1/ Institutional Gold (Parikh)

"Gold’s correlations are sensitive to the investor’s horizon and time period. We discuss the difficulties of estimating correlations (especially for long horizons) and the importance of measuring estimation uncertainty."

papers.ssrn.com/sol3/papers.cf…

"Gold’s correlations are sensitive to the investor’s horizon and time period. We discuss the difficulties of estimating correlations (especially for long horizons) and the importance of measuring estimation uncertainty."

papers.ssrn.com/sol3/papers.cf…

2/ * Futures include cash returns

* Rolls to contract with the most favorable carry or (if carry is negative) to a simulated gold ETF with 40 bps/y expenses

* Using this roll strategy has 7.1%/year returns vs. 4.8% for rolling monthly

More on this here:

* Rolls to contract with the most favorable carry or (if carry is negative) to a simulated gold ETF with 40 bps/y expenses

* Using this roll strategy has 7.1%/year returns vs. 4.8% for rolling monthly

https://twitter.com/ReformedTrader/status/1269093206513180673

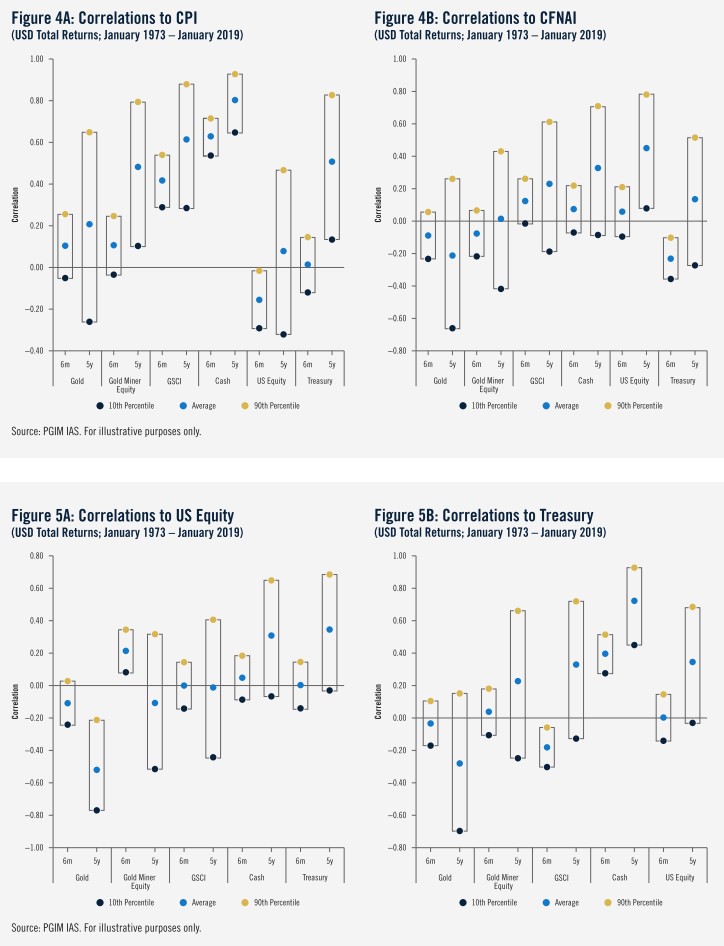

3/ "Gold might serve as a long-term hedge against economic slowdowns, was the only asset to have negative correlation to equity at the 90th percentile for 5y horizon returns, and (of all the assets) was the most diversifying to Treasuries."

4/ "Like our correlation estimation methodology, we use the bootstrap to conduct the regression analysis using simultaneously sampled asset returns, macroeconomic and market variables. We repeat 10,000 times, each with a different sample, for each set of horizon returns (6m-5y)."

5/ "Figure 7 summarizes the gold and gold miner equity relationships with CPI and CFNAI and how these relationships differ with the length of the investment horizon."

CPI = U.S. CPI

CFNAI = Chicago Fed National [economic] Activity Index

CPI = U.S. CPI

CFNAI = Chicago Fed National [economic] Activity Index

6/ "Depending on the investment horizon, the optimal weights to asset classes vary for a given target level of inflation or growth exposure. Notably, there is a portfolio role for gold-related assets separate from those of commodities and energy equities."

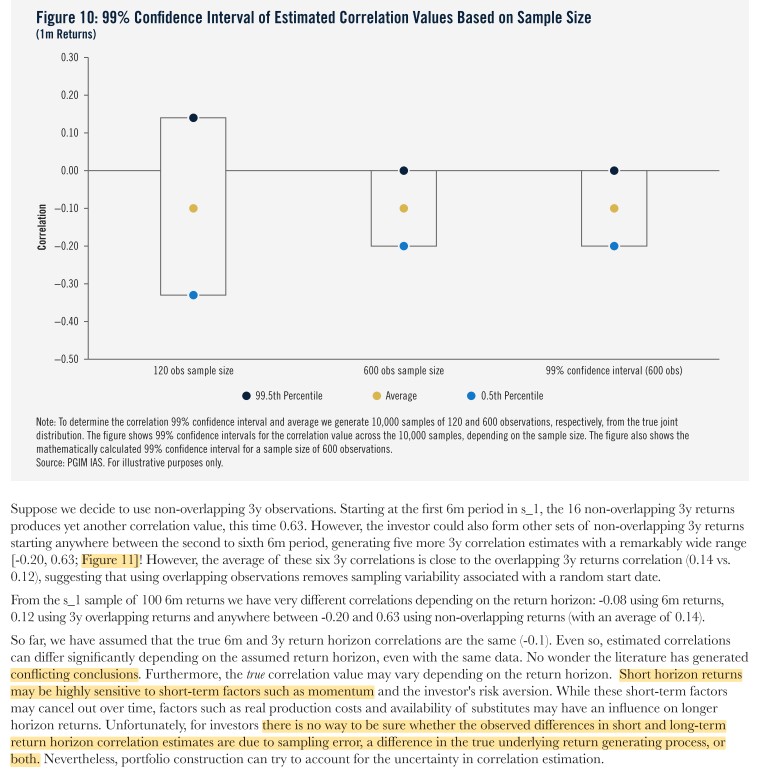

7/ "Correlations can be wildly different depending on the return horizon even for the *same* sample.

"Short-horizon returns may be sensitive to short-term factors (momentum).

"There is no way to be sure whether differences are from sampling error, a true difference, or both."

"Short-horizon returns may be sensitive to short-term factors (momentum).

"There is no way to be sure whether differences are from sampling error, a true difference, or both."

8/ "Although the true correlation is -0.1 [for this random sample, by construction], the wide range of the confidence interval suggests the investor may estimate either negative or positive values from the available sample data."

• • •

Missing some Tweet in this thread? You can try to

force a refresh