1/With #Shanghai out of lockdown & COVID cases far lower than the April peak, is the Chinese #economy out of the woods? Not really. Any rebound in 3Q will be illusory as the underlying economy remains weak. @hzsong makes the case in his macro outlook: macropolo.org/analysis/3q202…

2/For one, consumption remains weak. It is sensitive to even modest lockdowns like those in #Beijing, and these smaller-scale lockdowns will likely be repeated across the country.

3/Second, Beijing continues to resist using the bazooka when it comes to stimulus. The recent news on #infrastructure spending won’t do much for growth. If anything, it will likely do the opposite and withdraw stimulus in 3Q: macropolo.org/chinese-econom…

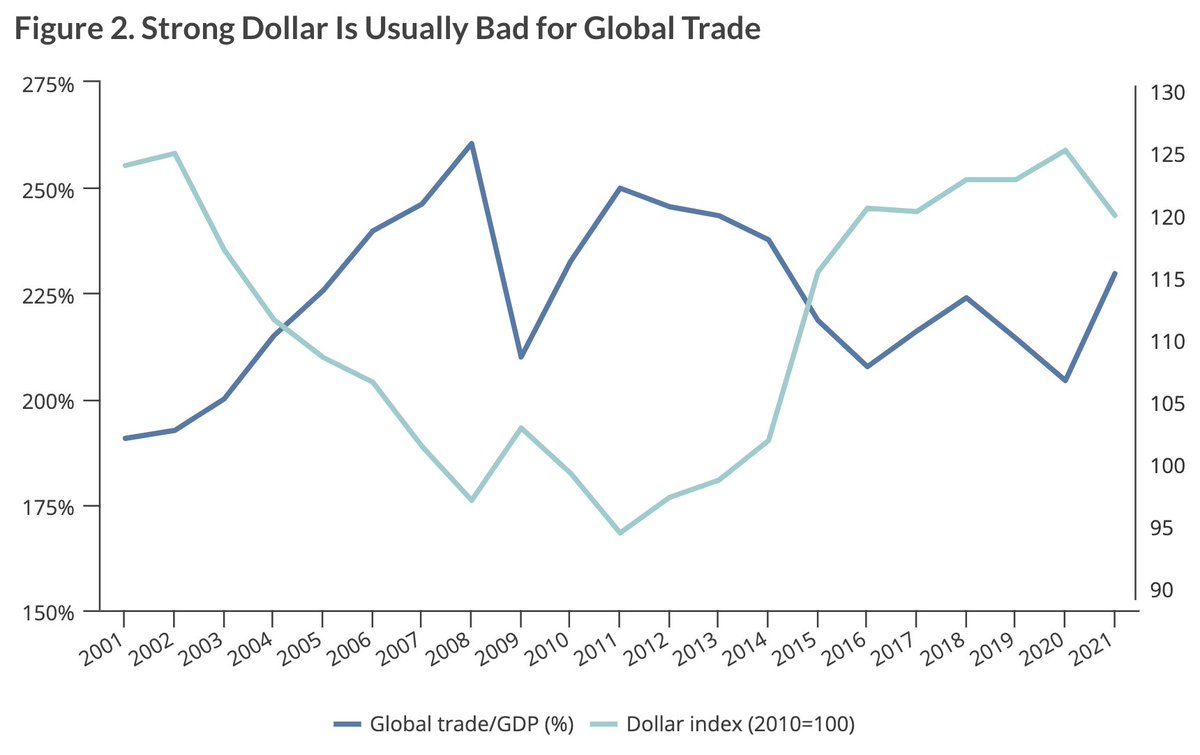

4/Third, exports likely won’t save the day again. The US dollar has appreciated by 5% this year because of the Fed’s tightening. Historically, this spells bad news for global #trade and Chinese goods.

5/The bottom line is that Zero COVID remains the main variable in China’s growth performance, and that variable will likely remain in place until the end of the year. So expect a Chinese economy that will be in a mild recession until early 2023. macropolo.org/analysis/3q202…

• • •

Missing some Tweet in this thread? You can try to

force a refresh