Was the fortnight of Indian monsoons a harbinger of hope for the Indian economy? Check out our latest edition of Macroeconomics of India Series with @tulsipriya_rk #macroIndiaupdate #EconTwitter

Tentative real activity stabilisation amid re-emerging state lockdowns and monsoons

Tentative real activity stabilisation amid re-emerging state lockdowns and monsoons

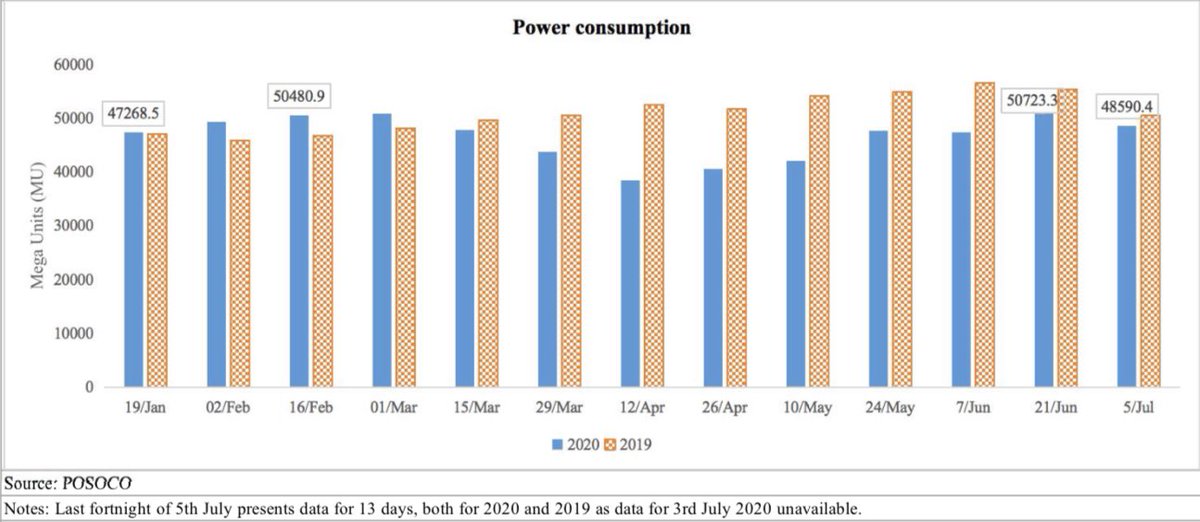

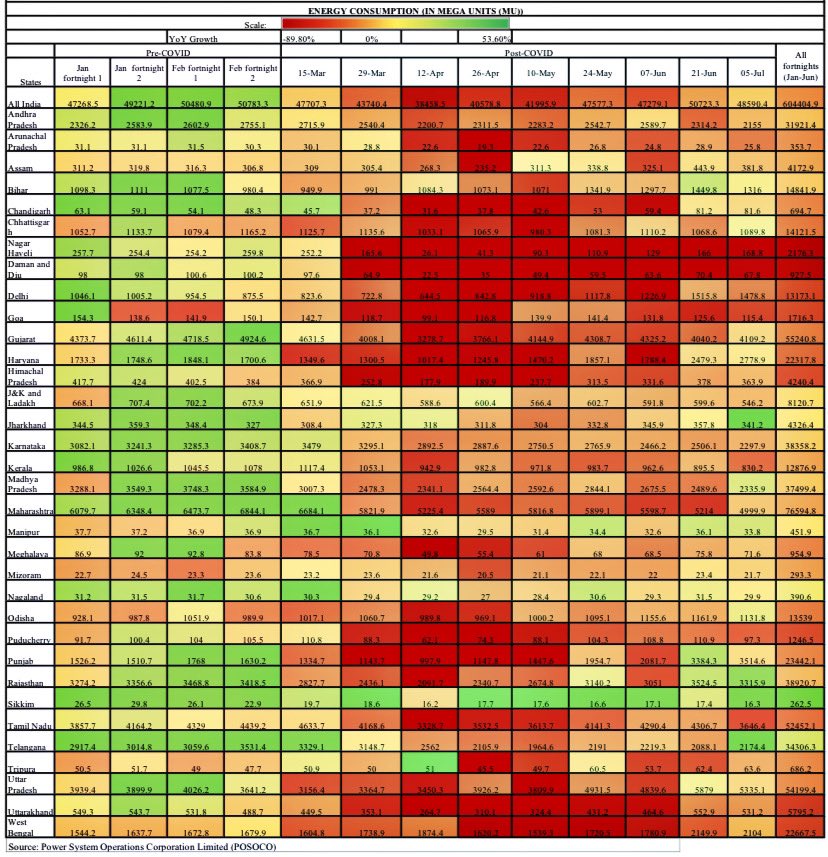

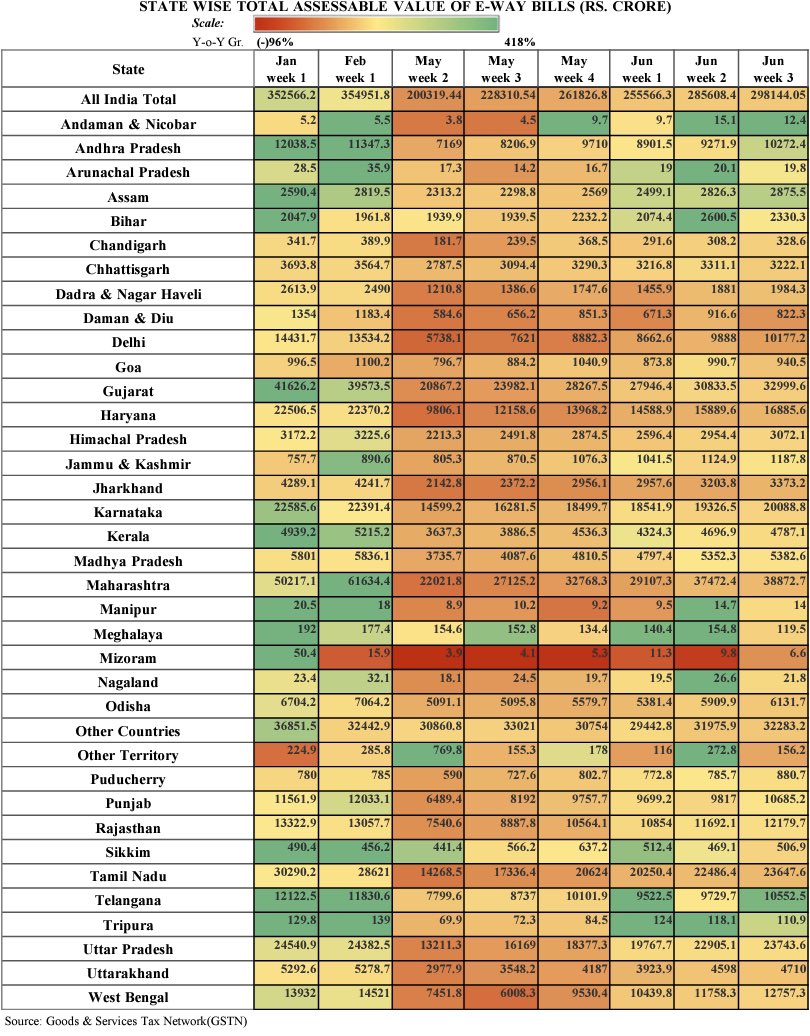

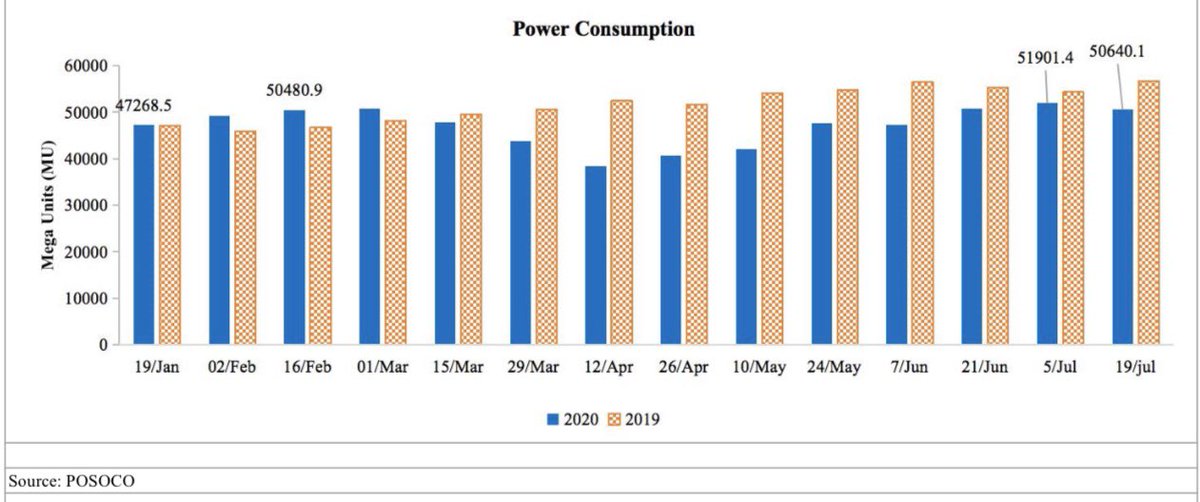

Indian recovery= States recovery Power consumption drops amid monsoon and re-imposition of lockdowns in TN, KA, JH, AS, WB and MZ @tulsipriya_rk

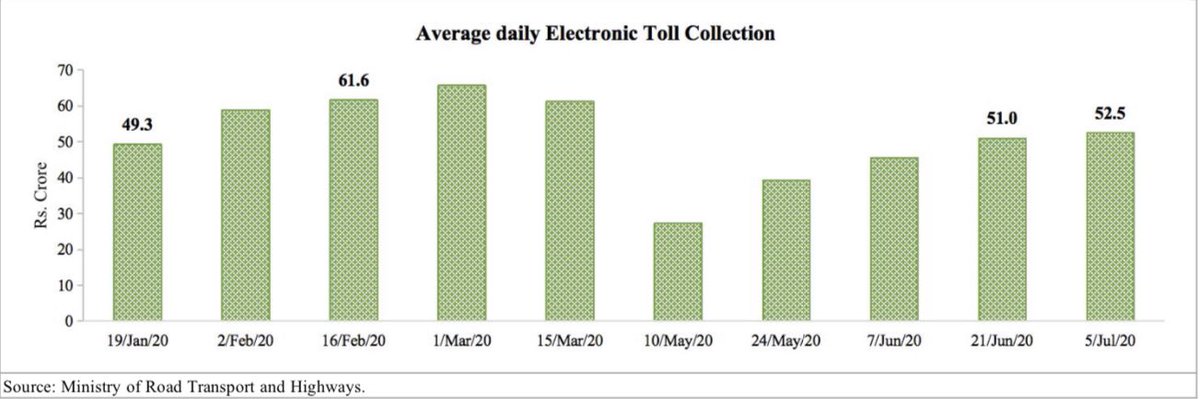

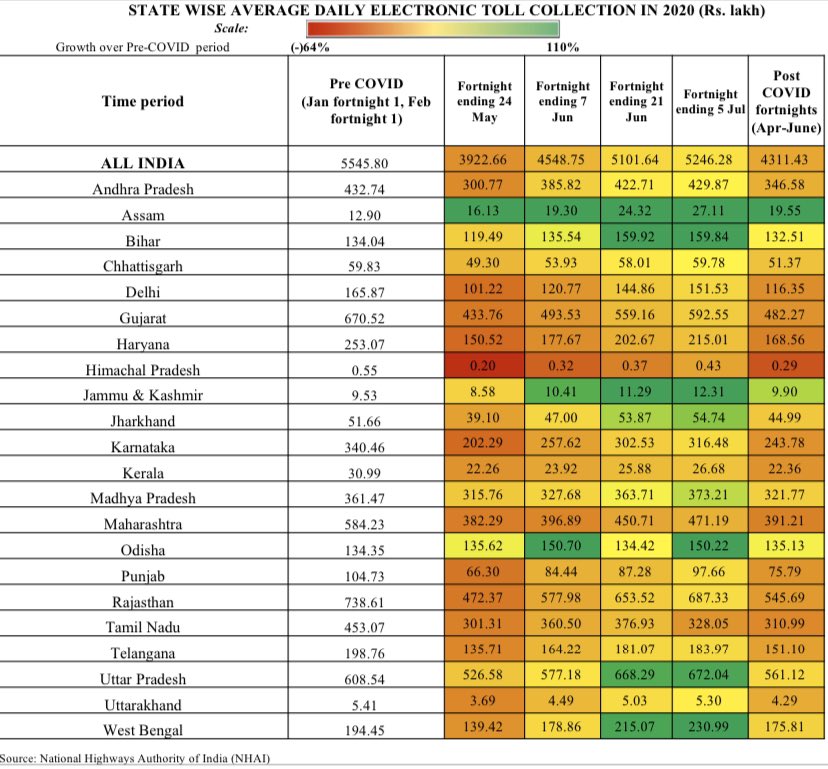

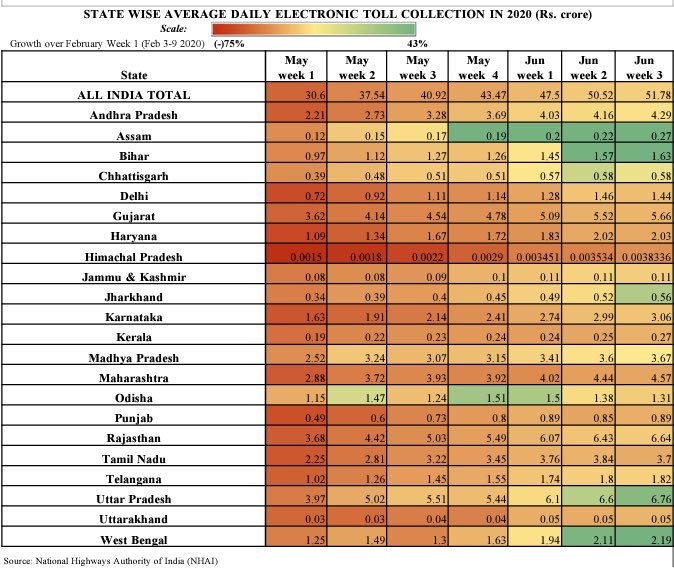

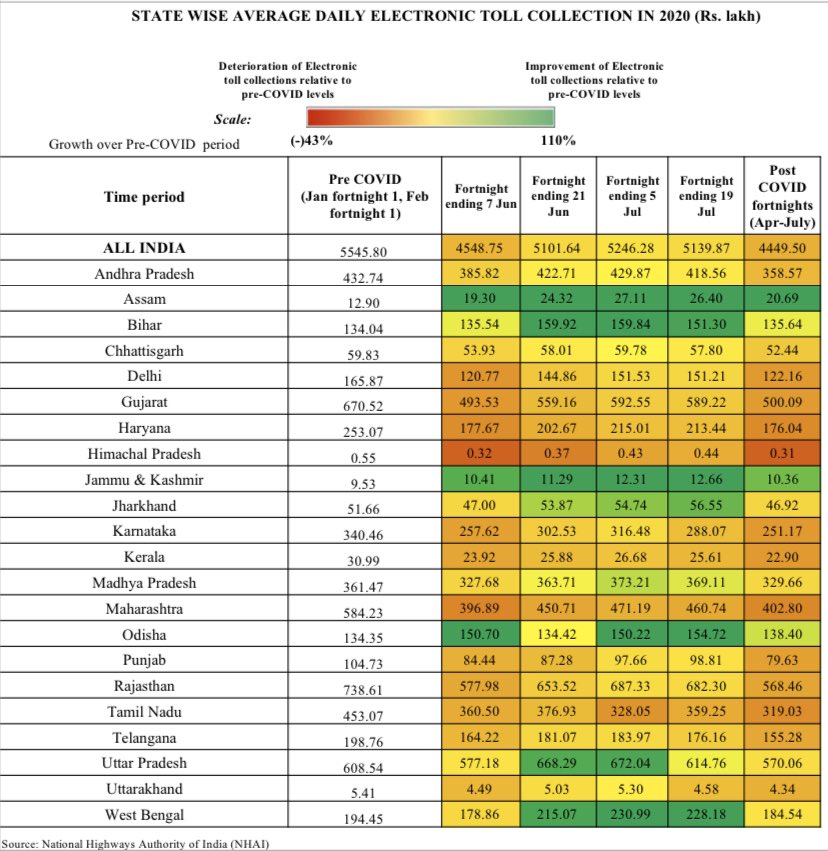

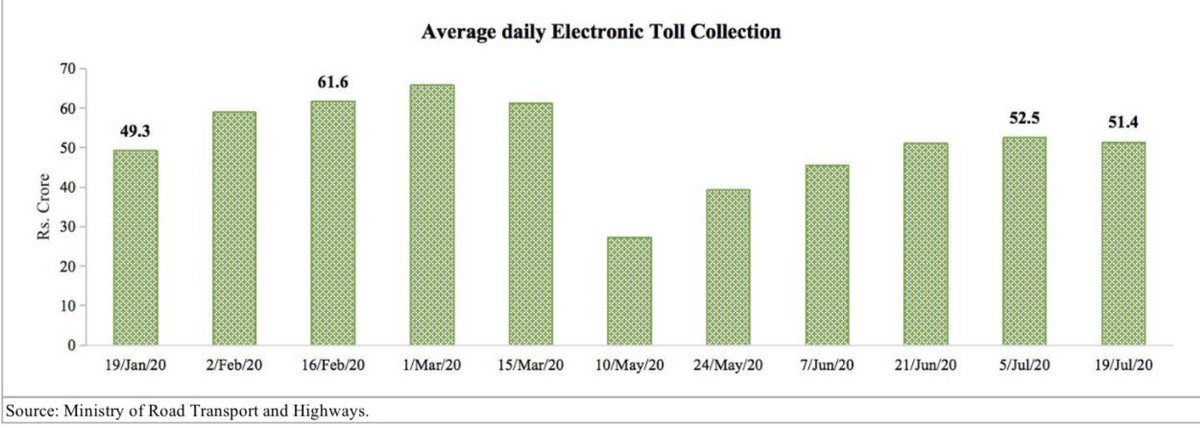

Moderation in Electronic toll collections compared to pre-COVID levels. Persistent improvement seen only in BHR, AS, J&K, OD and WB. @tulsipriya_rk

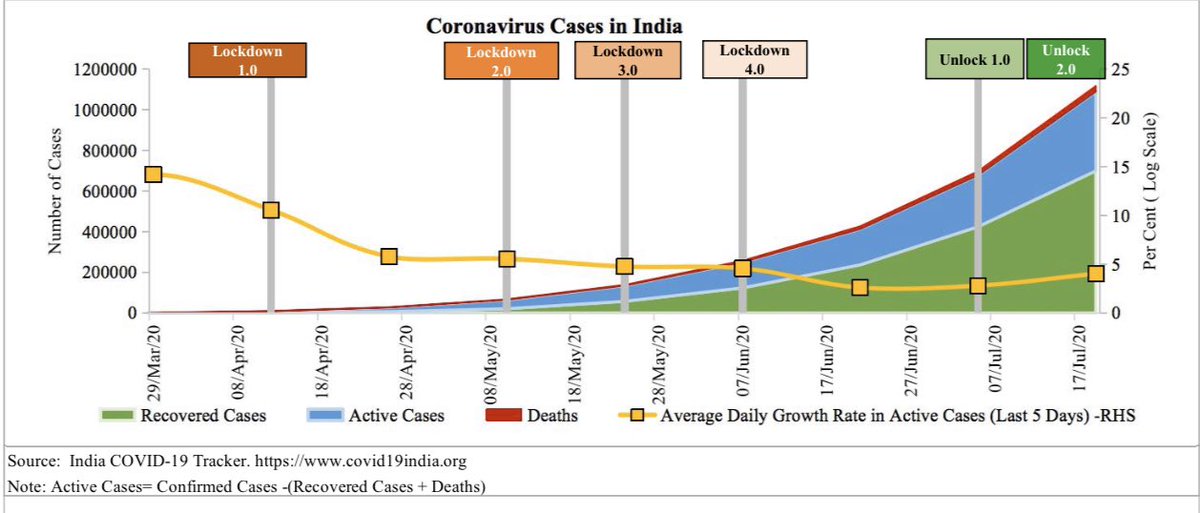

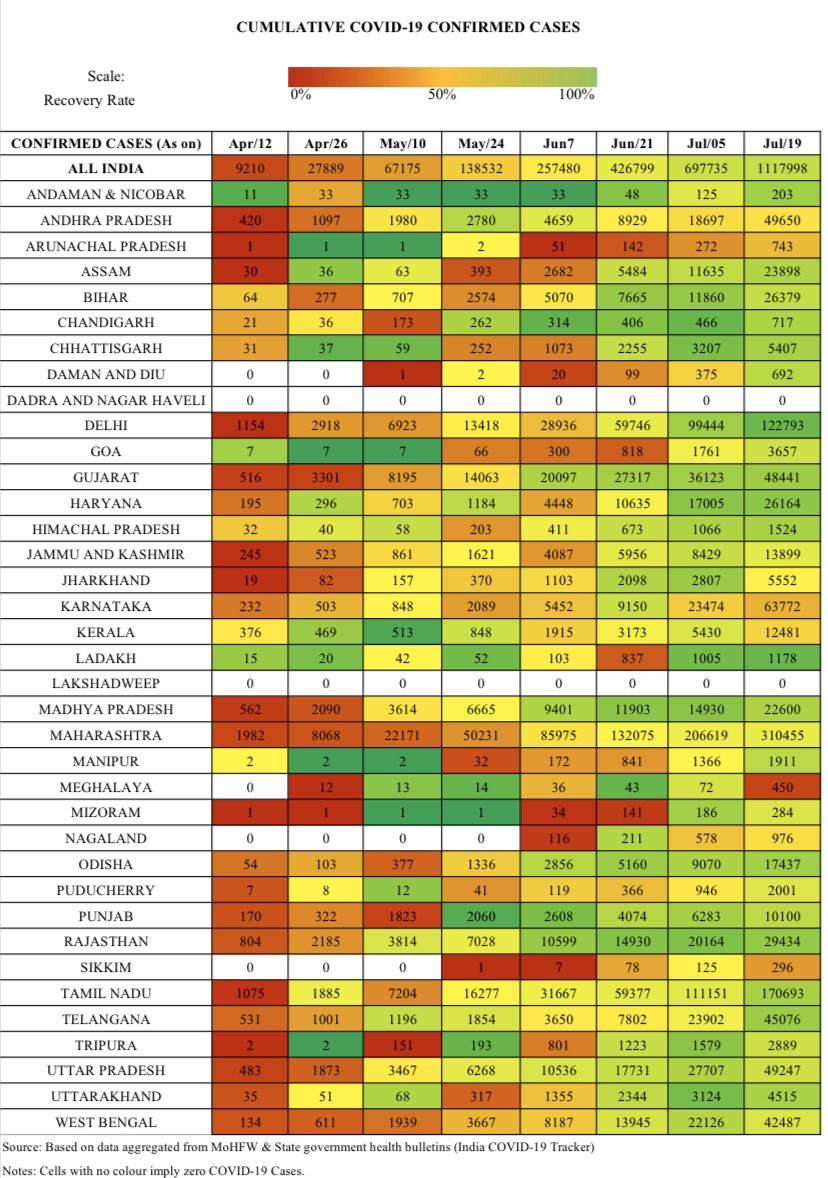

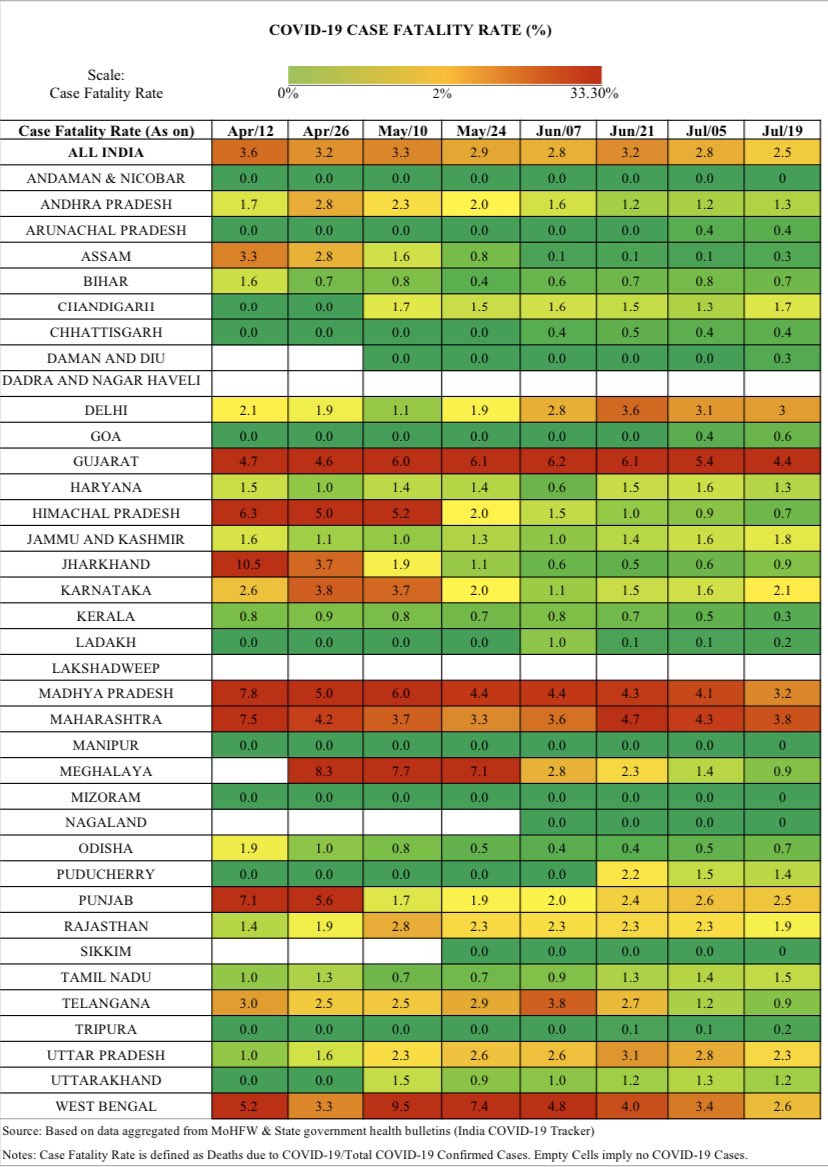

Indian economy unlocking and re-locking. Growth in active cases rose to 4% in fortnight ending 19th July compared to 2.8% in previous fortnight. Some good news-Recovery rate, high and improving- particularly in DL, HR, RJ, GJ and TS. Death rate goes below 2.5%. @tulsipriya_rk

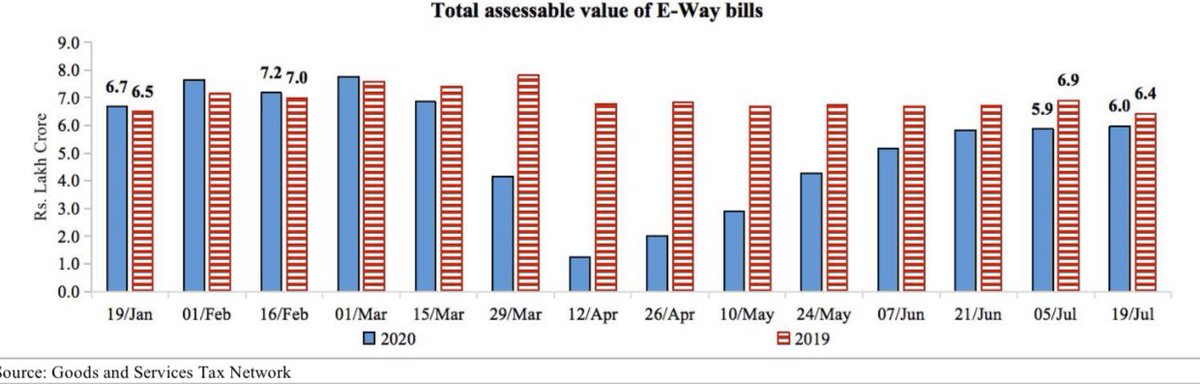

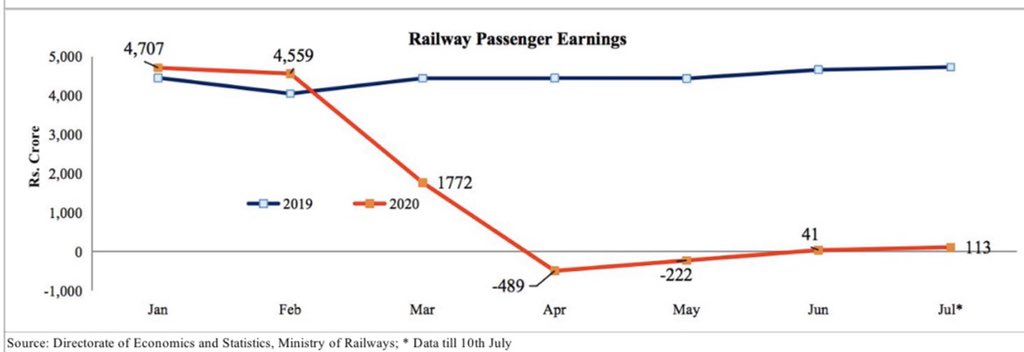

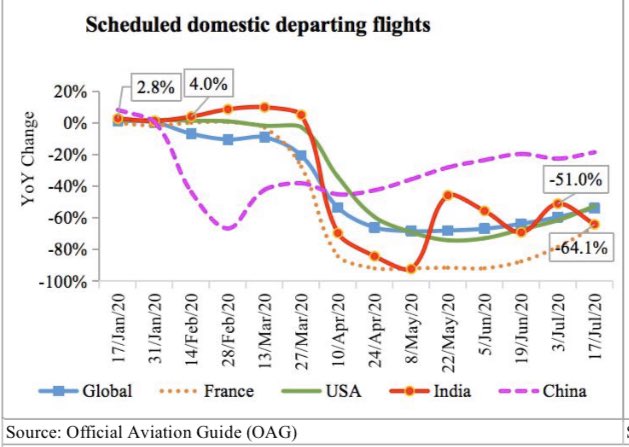

India unlocking and re-locking. Moderate improvement in rail passenger earnings in fortnight ending 19th July but aviation activity drops again. @tulsipriya_rk

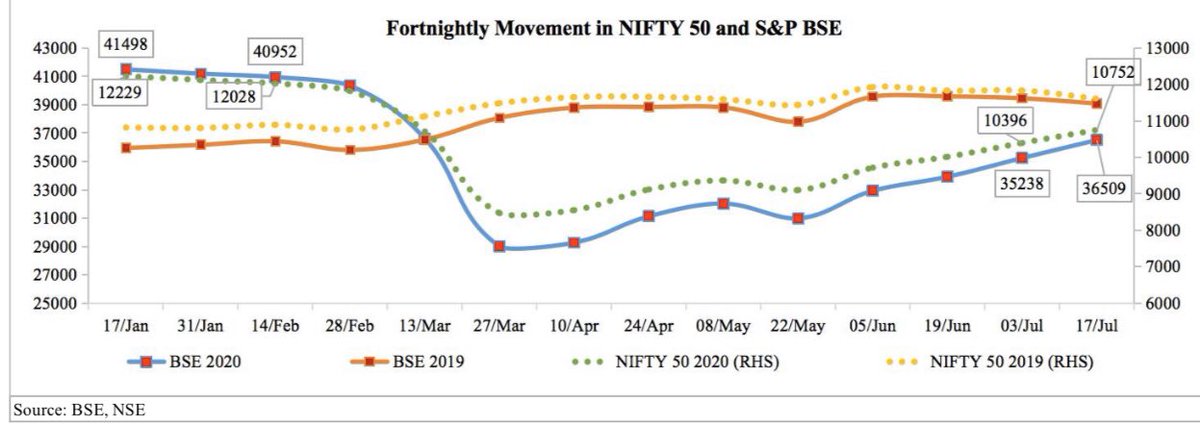

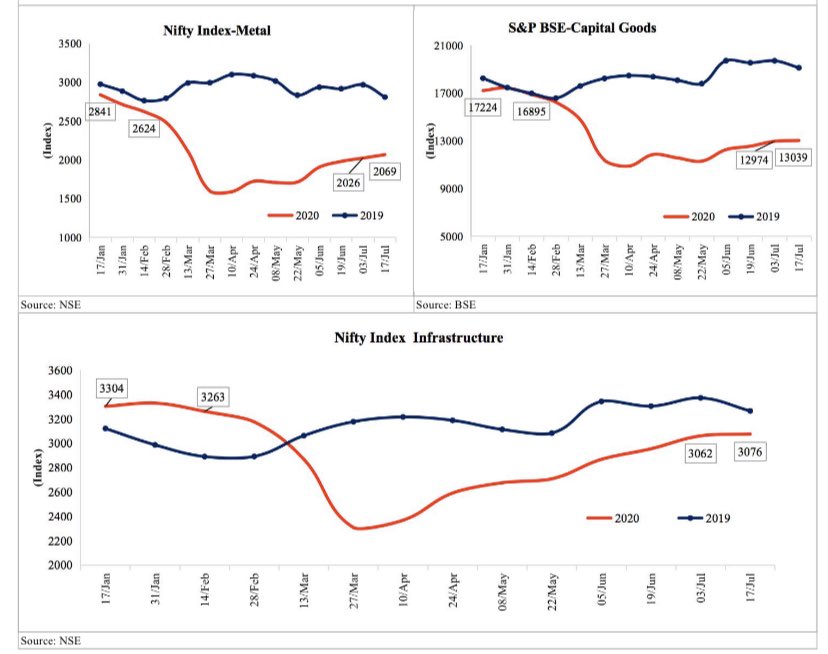

Buoyed optimism of financial markets continued led by infra, energy, banking and Pharma equities. @tulsipriya_rk

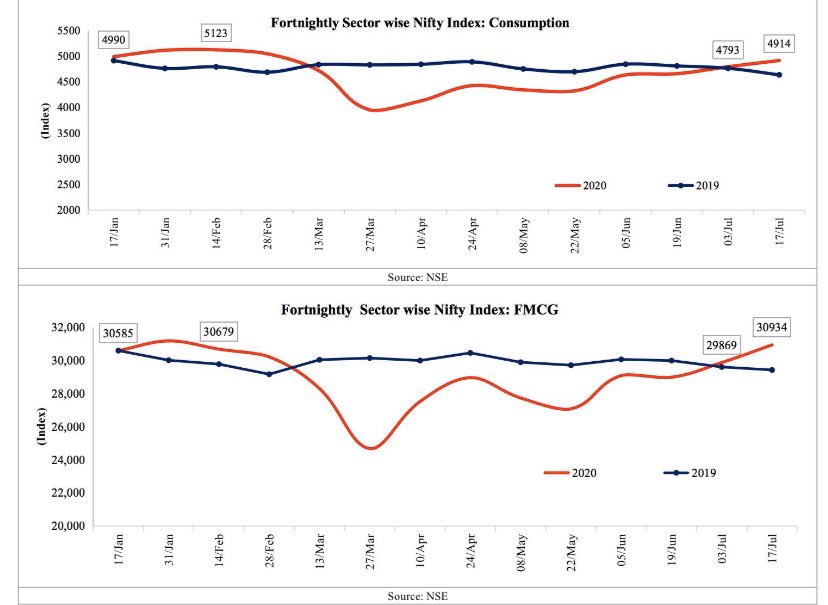

Inching previous year levels. Upbeat growth of consumption stocks.

Inching previous year levels. Upbeat growth of consumption stocks.

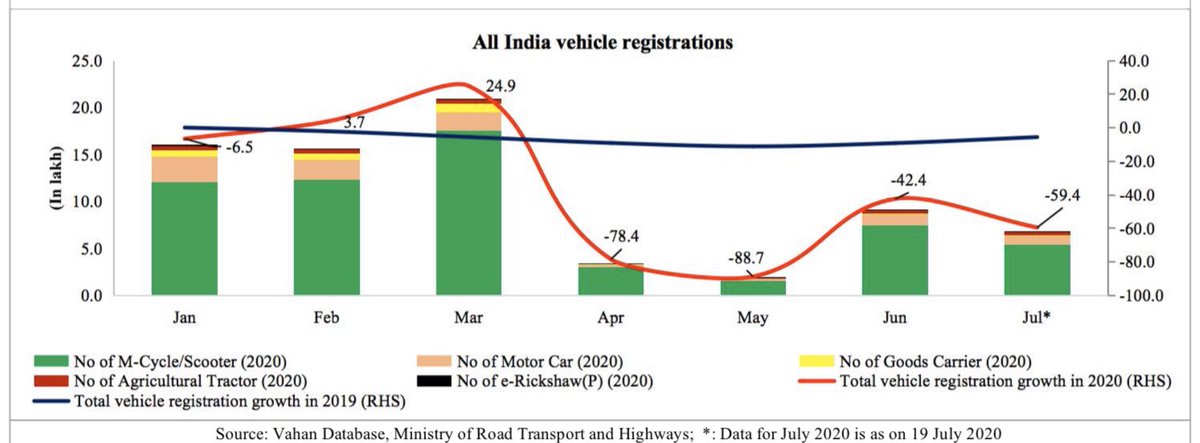

Vehicle registrations in first 20 days of July reached more than 40% of registrations seen in pre-Covid (February) and previous year ( full month of July). @tulsipriya_rk

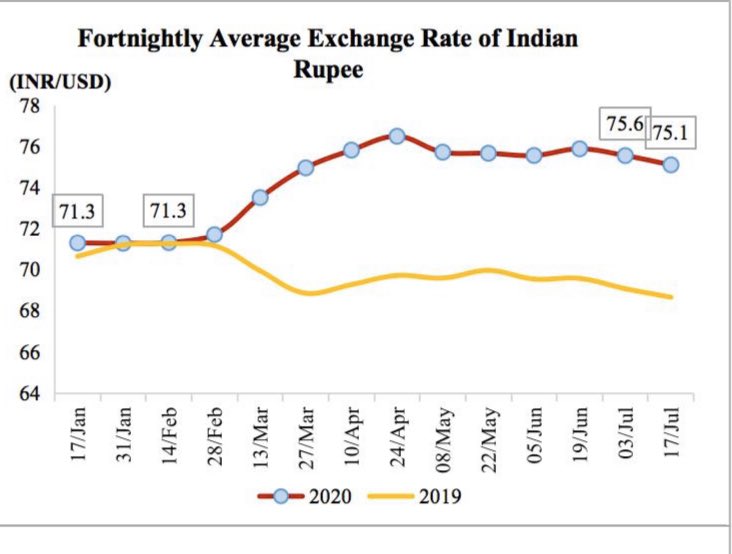

External sector update- Rupee continues appreciating trend amid healthy forex, trade balance improvement driven by sharp import decline, consistent foreign investment inflows and RBI’s liquidity management efforts in forex markets @tulsipriya_rk

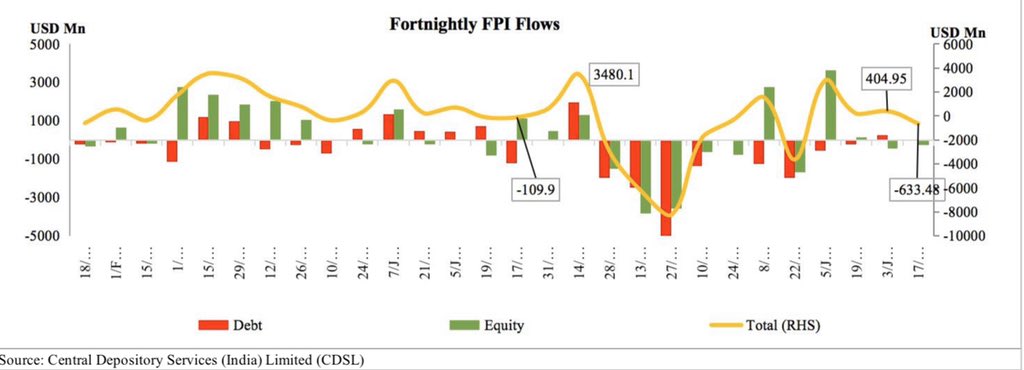

FPIs, however, turned net sellers in fortnight gone by driven by fall in debt inflows and equity outflows, profit booking after recent surge in Indian stock markets. RBI remained net purchase of dollars, though at lower level. FPI inv in G-Secs low and stable @tulsipriya_rk

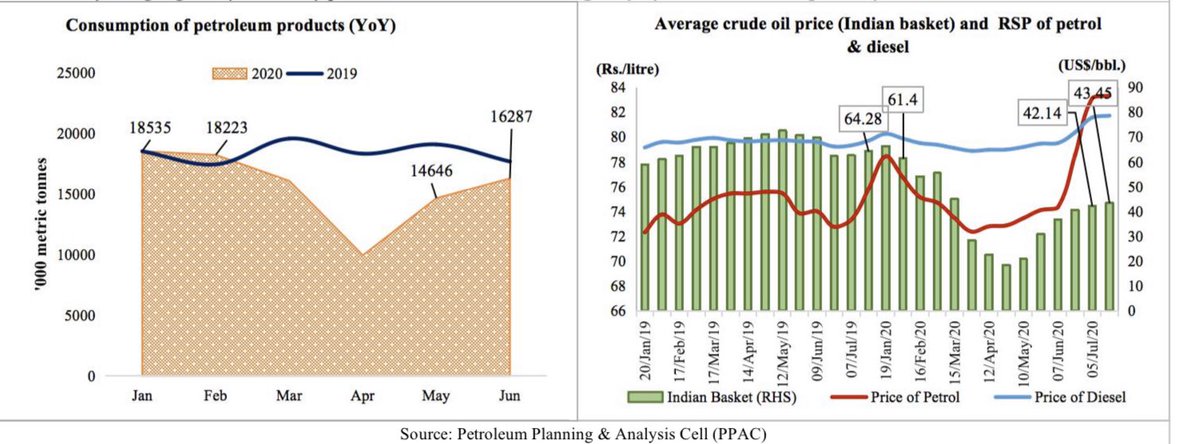

Consumption of petroleum products and gold imports picked up in June. Crude prices continued to rise in fortnight ending 19th July driven by OPEC+ supply declines. RSP of petrol and diesel high and rising. Yellow metal surge continued amid rising Covid cases. @tulsipriya_rk

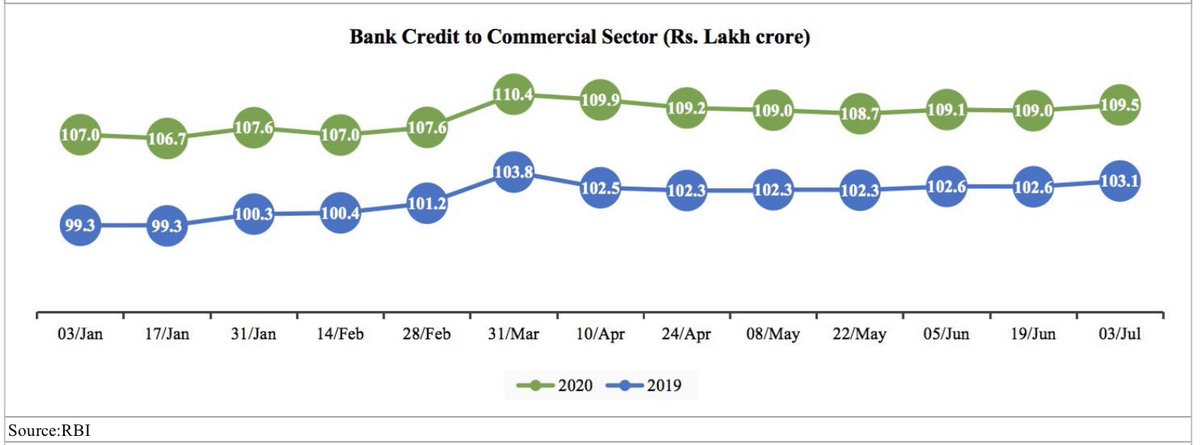

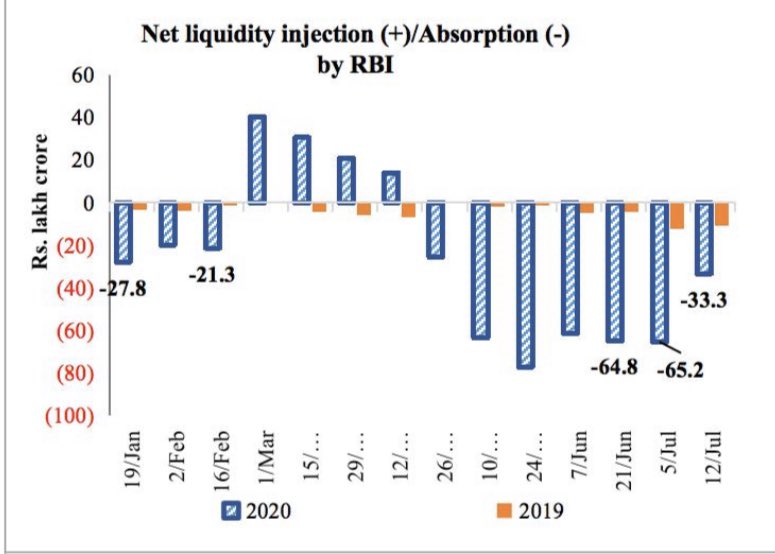

Bank credit growth continued to be tepid at 6.22% in fortnight ending 5th July, picked up marginally. Net liquidity absorption fell moderately in the subsequent week, lesser funds parked in reverse repo. @tulsipriya_rk

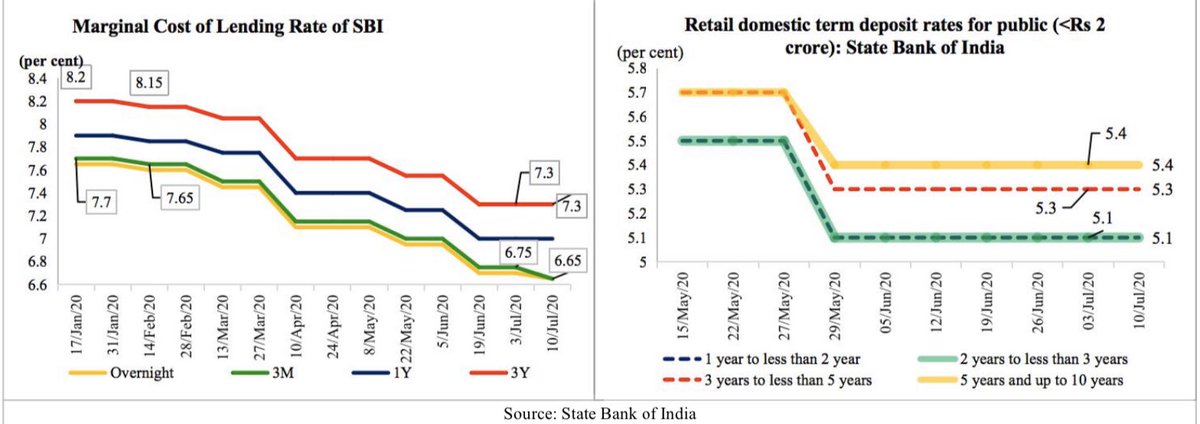

In June, Excess SLR portfolio holdings of risk averse bank were high and rising. In first 20 days of July, SBI’s MCLR reduced by 10 bps. Deposit rates unchanged.

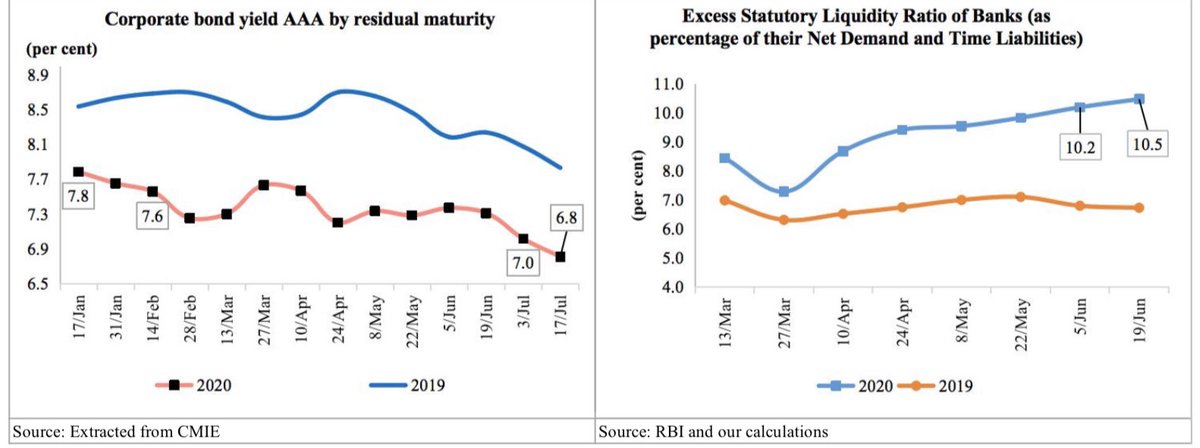

Corporate bond yields easing, on average, for 3 consecutive fortnights on account of RBI’s TLTROs. @tulsipriya_rk

Corporate bond yields easing, on average, for 3 consecutive fortnights on account of RBI’s TLTROs. @tulsipriya_rk

Average G-sec bond yields softened in fortnight ending 19th July compared to previous fortnight, still elevated relative to short term yields given excess market supply and increased fiscal borrowing. Centre’s cumulative FD upto May widened to Rs. 4.7 lakh crore @tulsipriya_rk

Centre and states gross and net market borrowings higher in fortnight ending 19th July as compared to prev year. Centre not relying on borrowings under WMA for 4 consecutive fortnights suggesting improving cash position, states continue to borrow from here well. @tulsipriya_rk