🚨🚨🚨

A slew of recent data is consistent with slow or even negative jobs growth in November. A quick thread.

A slew of recent data is consistent with slow or even negative jobs growth in November. A quick thread.

November is typically a month when we expect raw, non-seasonally-adjusted employment data to *strengthen* (due, among other things, to hiring up for the holidays).

So when the unadjusted data is weakening or shrinking in November, that's an especially bad sign.

So when the unadjusted data is weakening or shrinking in November, that's an especially bad sign.

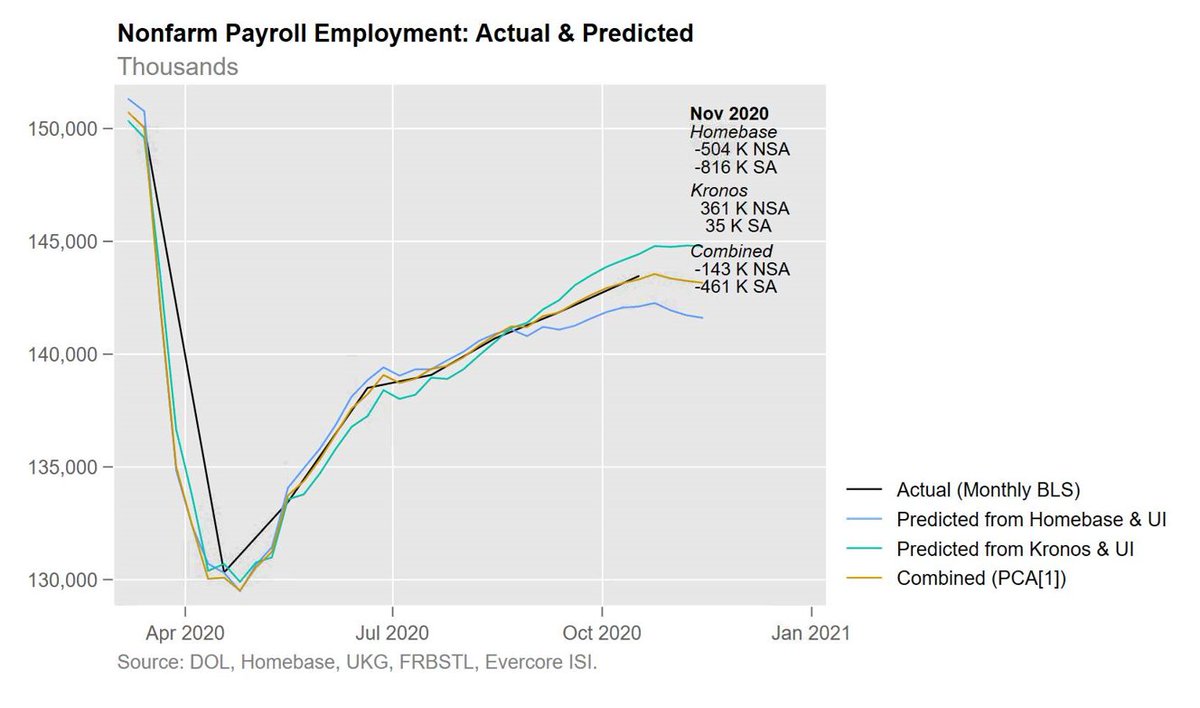

Data from Homebase, a private scheduling firm, suggest shrinking employment b/t mid-Oct and mid-Nov. Kronos, a different firm, shows slightly positive but weak growth.

Both, in tandem w/ UI claims, are consistent with -143K jobs in Nov not-seasonally-adjusted, or -461K adjusted.

Both, in tandem w/ UI claims, are consistent with -143K jobs in Nov not-seasonally-adjusted, or -461K adjusted.

The Homebase and Kronos data sometimes get revised week-to-week, however, so these estimates could shift. The revisions have tended to be modest.

The @uscensusbureau Household Pulse Survey meanwhile is showing a -1.8 percentage point decline in the employment-to-population ratio over the last 4 weeks. That's the equivalent of -4.5 million fewer workers, not-seasonally-adjusted.

The HPS has had large misses before however.

The HPS has had large misses before however.

We're also beginning to see some signs of slowdown in states with more recent COVID surges, such as through lower mobility and soggier Homebase employment, though earlier Spring Peak states are also showing signs of decline.

So at this point, we have several data sources--Homebase, Kronos, the HPS, and mobility data--pointing to a weak or negative Nov labor market.

Some might firm a bit in the weeks ahead with revisions (though they might weaken too).

But what there is so far doesn't bode well.

Some might firm a bit in the weeks ahead with revisions (though they might weaken too).

But what there is so far doesn't bode well.

I lay out a few more caveats and go into two data sources that are pointing the other direction in this companion thread.

https://twitter.com/ernietedeschi/status/1330898234009669632

• • •

Missing some Tweet in this thread? You can try to

force a refresh