Kripfganz's findings not only imply that there is no cointegration between #Bitcoin price & S2F ratio, but also that these time series should not be used to predict the future Bitcoin price, as it could go anywhere.

@Kripfganz's findings not only imply that there is no cointegration between #Bitcoin price & S2F ratio, but also that these time series should not be used to predict the future Bitcoin price, as it could go anywhere.

9/n However, is that true? If the magic behind 'number go up' wasn't captured in these models it could mean that there's a driver of price that could not (yet) be quantified.

If all model's are thrown in the 🗑️, there's always praxeology to fall back on.

If all model's are thrown in the 🗑️, there's always praxeology to fall back on.

10/n Right now it seems like the last glimmer of hope for these time series models lies with @BurgerCryptoAM, who is still chewing on @Kripfganz's results and said to be working on a new article. Although even Marcel seems to lean toward 'falsified'.

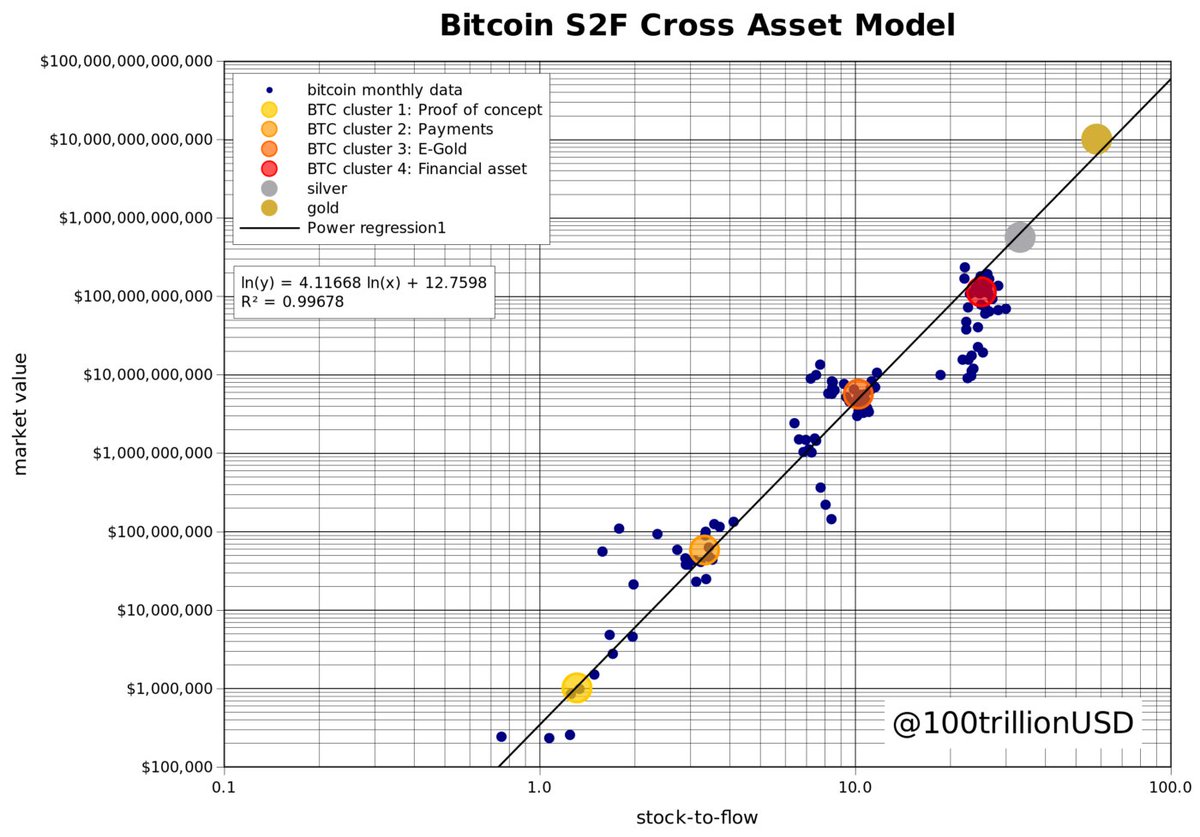

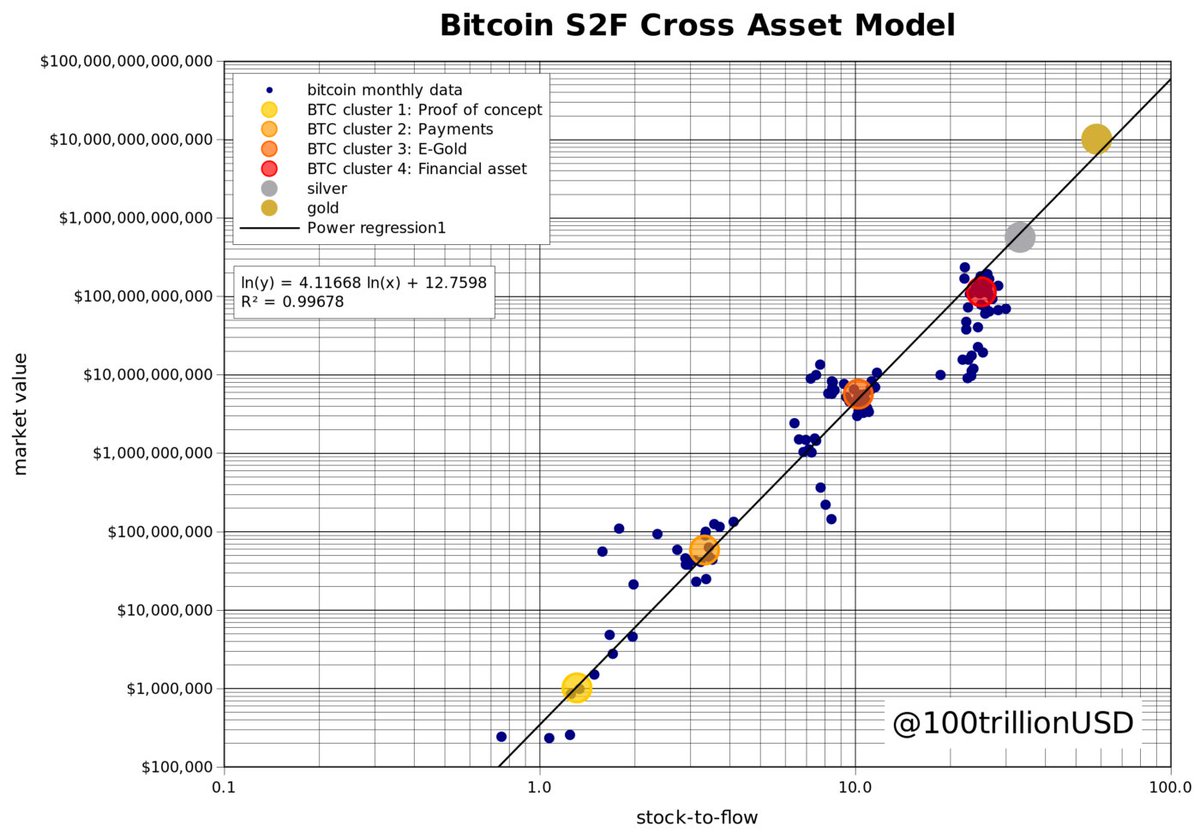

11/n There's still @100trillionUSD's #Bitcoin S2FX (cross asset) model; which is NOT a time series.

The @ValueOfBitcoin S2F-panelists seemed to agree that it is conceptually interesting, but 6 datapoints is too little. @ercwl also questioned the used gold & silver datapoints.

The @ValueOfBitcoin S2F-panelists seemed to agree that it is conceptually interesting, but 6 datapoints is too little. @ercwl also questioned the used gold & silver datapoints.

12/n @btconometrics showed that using just 6 datapoints at least introduces uncertainties in the interval of the price predictions, which becomes very wide.

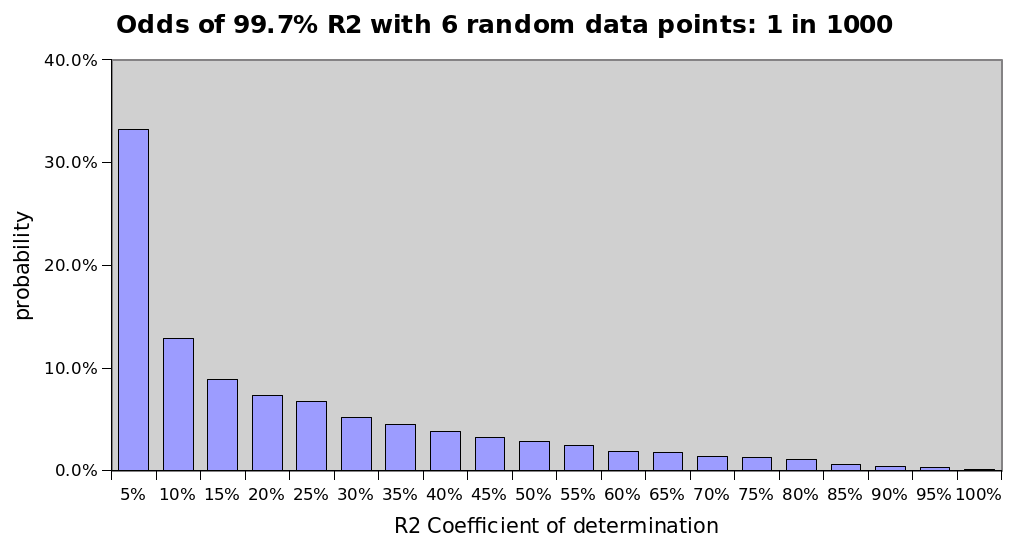

13/n @100trillionUSD also showed that accidentally finding 6 datapoints that align well enough to find an R-squared of 0.997 (which means that the model explains 99.7% of the variance between these datapoints) is at least very unlikely.

14/n Until the S2FX model is expanded upon by adding more assets, it looks like most of the discussions will be about 'are 6 datapoints enough?' for now.

Could this be a case of 'where's smoke, there's fire'?

Or, as @btconometrics put it:

Could this be a case of 'where's smoke, there's fire'?

Or, as @btconometrics put it: