🇺🇸🏦 America's Shadow Banks

With all this Debt Ceiling talk, here's another throwback:

What are shadow banks?

How did they spur the 2008 financial crisis?

"But shadow banks aren't a thing anymore, right?"

Wrong.

Today they underwrite more debt than regular banks.

Thread👇

With all this Debt Ceiling talk, here's another throwback:

What are shadow banks?

How did they spur the 2008 financial crisis?

"But shadow banks aren't a thing anymore, right?"

Wrong.

Today they underwrite more debt than regular banks.

Thread👇

1/ If it looks like a duck & quacks like a duck...

Is it a 🦆?

If a company moves money around and lends to other companies even (especially) when real banks refuse, then is it a bank?

In 2007, economist Paul McCulley named these things "shadow banks."

The name stuck around.

Is it a 🦆?

If a company moves money around and lends to other companies even (especially) when real banks refuse, then is it a bank?

In 2007, economist Paul McCulley named these things "shadow banks."

The name stuck around.

2/ What do they do?

4 things.

- Transfer credit risk: from loan originator to 3rd party

- Lever up: borrow $ to invest & make more $

- Transform liquidity: use cash-like liabilities to buy hard-to-sell assets

- Transform maturity: use short-term deposits to fund long term loans

4 things.

- Transfer credit risk: from loan originator to 3rd party

- Lever up: borrow $ to invest & make more $

- Transform liquidity: use cash-like liabilities to buy hard-to-sell assets

- Transform maturity: use short-term deposits to fund long term loans

Commercial banks do all 4 things too.

BUT the difference is: shadow banks aren't regulated, can't borrow from Fed in an emergency & deposits aren't insured.

So:

They can transfer credit risk (& lie about risk magnitude)

They can lever up (way beyond Dodd Frank's min cap reqs)

BUT the difference is: shadow banks aren't regulated, can't borrow from Fed in an emergency & deposits aren't insured.

So:

They can transfer credit risk (& lie about risk magnitude)

They can lever up (way beyond Dodd Frank's min cap reqs)

They can lend to high risk businesses (whose credit ratings are too low for most regular banks to touch).

They fall like dominos in a bank run (because no access to emergency cash).

And most importantly, they used to be owned by the regular banks themselves.

They fall like dominos in a bank run (because no access to emergency cash).

And most importantly, they used to be owned by the regular banks themselves.

3/ Birth of shadow banking

Flash back to the 80s.

“Junk bonds" are the old NFTs.

Traditional banks won't lend to companies w/ less than blue-chip credit ratings. But meanwhile the street's investors are all hungry for yield.

Step in, new middleman. Make the match happen.

Flash back to the 80s.

“Junk bonds" are the old NFTs.

Traditional banks won't lend to companies w/ less than blue-chip credit ratings. But meanwhile the street's investors are all hungry for yield.

Step in, new middleman. Make the match happen.

So these rando non-bank entities would come in, fund the low-credit corporates at some ridiculously high interest rate (read: high yield for investors), then sell them to the street as super juicy junk bonds.

Now flash forward to the 90s.

Time to land & expand.

They expanded into home mortgages & other consumer debt — auto loans, student loans, credit card debt — which they bought from banks, packaged together and sold to investors as bond-like securities.

The rest is history.

Time to land & expand.

They expanded into home mortgages & other consumer debt — auto loans, student loans, credit card debt — which they bought from banks, packaged together and sold to investors as bond-like securities.

The rest is history.

4/ Role in the 2008 crisis

As long as shadow banks ultimately put their funds into "safe" investments, everything should be ok.

So what went wrong in 2008?

The investments were garbage.

They were garbage posing as AA ratings w/ the help of S&P and Moody's.

But they were 💩.

As long as shadow banks ultimately put their funds into "safe" investments, everything should be ok.

So what went wrong in 2008?

The investments were garbage.

They were garbage posing as AA ratings w/ the help of S&P and Moody's.

But they were 💩.

Most of you have seen the Big Short.

TLDR: Investors got skittish and suddenly a bunch wanted to pull out. To repay these investors, shadow banks had to sell assets. These “fire sales” reduced the value of those assets. Book values on bank balance sheets tanked. Banks collapsed.

TLDR: Investors got skittish and suddenly a bunch wanted to pull out. To repay these investors, shadow banks had to sell assets. These “fire sales” reduced the value of those assets. Book values on bank balance sheets tanked. Banks collapsed.

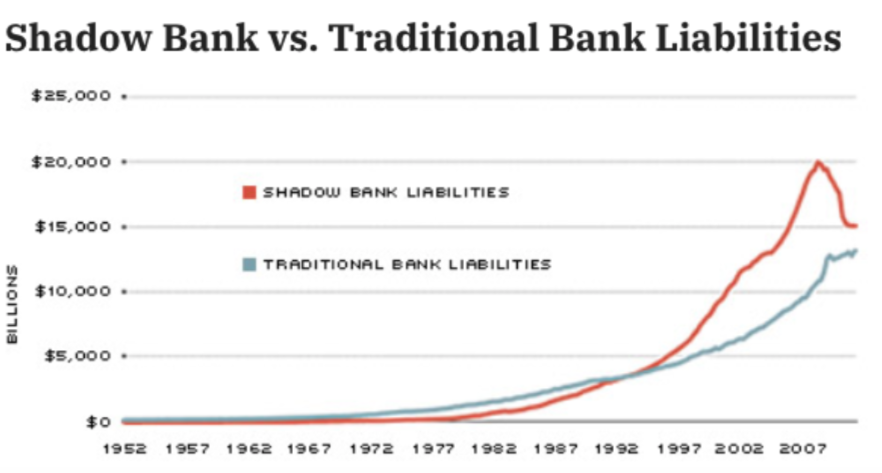

5/ Are shadow banks still a thing TODAY?

Yep.

In fact they're an even bigger thing now:

In 2007 the global shadow banking sector was $62 trillion.

In 2011 it reached $67T.

In 2009, non-banking loans accounted for only 25% of all US loans.

In 2018, they account for 45%.

Yep.

In fact they're an even bigger thing now:

In 2007 the global shadow banking sector was $62 trillion.

In 2011 it reached $67T.

In 2009, non-banking loans accounted for only 25% of all US loans.

In 2018, they account for 45%.

6/ Why?

Why are shadow banks still ON THE RISE?

CLOs.

Because investors forever want YIELD (esp in QE-induced low interest rate environments) and CLOs offer yield.

Why are shadow banks still ON THE RISE?

CLOs.

Because investors forever want YIELD (esp in QE-induced low interest rate environments) and CLOs offer yield.

Post-2008, shadow bankers shifted from mortgages to business lending, using the same securitization process to buy and package leveraged loans into CLOs.

Investors wanted them & highly-levered businesses needed them.

What could possibly go wrong?

Investors wanted them & highly-levered businesses needed them.

What could possibly go wrong?

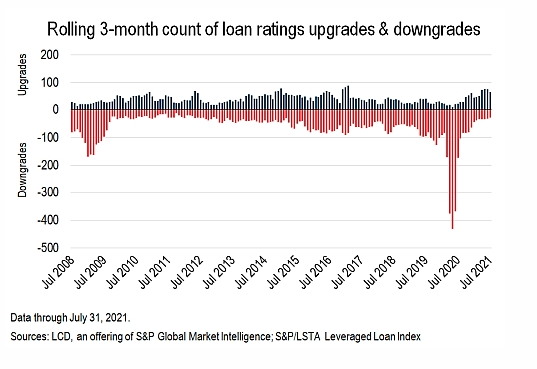

7/ New Problems?

Lately, the CLO market has seen a huge wave of downgrades. Credit quality has deteriorated.

Deja vu?

The trend started in 2012 & has worsened ever since.

Diagram below shows U.S. leveraged loan downgrades hitting new highs in June 2020.

At 3X 2008 levels.

Lately, the CLO market has seen a huge wave of downgrades. Credit quality has deteriorated.

Deja vu?

The trend started in 2012 & has worsened ever since.

Diagram below shows U.S. leveraged loan downgrades hitting new highs in June 2020.

At 3X 2008 levels.

8/ What now?

Ok so are we screwed? Is this gonna be a replay of 2008?

According to the Fed: No.

Ok so are we screwed? Is this gonna be a replay of 2008?

According to the Fed: No.

What's different and why are we "safe" this time?

- Post- Dodd Frank, the US banking system is much better capitalized. Banks are passing stress tests & got enough RWAs.

- Bank runs are "structurally difficult" now, minimizing fire sale risk.

- Household debt < household income.

- Post- Dodd Frank, the US banking system is much better capitalized. Banks are passing stress tests & got enough RWAs.

- Bank runs are "structurally difficult" now, minimizing fire sale risk.

- Household debt < household income.

But are we really safe?

Before writing off the American debt problem as a complete non-issue, let's take another look at the parallels btw '08 & today:

Before writing off the American debt problem as a complete non-issue, let's take another look at the parallels btw '08 & today:

- As before, growth in lending is driven by investors’ search for yield rather than borrowers need for new capital

- As before, lending standards are ever-loosening, first at the shadow banks and now at regulated banks too (who are anxious to compete & claw back market share)

- As before, lending standards are ever-loosening, first at the shadow banks and now at regulated banks too (who are anxious to compete & claw back market share)

If you enjoyed this piece you can read more about shadow banks here:

imf.org/external/pubs/…

stlouisfed.org/publications/r…

And for more educational threads on all things finance, check out my previous deep-dives here:

Happy weekend!

imf.org/external/pubs/…

stlouisfed.org/publications/r…

And for more educational threads on all things finance, check out my previous deep-dives here:

https://twitter.com/FabiusMercurius/status/1416550699173773314

Happy weekend!

• • •

Missing some Tweet in this thread? You can try to

force a refresh