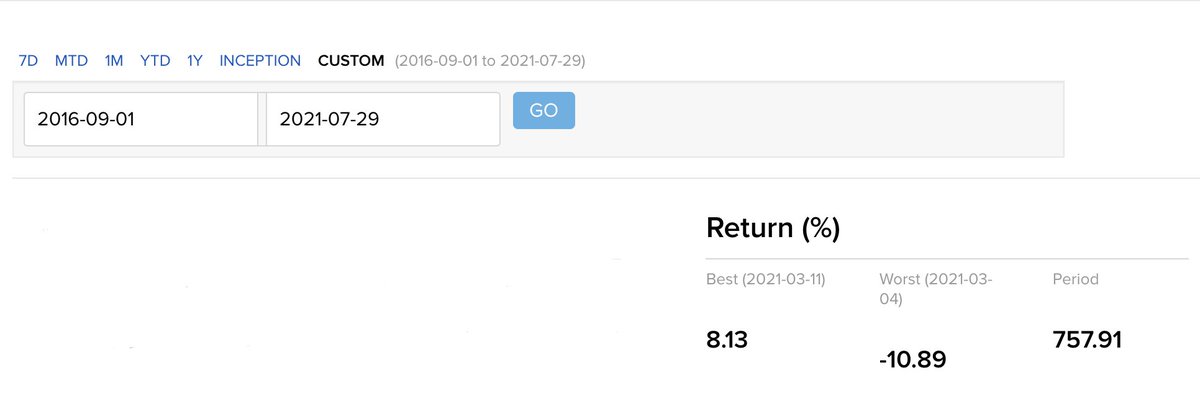

Updated portfolio -

$ADYEY $AGC $CRWD $DLO $DOCU $GLBE $LSPD

$MELI $MTTR $OKTA $PATH $PLTR $QELL $SE $SHOP $SNOW $TWLO $U $UPST $ZI #ES_F

Top 5 --> 1) $MELI 2) $SE 3) $PLTR 4) $U 5) $GLBE

$ADYEY $AGC $CRWD $DLO $DOCU $GLBE $LSPD

$MELI $MTTR $OKTA $PATH $PLTR $QELL $SE $SHOP $SNOW $TWLO $U $UPST $ZI #ES_F

Top 5 --> 1) $MELI 2) $SE 3) $PLTR 4) $U 5) $GLBE

Changes -

This month, I've further removed the lower conviction stocks from my portfolio, re-invested in Unity, Upstart and increased positions in D-Local, Lightspeed, Okta, Palantir and Snowflake.

If my companies keep executing, intend to own shares for the long haul.

This month, I've further removed the lower conviction stocks from my portfolio, re-invested in Unity, Upstart and increased positions in D-Local, Lightspeed, Okta, Palantir and Snowflake.

If my companies keep executing, intend to own shares for the long haul.

Sold -

$AFTPY -> Acquired by Square

$FVRR -> LinkedIn marketplace launch threat

$ROKU -> Intensifying competition, int'l is tough

$SNAP -> Doubts about s. media's moat

These companies may end up doing very well, but I just don't like doubt/uncertainty. Prefer simple stories.

$AFTPY -> Acquired by Square

$FVRR -> LinkedIn marketplace launch threat

$ROKU -> Intensifying competition, int'l is tough

$SNAP -> Doubts about s. media's moat

These companies may end up doing very well, but I just don't like doubt/uncertainty. Prefer simple stories.

• • •

Missing some Tweet in this thread? You can try to

force a refresh