RBI is playing with FIRE abt intervention in the FWD USDINR market…. Your sins with come back to haunt you … unlike Equities which can be manipulated for years, you can’t do that same with FX and RATES

@RBI EXTENT Of Forward Intervention is #MindBoggling in one #CHART. You can see INR 2yr & 3yr Implied Forward Premium is 7.8% & 7.59% Respectively

& has Actually Increased while the near term 12 Month INR forward is just 2.5%. This kind of DIVERGENCE is SCARY.#RETWEET #MUSTREAD

& has Actually Increased while the near term 12 Month INR forward is just 2.5%. This kind of DIVERGENCE is SCARY.#RETWEET #MUSTREAD

This is called Timing !!

My tweet was at 1.26pm IST. See the INTRADAY on the INR today … the breakdown happens at 1.57pm IST

I guess I was just lucky I guess since there was NO MOVEMENT in the DXY or regional currencies like the JPY (see Intraday Charts of JPY, INR, DXY)

My tweet was at 1.26pm IST. See the INTRADAY on the INR today … the breakdown happens at 1.57pm IST

I guess I was just lucky I guess since there was NO MOVEMENT in the DXY or regional currencies like the JPY (see Intraday Charts of JPY, INR, DXY)

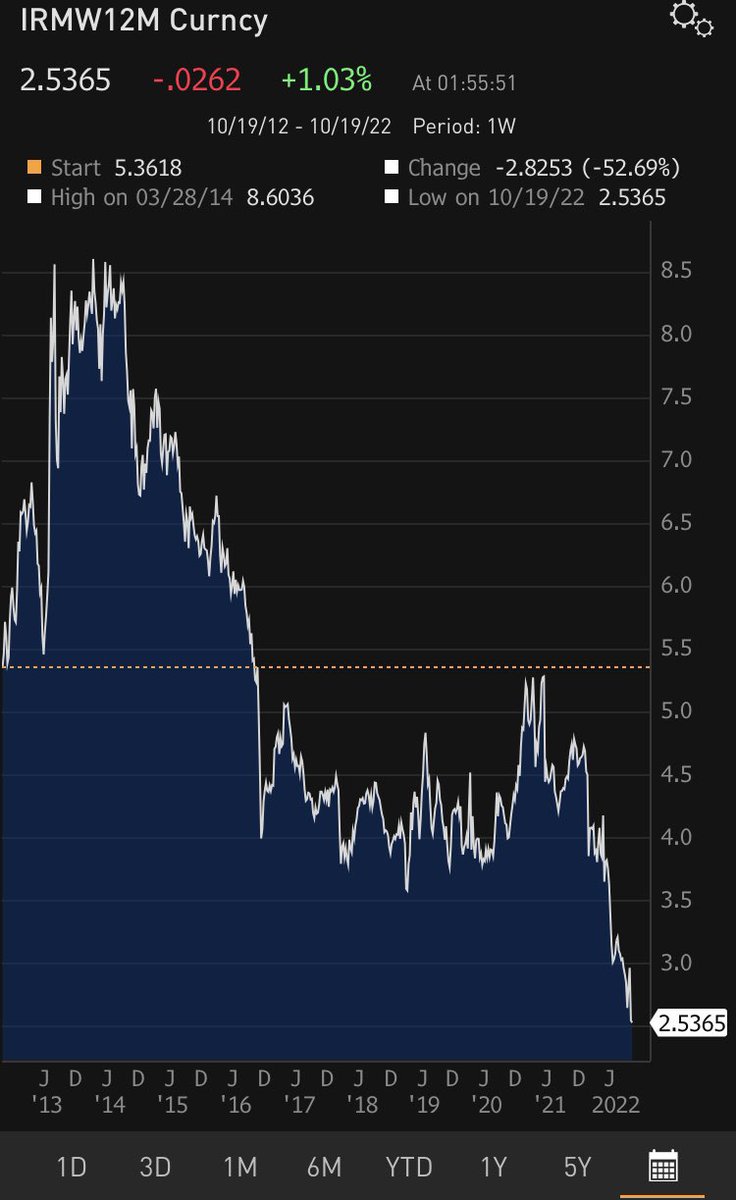

AN UPDATE ON THE #INR #USDINR. DANGEROUS GAME!!

@SaurabhDJosh pointed out that INR onshore 12mth fwd has fallen to just 2.18%.... the only last time this happened was in May 2010 and Sep-2011. In both these scenarios, Off-shore NDF 12 mth fwd Prems also contracted along onshore

@SaurabhDJosh pointed out that INR onshore 12mth fwd has fallen to just 2.18%.... the only last time this happened was in May 2010 and Sep-2011. In both these scenarios, Off-shore NDF 12 mth fwd Prems also contracted along onshore

But this time, as you can see, the ONSHORE 12 mth USDINR fwd is contracting (2.18%) while the Off-shore NDF 12 month fwd is expanding to 2013 #TaperTantrum levels (8.2%).

Why is this dangerous? IF I WERE an importer, RBI has effectively made my 12 month fwd IMPORTS super cheap

Why is this dangerous? IF I WERE an importer, RBI has effectively made my 12 month fwd IMPORTS super cheap

As an importer, I would be signing on more such IMPORT CONTRACTS & promise to pay the exporter over that time frame of 12 months. EFFECTIVELY, RBI is encouraging more & MORE IMPORTS over the next 12 mths when it should be encouraging the opposite "Making Imports expensive"

Meanwhile, EXPORTERS will be encouraged NOT TO HEDGE making the entire market very very illiquid.

@RBI in my view is playing a very dangerous game. Its run out of bullets and BUYING TIME. Its providing Speculators a reason to USE #INR as the #CARRYTRADE. 🤔

@RBI in my view is playing a very dangerous game. Its run out of bullets and BUYING TIME. Its providing Speculators a reason to USE #INR as the #CARRYTRADE. 🤔

Something will SNAP... if @RBI wins, then INR will rally like a coiled spring. But if @RBI loses, the INR will just crash.

ITS IMPORTANT that FX Speculators start viewing #Indias Disclosed FX RESERVES with a pinch of Salt. They have to ADJUST this with the FX Forwards.

ITS IMPORTANT that FX Speculators start viewing #Indias Disclosed FX RESERVES with a pinch of Salt. They have to ADJUST this with the FX Forwards.

• • •

Missing some Tweet in this thread? You can try to

force a refresh