Focus on the ECB on Thursday (but also on PEPP breakdown today and TLTRO-III.6 on Tursday).

We have an ECB pre-committment and a firm consensus - how could the ECB surprise? (1/n)

We have an ECB pre-committment and a firm consensus - how could the ECB surprise? (1/n)

https://twitter.com/fwred/status/1334867967474098179

The ECB's focus will be on the *duration* of policy support

more than on the *intensity* of asset purchases. The ECB could extend PEPP & TLTROs for even longer, although the consensus will have moved closer to our view by now. (2/n)

more than on the *intensity* of asset purchases. The ECB could extend PEPP & TLTROs for even longer, although the consensus will have moved closer to our view by now. (2/n)

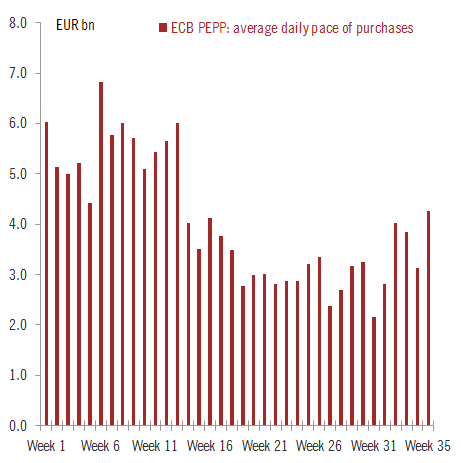

In order to extend the PEPP to June 2022, the ECB will need to increase its size by €450-850bn, so they could also surprise with a larger number (>€600bn).

We expect flexibility on both sides: the envelope might not be used in full, but they'll be ready to do more. (3/n)

We expect flexibility on both sides: the envelope might not be used in full, but they'll be ready to do more. (3/n)

What about the APP as the €120bn Temporary Envelope expires? We think the APP will be increased at a later stage, most likely after the conclusion of the strategy review, along with a transfer of flexibility from the PEPP to the APP. (4/n)

What about other asset classes? Concerns over corporate vulnerabilities and a premature withdrawal of government support suggest the inclusion of corporate fallen angels in the PEPP is possible. Adding bank debt would be a huge surprise, still unlikely for now. (5/n)

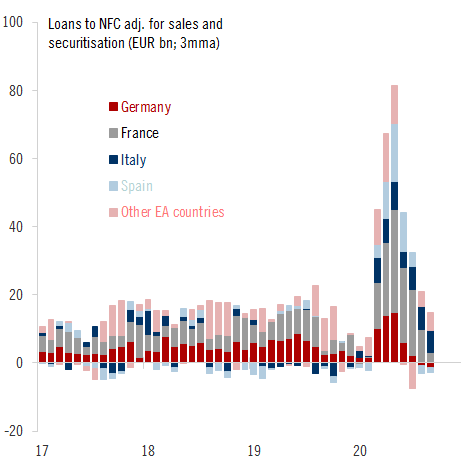

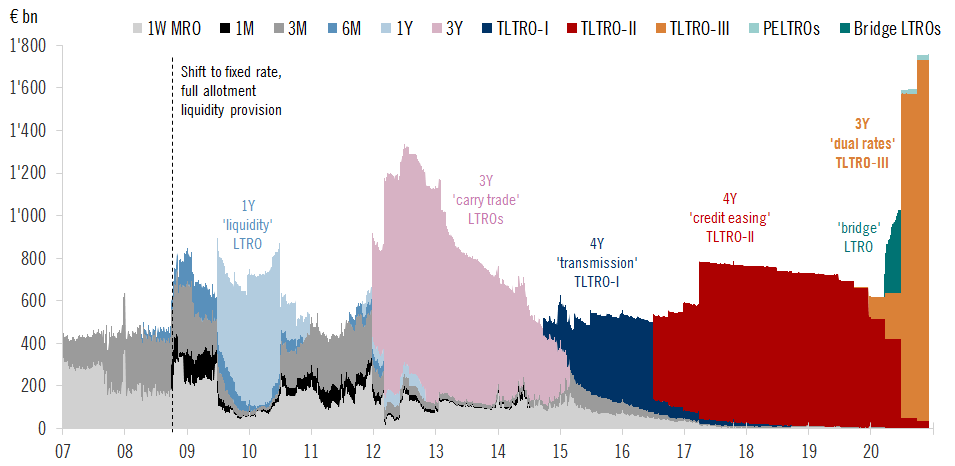

What about TLTROs? The ECB should extend the discount period of -1% rate to June 2022 at a minimum. They could also cut the minimum rate by 25bp, increase maturities, boost allowances, and/or include mortgages in the eligible loan book. (6/n)

No deposit rate cut, so what about the EUR? The FX pain threshold is state-dependent, and the EUR has been rising for good reasons.

This could be a tricky one for @Lagarde not to sound too hawkish, and another reason to push for larger QE boost. (7/n)

This could be a tricky one for @Lagarde not to sound too hawkish, and another reason to push for larger QE boost. (7/n)

A higher tiering multiplier at last? The cost of NIRP has exceeded €15bn on an annual basis, but net of tiering and TLTROs the ECB has engineered a net *transfer* of more than €5bn to banks. A higher tiering multiplier is possible (8-10x) but not a pressing issue (8/8).

• • •

Missing some Tweet in this thread? You can try to

force a refresh