US Swaption/Rates Vol off highs but still elevated

Reasons:

▪️ Economic data ahead; CPI tom; Fed data dependent

▪️ UST supply, 3y 10y 30y auctions this wk

▪️ US ylds, off highs, still close to higher end => risk premium in vols

▪️ Market v/s Fed disconnect on Rate Hike

1/4

Reasons:

▪️ Economic data ahead; CPI tom; Fed data dependent

▪️ UST supply, 3y 10y 30y auctions this wk

▪️ US ylds, off highs, still close to higher end => risk premium in vols

▪️ Market v/s Fed disconnect on Rate Hike

1/4

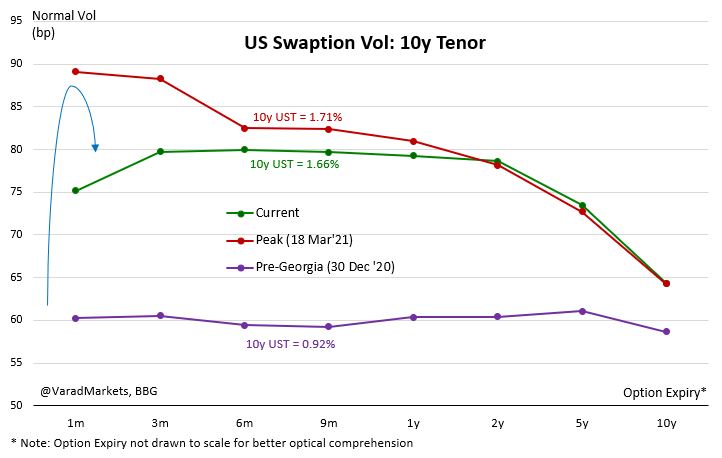

▪️ SEP-based June FOMC important => till then would have got two more NFPs & Inflation data till May incorporating Apr/May base effect + stimulus based spikes => little kink around 3m in vol curve

▪️ Vol Skew mildly softer but still topside nervousness (convexity hedging)

2/4

▪️ Vol Skew mildly softer but still topside nervousness (convexity hedging)

2/4

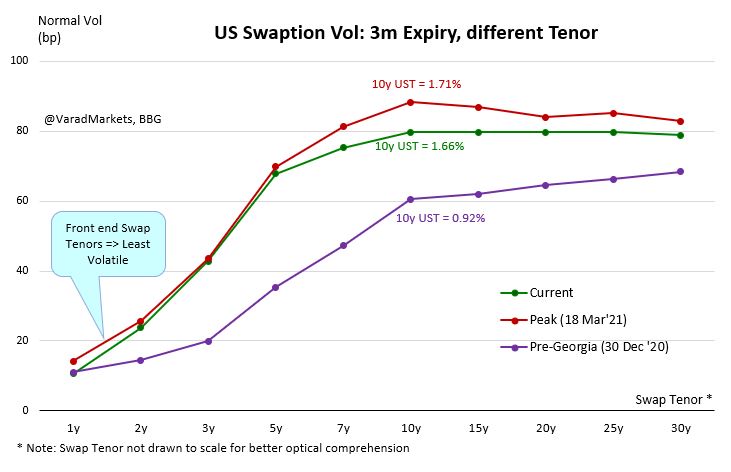

▪️ Chart: 3m Expiry Vol across Swap Tenors => Front end swap tenors least volatile as anchored by Fed Fund/OIS/T-Bill yields

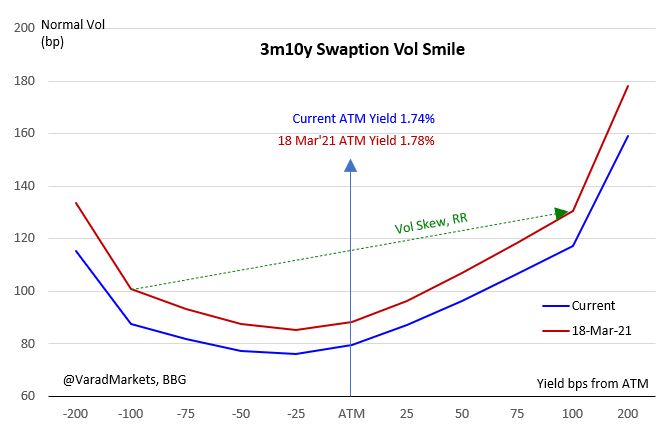

▪️ Chart: 3m10y Swaption Vol v/s 10yr US Yield: higher yield => higher vol as reflected in Vol Skew

3/4

@bondstrategist

▪️ Chart: 3m10y Swaption Vol v/s 10yr US Yield: higher yield => higher vol as reflected in Vol Skew

3/4

@bondstrategist

https://twitter.com/VaradMarkets/status/1371717468276727810?s=20

Basic Swaption recap:

▪️ Option on USD Interest Rate Swap (IRS); Call (Payer); Put (Receiver)

▪️ Two time horizons:

1⃣ Tenor of underlying swap

2⃣ Maturity/expiry of option

▪️ Vol Cube => Vol across Strike vs Tenor vs Maturity

▪️ 3m10y => 3m Expiry Option on 10yr USD IRS

▪️ Option on USD Interest Rate Swap (IRS); Call (Payer); Put (Receiver)

▪️ Two time horizons:

1⃣ Tenor of underlying swap

2⃣ Maturity/expiry of option

▪️ Vol Cube => Vol across Strike vs Tenor vs Maturity

▪️ 3m10y => 3m Expiry Option on 10yr USD IRS

• • •

Missing some Tweet in this thread? You can try to

force a refresh