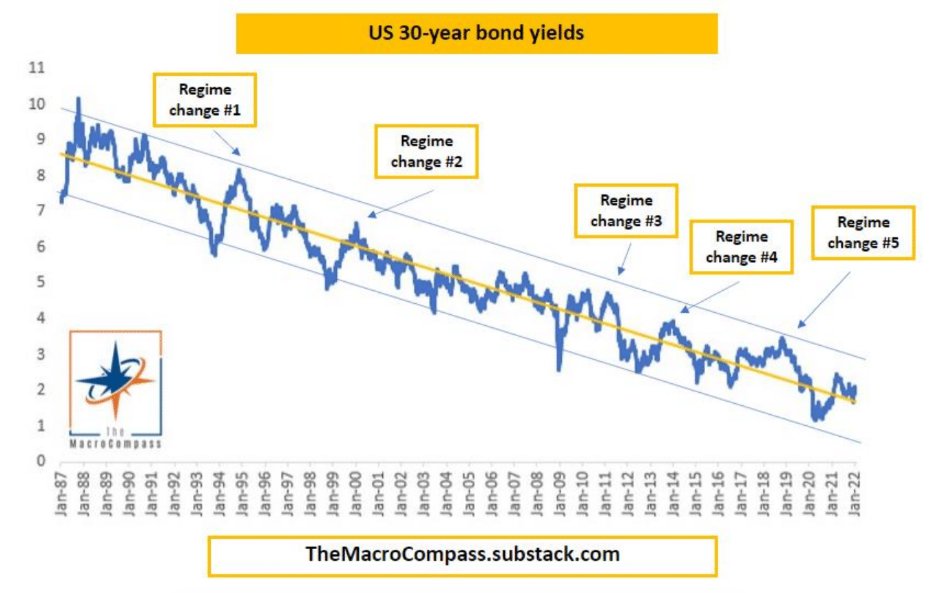

What if I am wrong in my secular bond bullish thesis?

What if this time is REALLY a ''regime change''?

Running a large portfolio, I learnt that coherently challenging your own highest conviction macro thesis is a great exercise to do: tough, but very useful.

Challenge me.

1/7

What if this time is REALLY a ''regime change''?

Running a large portfolio, I learnt that coherently challenging your own highest conviction macro thesis is a great exercise to do: tough, but very useful.

Challenge me.

1/7

Since I started managing money professionally, I had to endure at least 3-4 ''this time is different'' episodes: people would argue rates were going higher, big times higher.

2010-2011 QE = money printing

2013 taper tantrum

2018 rates to 5%+

2021-2022 fiscal paradigm change

2/

2010-2011 QE = money printing

2013 taper tantrum

2018 rates to 5%+

2021-2022 fiscal paradigm change

2/

I stand behind my bond bullish secular trend until facts change.

What facts?

- Declining rates of potential growth: low population growth and ageing society

- Stagnant productivity: capital misallocation & co.

- Technological trends

- Growing tally of unproductive debt

3/

What facts?

- Declining rates of potential growth: low population growth and ageing society

- Stagnant productivity: capital misallocation & co.

- Technological trends

- Growing tally of unproductive debt

3/

I described the drivers of real rates in my latest article on The Macro Compass

My conviction here is high as turning around demographics trends would take a gigantic effort

A productivity boost? Could be, but it needs to permeate the entire economy

themacrocompass.substack.com/p/real-yields?…

4/

My conviction here is high as turning around demographics trends would take a gigantic effort

A productivity boost? Could be, but it needs to permeate the entire economy

themacrocompass.substack.com/p/real-yields?…

4/

Sure, but nominal yields can be decomposed in real yields + inflation expectations

Perhaps even if real rates continue to drop or remain very low, inflation expectations can become de-anchored on the upside and more than offset that

In that case, nominal yields would rise

5/

Perhaps even if real rates continue to drop or remain very low, inflation expectations can become de-anchored on the upside and more than offset that

In that case, nominal yields would rise

5/

Actually, also inflation risk premium would need to reprice higher and that would lead to steeper curves as well as investors demand a larger premium to own long-end bonds in that scenario.

I believe the distribution of future CPI outcomes has shifted a bit right, yes...

6/

I believe the distribution of future CPI outcomes has shifted a bit right, yes...

6/

...Net Zero Emissions & a shrinking labor force leading to higher wage bargaining power in certain sectors move the needle a bit.

But is it a regime change?

The structural headwinds are so big.

Convince me otherwise.

7/7

But is it a regime change?

The structural headwinds are so big.

Convince me otherwise.

7/7

• • •

Missing some Tweet in this thread? You can try to

force a refresh