For a while now, China rather than the United States has had the world's largest GDP in terms of purchasing power parity, even though the US still has the highest nominal GDP. en.wikipedia.org/wiki/List_of_c…

Some people think PPP is less accurate than nominal GDP, but for example, China has way more electricity consumption, 3x as many skyscrapers, more commodity imports, and more industrial capacity, than the US. Makes sense, given how big their population is.

China also surpassed the US a long time ago as being the largest trading partner for majority of countries in the world.

China has weaker geography, weaker global influence (including language of global business), weaker military, and lower nominal GDP than the US, but the latter two are increasing in size faster than the US.

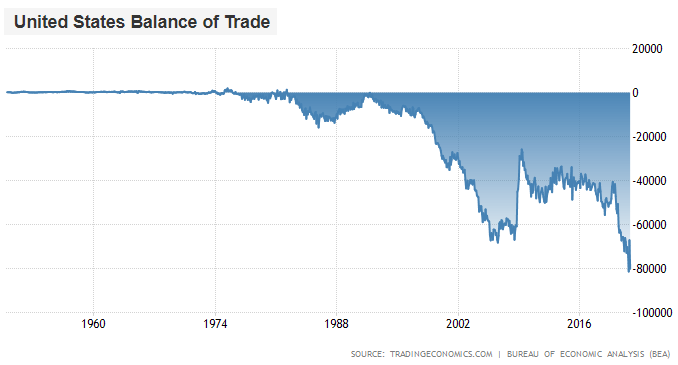

Meanwhile, the US has a rapidly declining NIIP caused by a structural trade deficit and capital surplus which is unsustainable at this rate. It's ironically in large part due to putting the Treasury security at the heart of the global reserve system.

ft.com/content/698995…

ft.com/content/698995…

• • •

Missing some Tweet in this thread? You can try to

force a refresh