If MMTers were just doing standard Keynesian macro, then we would not have arrived at completely different conclusions (from mainstream Keynesians) re: the Bush tax cuts, the Clinton surpluses, the Euro, debt sustainability, interest rates (eg Japan vs Italy), the Trump tax cuts.

Our framework is grounded in Minsky, Godley, Lerner, (to name a few) and complemented/strengthened by interdisciplinary work, especially legal scholarship. If MMT was just Lerner's Functional Finance, we never would have gotten all the big stuff right.

No MMT economist urged lawmakers to return to PAYGO in 2007, complaining that the deficit was "driving down national saving." A mainstream Keynesians did.

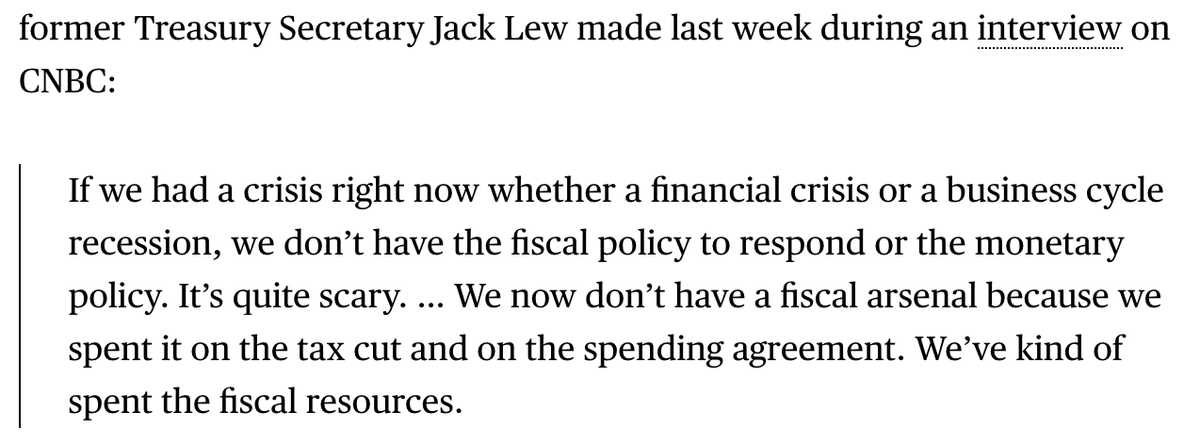

No MMT economist ever argued that the Trump tax cuts would leave us incapable of responding to the next recession. A mainstream Keynesian did.

No MMT economist cheered the Clinton surpluses or claimed that the US could end up like Greece. Many mainstream Keynesians did.

No MMT economist urged central banks to purse QE as a potent "reflationist" policy. Mainstream Keynesians did.

No MMT economist is today arguing that tax increases will be necessary to deal with the debt overhang in the post-COVID-19 era. Plenty of mainstream Keynesians are.

So please spare me the continued efforts to conceal the many failures of mainstream Keynesianism. We are working with a fundamentally different macro framework, one that takes money/finance/monetary operations/law/institutions seriously.

MMT integrates and builds on the work of Minsky, Godley, Keynes, Kalecki, Lerner, Innes, and others. The MMT framework looks nothing like mainstream Keynesianism, which explains why it has led us to such different conclusions over the decades. /end

No MMT economist claims that interest rates are the best tool to fight inflation. Mainstream Keynesians do.

No MMT economist believes that the central bank should target the "natural rate of unemployment." Mainstream Keynesians do.

No MMT economist adheres to "loanable funds" theory of the interest rate. Mainstream Keynesians do.

• • •

Missing some Tweet in this thread? You can try to

force a refresh