Debilitating uncertainty effects of July lockdowns and monsoons leveled off recovery in first fortnight of August. Check out our latest edition of Macroeconomics of India Series with @tulsipriya_rk #macroIndiaupdate #EconTwitter

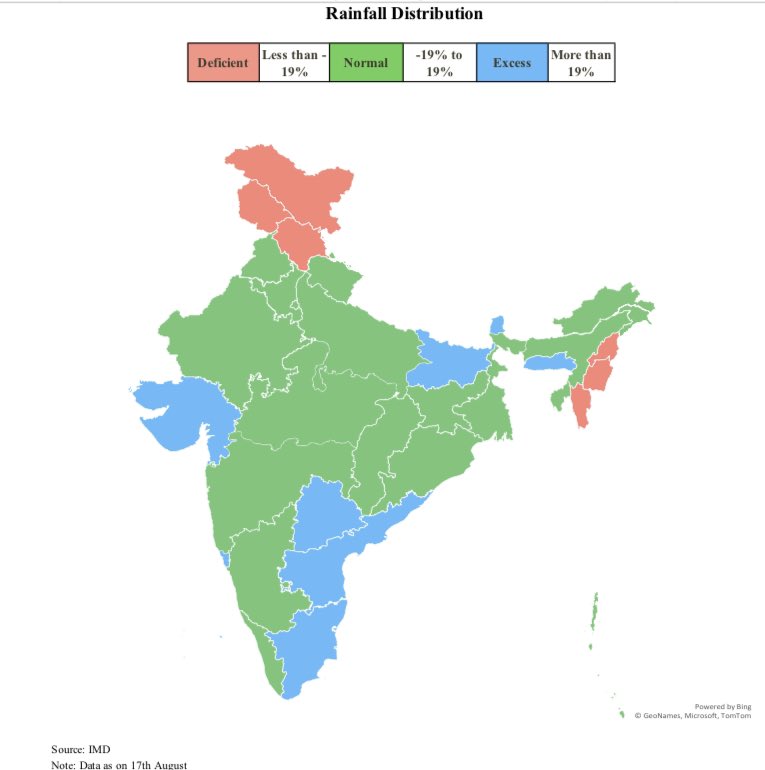

31 states have received normal or excess rainfall

31 states have received normal or excess rainfall

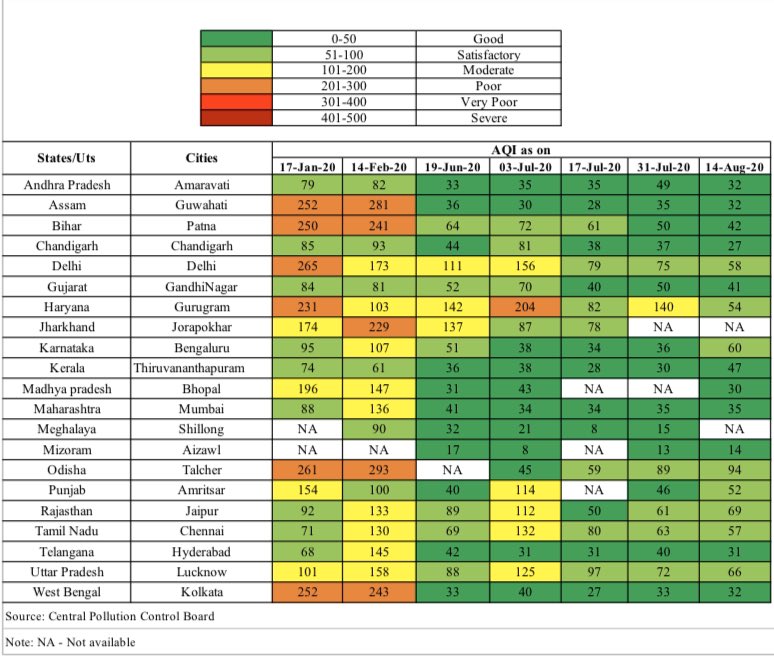

Air quality index as on 14th August indicated further improvement in majority of cities compared to pre-COVID levels. @tulsipriya_rk

Healthy monsoons continued to boost Kharif sowing area and water reservoir levels in the fortnight gone by.

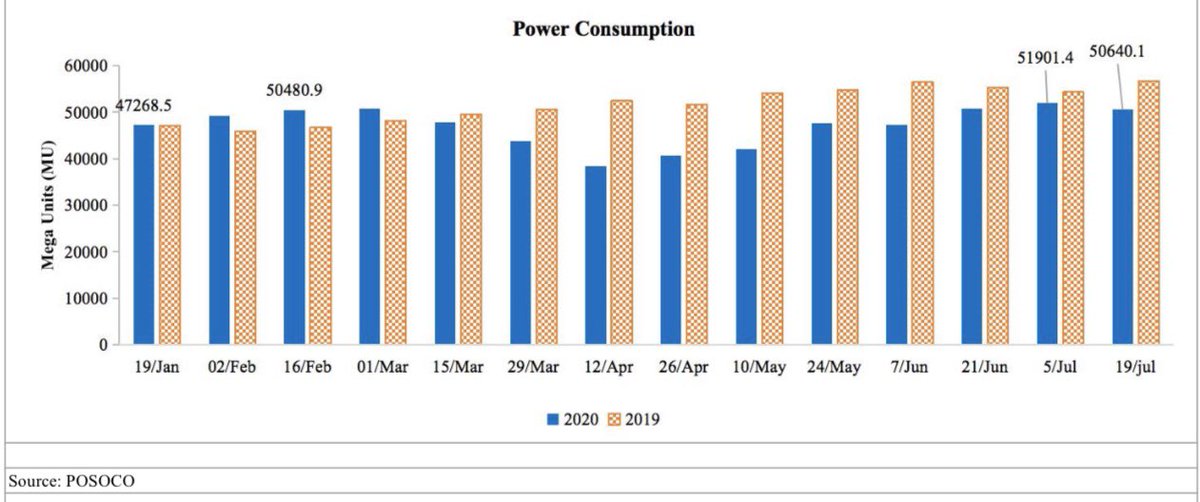

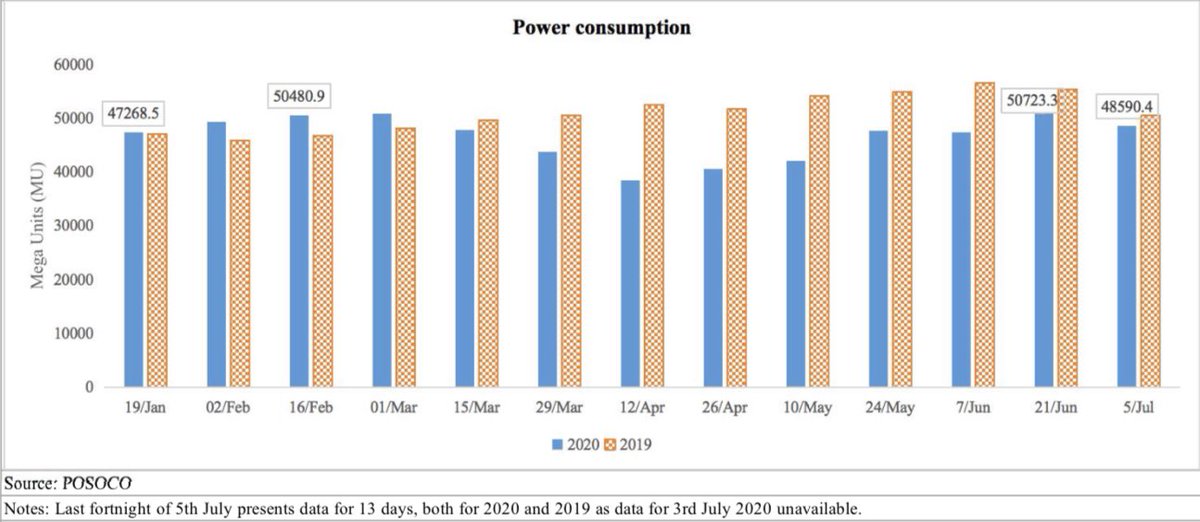

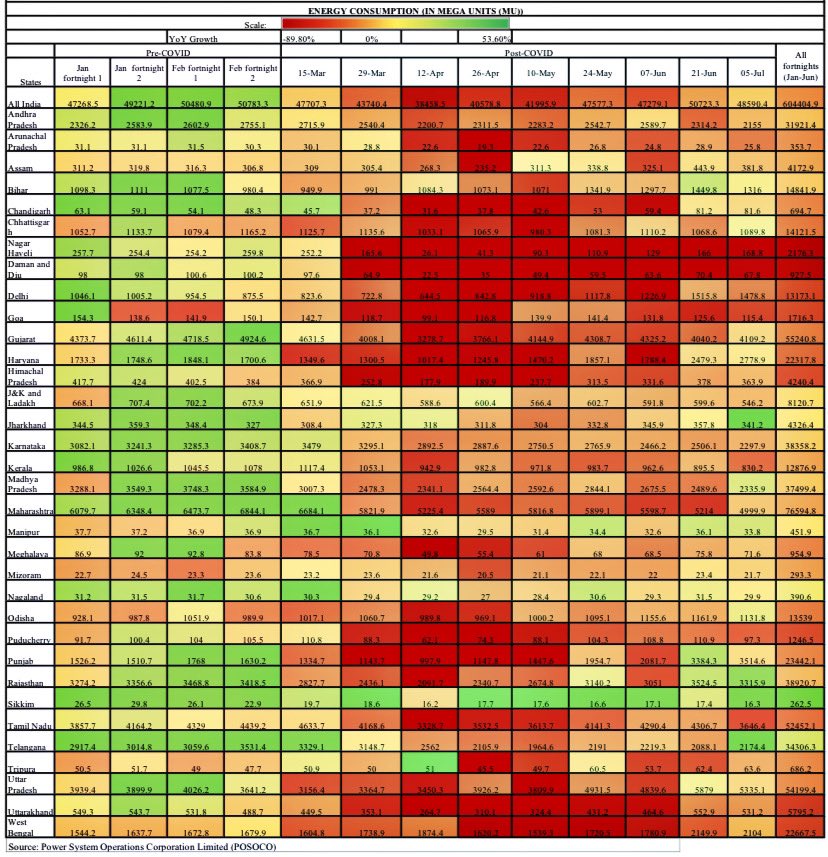

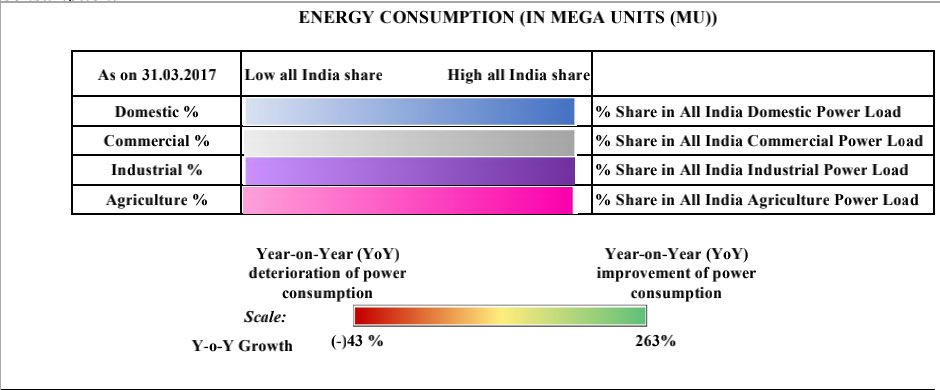

Power consumption declined both fortnight over fortnight and YoY(-0.2%). Sharp decline in Covid hotspots and top domestic and industrial load states like TN and in high Agri and industry load states like GJ and AP. @tulsipriya_rk

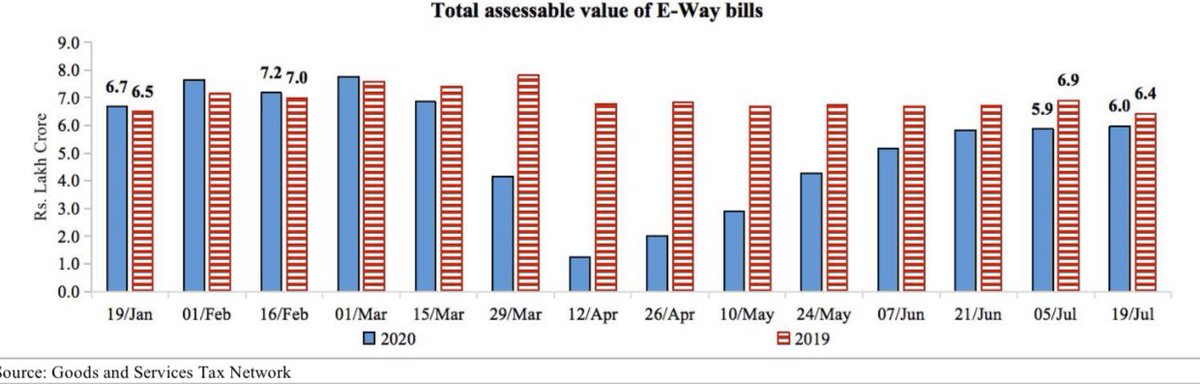

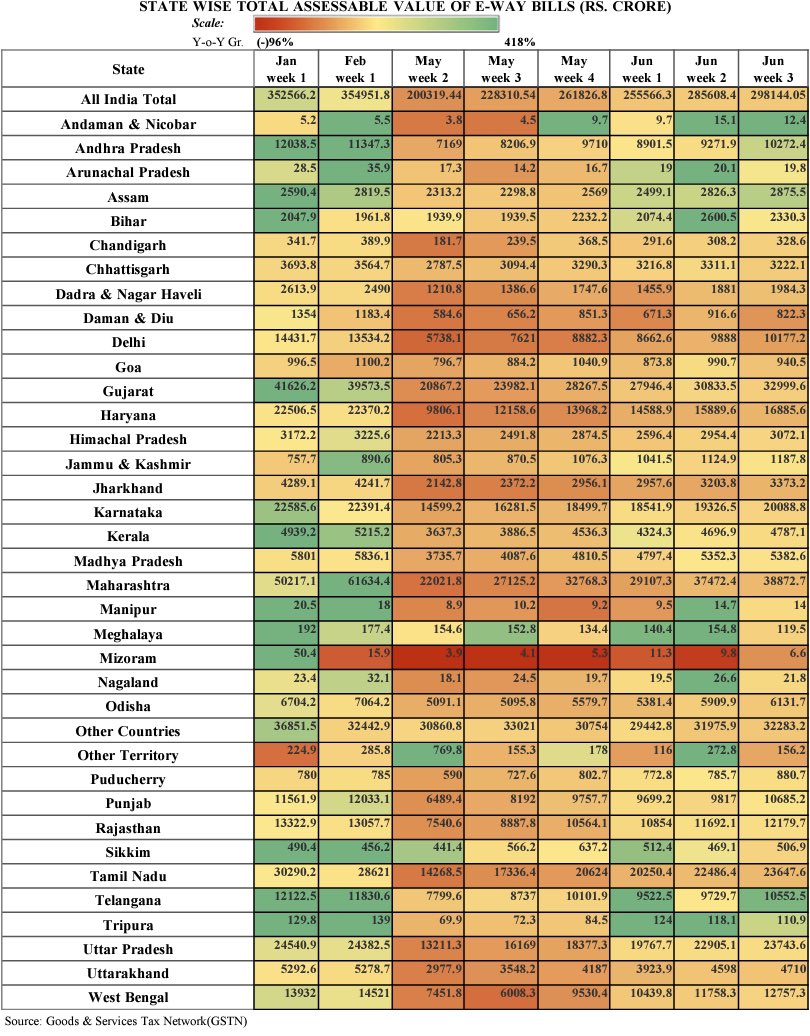

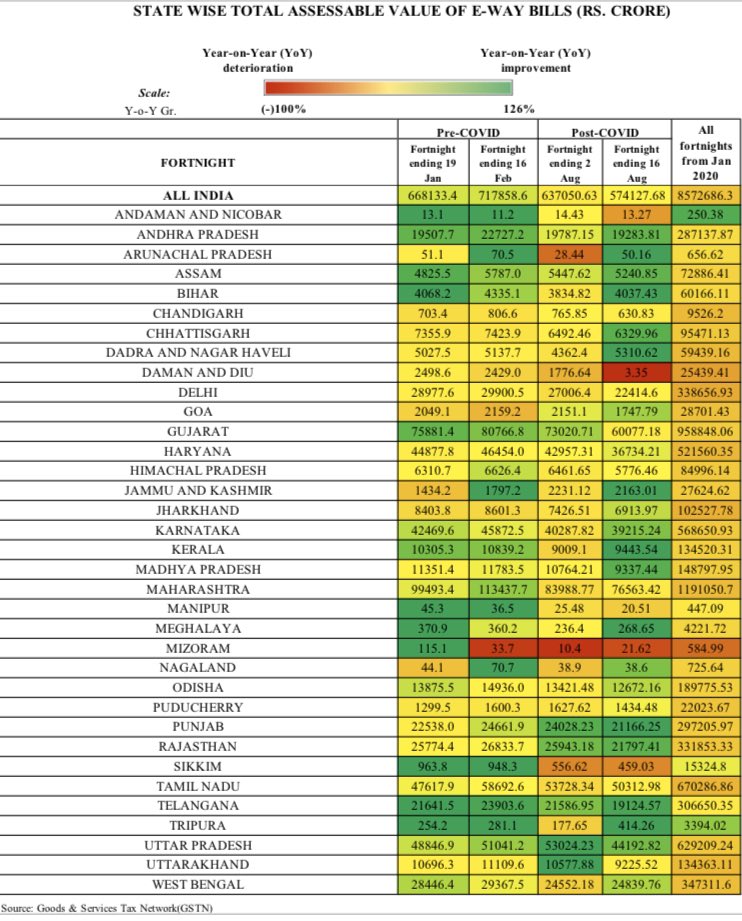

While E-way bills generated witnessed decline in fortnight gone by compared to prev fortnight, possibly due to seasonal factors, they touched previous year levels. WB, KL and BH reported improvement compared to previous year levels and preceding fortnight. @tulsipriya_rk

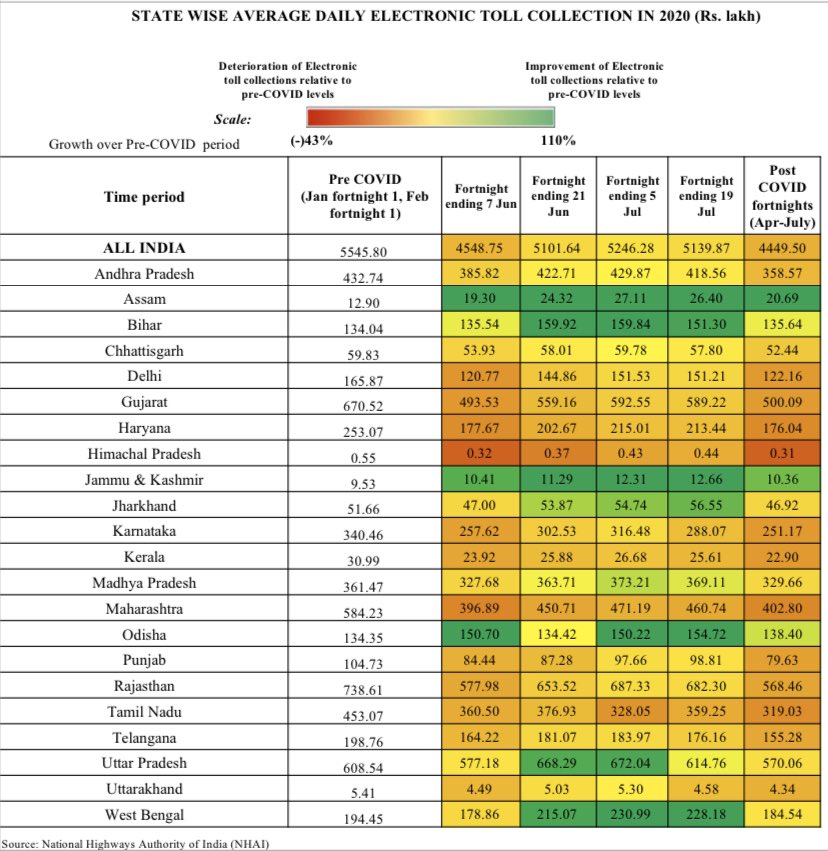

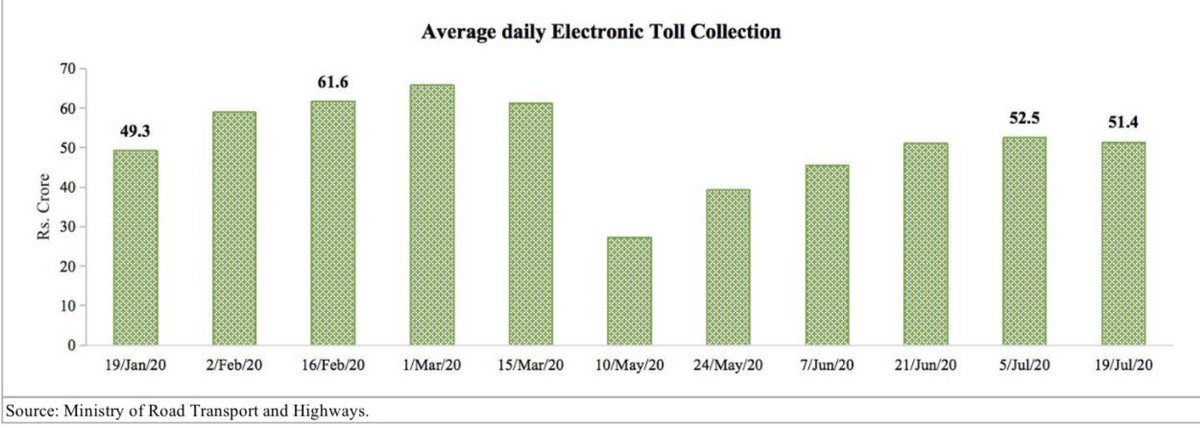

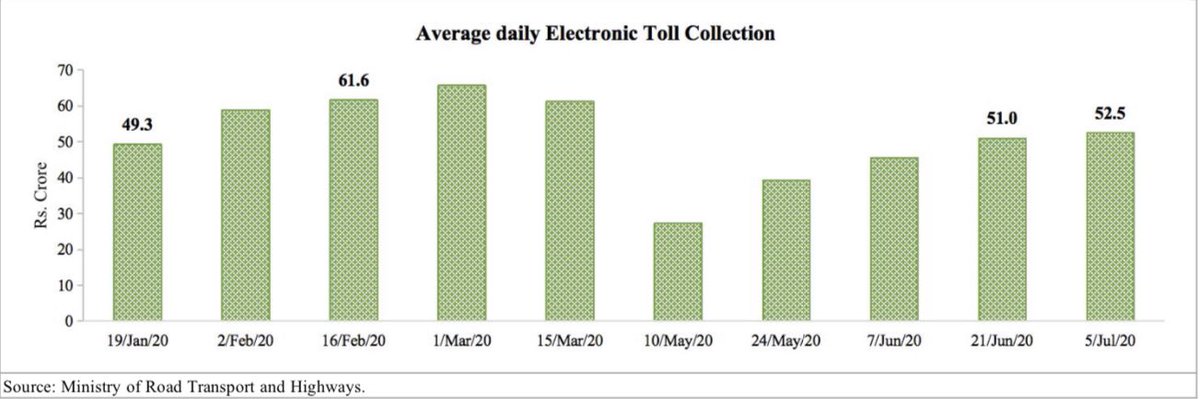

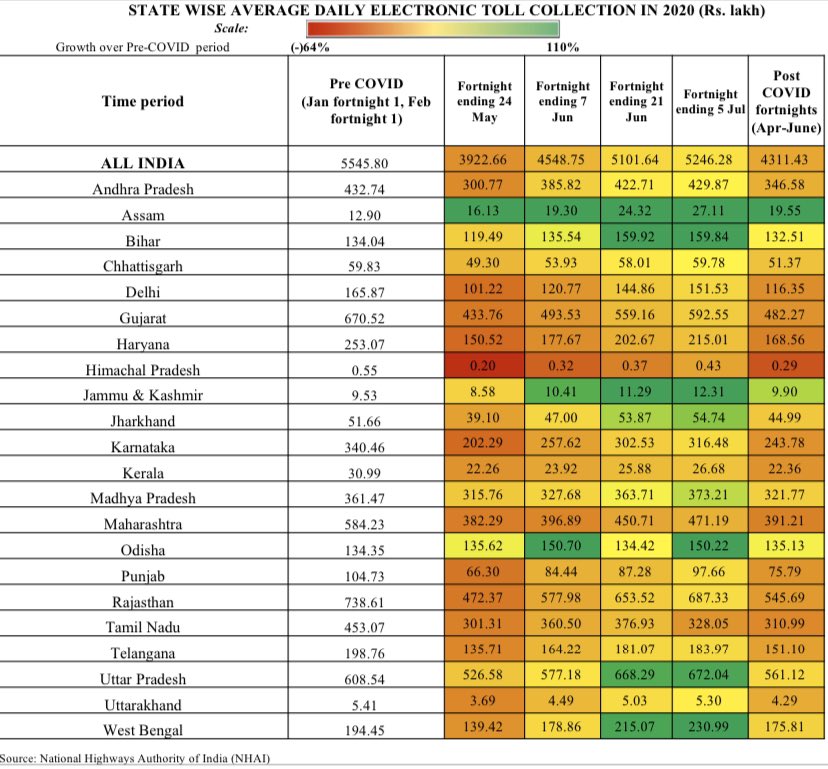

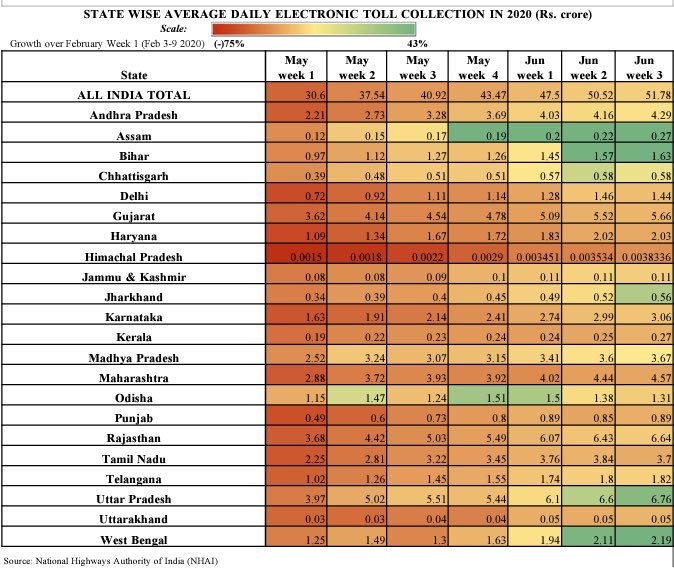

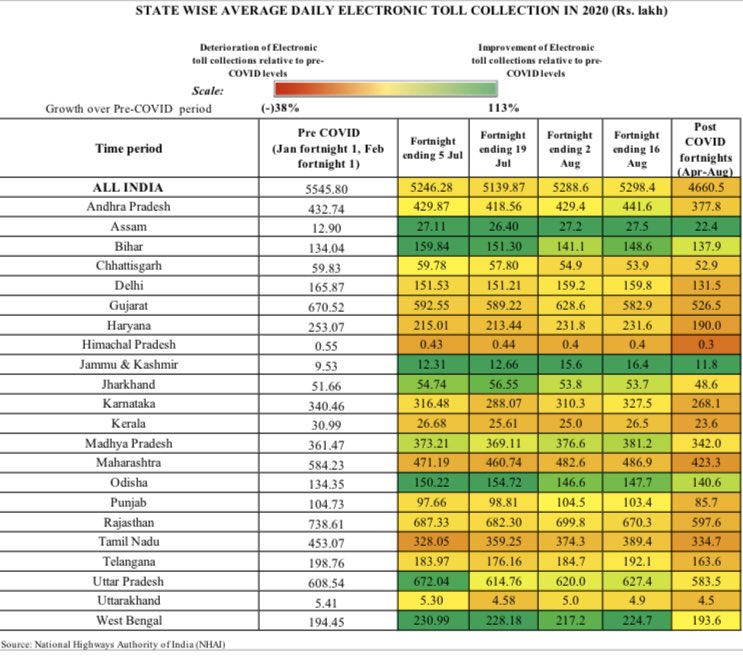

Average daily toll collection increased marginally in the fortnight gone by, reaching 86 per cent of pre-COVID levels, with improvement seen in West Bengal, Assam, Bihar, J&K, West Bengal and Odisha compared to pre- COVID levels. @tulsipriya_rk

Active cases growth fell sharply to 1% in fortnight ending 16th Aug from 2.6% in the preceding fortnight with recovery rate at 72.45%

DL more than 90% recovery, also HR, TN, GJ, RJ, TG and MP with more than 75% recovery. MH also picking up. CFR decline broad based except PB.

DL more than 90% recovery, also HR, TN, GJ, RJ, TG and MP with more than 75% recovery. MH also picking up. CFR decline broad based except PB.

Railway freight traffic recovered in July, reaching 95 per cent of previous year levels. Domestic aviation witnessed marginal pick up in activity.

Sensex and Nifty-50 witnessed muted activity in fortnight ending 14th August, with banks, financials and auto stocks reporting losses owing to weak global cues. NIFTY volatility continued to fall for the 9th consecutive fortnight giving mixed signals about market participation

On external front, India’s forex reserves at record highs covering more than 13 months of imports, supported by gains in FCA and rise in gold reserves. RBI’s regular forex spot interventn in forex spot market has subdued market volatility and confined rupee to a narrow range

Rupee stability further supported by continued FPI inflows in equities and lesser outflows in debt in the fortnight gone by.

Global oil markets recovery was restricted by OPEC+ supply cuts, only marginal increase in average crude prices. While average retail prices of petrol in metro cities remained unchanged in fortnight gone by, diesel prices fell.

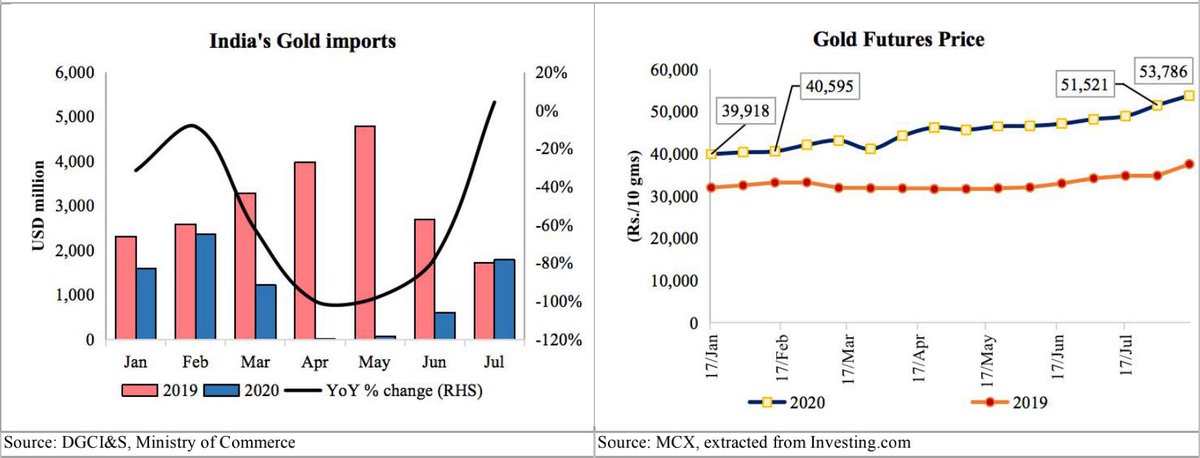

While YoY growth in consumption of petroleum products reported greater contraction in July 2020, gold imports witnessed uptick in July. Gold prices continued to remain elevated in the fortnight gone by.

Domestic investment outlook: While growth of bank credit to commercial sector increased by 0.4 per cent in the fortnight ending 31st July compared to previous fortnight, YoY growth continued to be tepid at 5.7 per cent. Metal and capital equities gained, infra moderate pick up.

Monetary: Net liquidity absorption increased to Rs. 33.8 lakh crore in the week ending 9th August compared to Rs. 30.3 lakh crore in the previous week. Policy rates were kept unchanged in the latest MPC meeting owing to inflationary pressures.

Food Inflation: Mandi arrivals of most agricultural commodities except groundnuts continued to decline in the fortnight gone by, possibly owing to monsoons. Retail food prices remained elevated relative to previous fortnight and previous year except for tomato.

Financial : On avg, corporate bond yield fell marginally to 6.8 per cent while 10 year G-sec yield stiffened to 5.9 percent amid rising inflation and lower scope for future rate cuts . Banks preferred to hold G-Secs with excess SLR standing higher in fortnight ending 31st July.

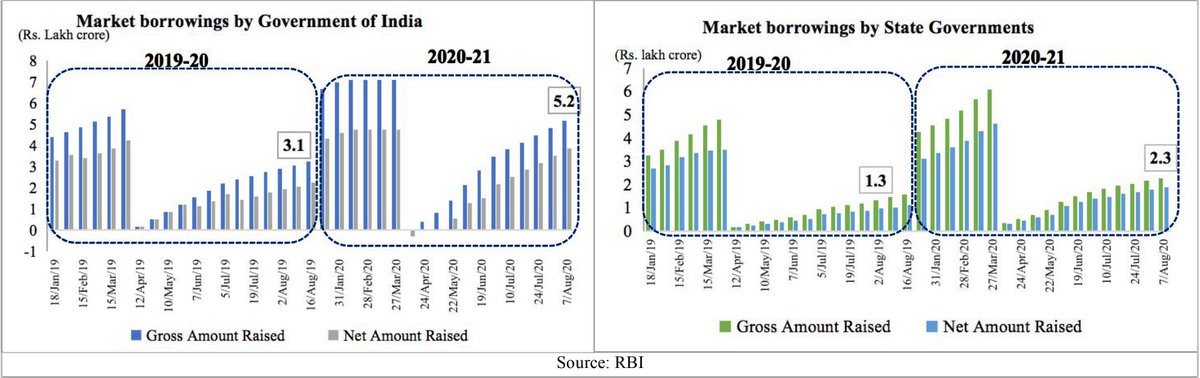

Fiscal: Centre’s gross and net borrowings upto 7th Aug increased by 1.7 and 1.9 times YoY. So did States. While Centre did not borrow from WMA window for ninth consecutive week, States borrowed 2.5 times more of last year levels in wk ending 7th Aug

unroll @threadreaderapp