Welcome to the "Omnirally". The development of Covid vaccines has helped nurture the single biggest monthly gain for global equities on record. But is the euphoria obscuring some festering economic challenges? My latest big read: ft.com/content/d78563…

For sure, the global economy has bounced far more strongly than we dared hope earlier this year, and corporate profits will follow next year.

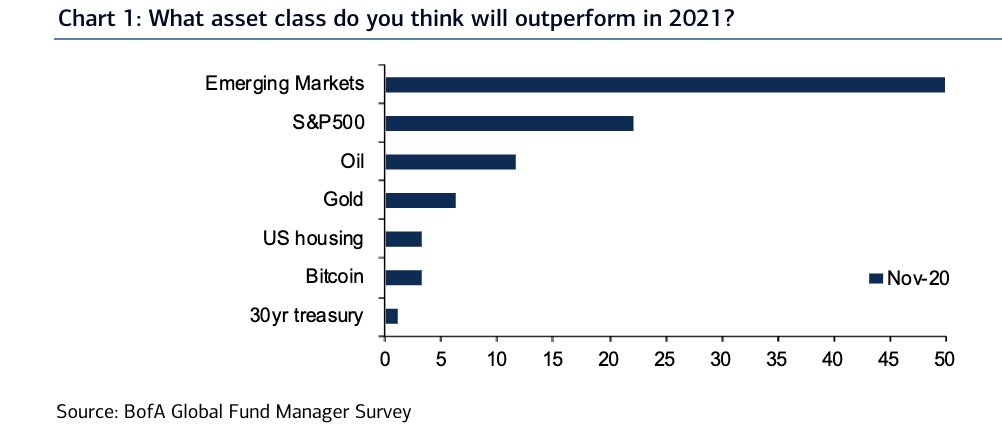

But the optimism is palpable. Fund managers haven't been this optimistic that growth and profits will strengthen in nearly two decades.

Equity overweights are the highest since February 2018, when markets were basking in the US corporate tax cut afterglow, and cash reserves close to the lowest in seven years.

Bears are throwing in the towel. Short positioning in US stocks has never been lower, according to Goldman Sachs. bloomberg.com/news/articles/…

Even the bulls are nervous about how almost everyone seems optimistic at the moment.

And the few remaining bears, like GMO's Jeremy Grantham, are just awestruck at what they think is a picture-perfect, history book-worthy ticks-all-the-boxes stock market bubble.

• • •

Missing some Tweet in this thread? You can try to

force a refresh