Big number!

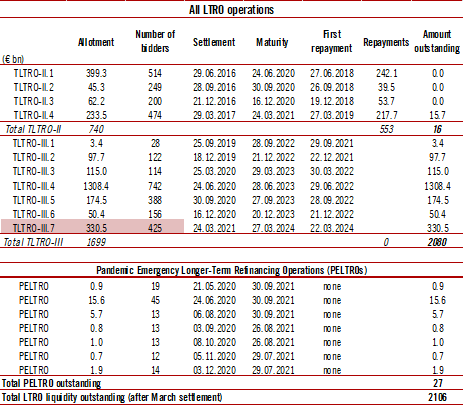

425 banks took €330.5bn in ECB's TLTRO-III.7 operation, highest since June.

A positive sign for the banking sector and the real economy.

/thread

425 banks took €330.5bn in ECB's TLTRO-III.7 operation, highest since June.

A positive sign for the banking sector and the real economy.

/thread

https://twitter.com/fwred/status/1372183660363927552

This large take-up will result in a €315bn increase in total TLTRO borrowing (to €2080bn excluding PELTROs) after €15.7bn mature from the final TLTRO-II.4 next week.

€330.5bn represents a 18% increase in total TLTRO borrowings vs. a 10% increase in borrowing capacity following the ECB decision (from 50% to 55% of eligible loans). It suggests that banks in the core have increased their borrowing more than proportionally.

This is particularly important because core banks, which have a good visibility over their lending performance vs TLTRO benchmarks, could be more optimistic relative to future lending including after the expiry of state loan guarantees.

Here's the TLTRO history chart, a thing of beauty indeed @natacha_valla.

Total longer-term liquidity provision will rise to €2106bn, above the €2 trillion mark for the first time ever.

Total longer-term liquidity provision will rise to €2106bn, above the €2 trillion mark for the first time ever.

With excess liquidity close to €3700bn and rising, today’s operation will make little difference to money markets. But if anything it confirms the importance of TLTROs as a central part of the ECB's toolkit. No need to ease conditions for now, but they are here to stay.

• • •

Missing some Tweet in this thread? You can try to

force a refresh