Iceberg might have a point here

$WW is Weight Watchers

$WW is Weight Watchers

https://twitter.com/icebergdevalor/status/1344931424298741761

Don't worry, not going on a bender with filings

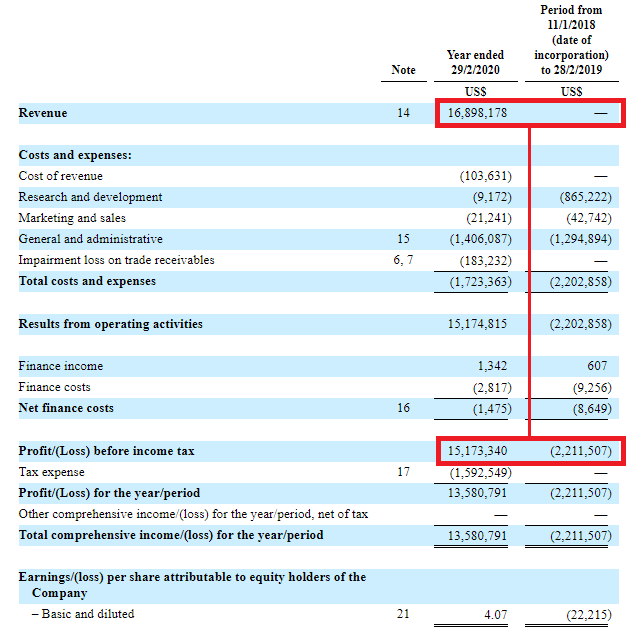

T9M figures last 4 years. Yes it's a bit stagnant in the numbers and costs up / profit down a little etc but the COGs numbers are roughly consistent. You could imagine a jump in revenues flowing through quite well.

2018 was Oprah

T9M figures last 4 years. Yes it's a bit stagnant in the numbers and costs up / profit down a little etc but the COGs numbers are roughly consistent. You could imagine a jump in revenues flowing through quite well.

2018 was Oprah

Fair to guess lots of New Year gym sign-ups are postponed or never happen and more NY lose weight / get fit resolutions than usual find their way here instead?

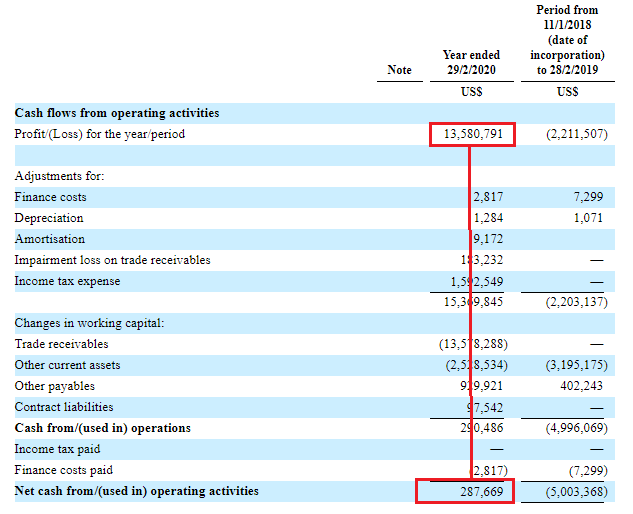

Cashflow behaves roughly the same. More SBC, bit more capex.

Cashflow behaves roughly the same. More SBC, bit more capex.

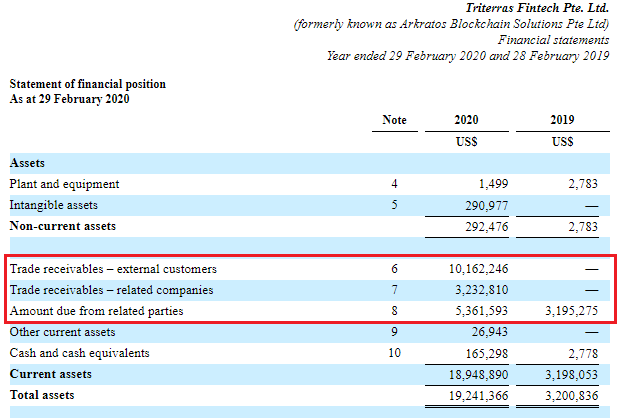

Balance sheet not much changed

Overall, not an entirely dissimilar company to before

2021 is the first NY w/Covid, lots of fitness options are closed off, which produces an Oprah bump, that then flows well into the financials and subscriber numbers jump even more than usual?

Overall, not an entirely dissimilar company to before

2021 is the first NY w/Covid, lots of fitness options are closed off, which produces an Oprah bump, that then flows well into the financials and subscriber numbers jump even more than usual?

Anyway, I don't know the company and I don't know what Iceberg has in mind (whatever it is, it'll be vastly better thought through than this - you should follow him) and this is all just a lazy first level thinking with the idea that there's a chance the stock might pop a bit.

• • •

Missing some Tweet in this thread? You can try to

force a refresh