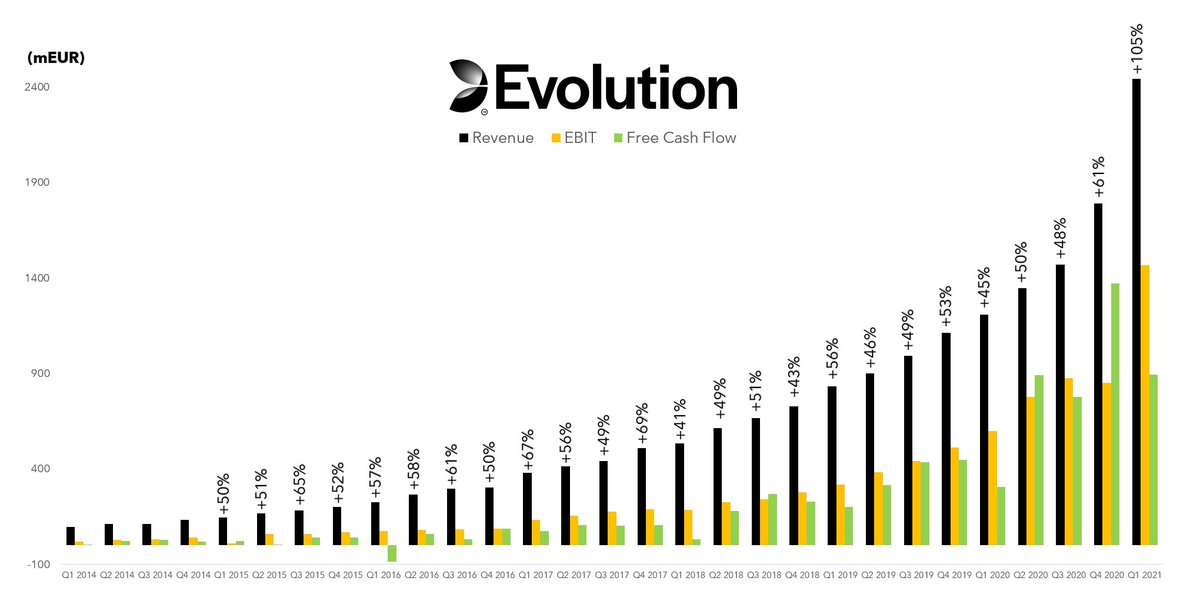

$EVO Q2'21💥

Revenue +100%

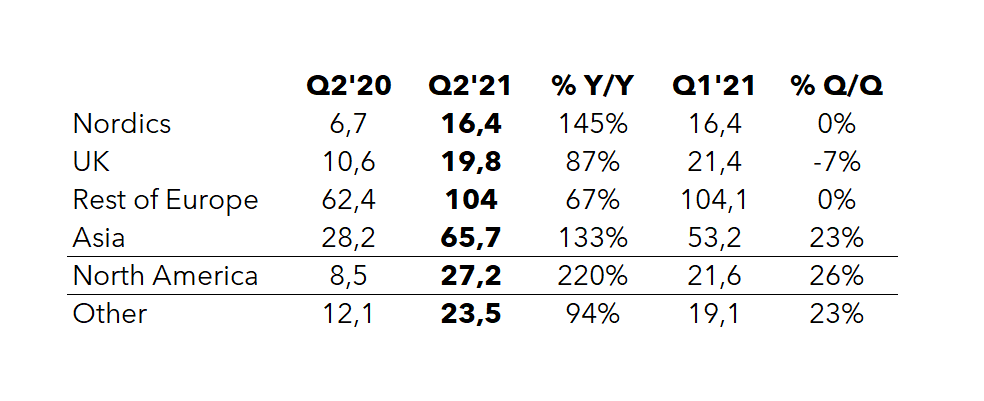

*North America +220%

*Asia +133%

*Live +59%

*RNG -2%

EBITDA +115%

*marg. 68.0% (63.2)

EBIT +110%

*marg. 60.7% (57.8)

Net Profit +105%

*marg. 56.3% (54.9)

EPS +75%

Revenue +100%

*North America +220%

*Asia +133%

*Live +59%

*RNG -2%

EBITDA +115%

*marg. 68.0% (63.2)

EBIT +110%

*marg. 60.7% (57.8)

Net Profit +105%

*marg. 56.3% (54.9)

EPS +75%

Geo Split:

Martin expects RNG growth to improve in H2

Maintaining the record high EBITDA margin

Game launches

Further studio expansion in current locations + "new markets like LATAM"

"Only the paranoid survive." - Andy Grove

"After the end of the period, the new Michigan studio was approved and is ready for launch"

Online (Live) Casino Market

The number of bet spots from end users amounted to 17.5 billion (11.9), +47% y/y

• • •

Missing some Tweet in this thread? You can try to

force a refresh