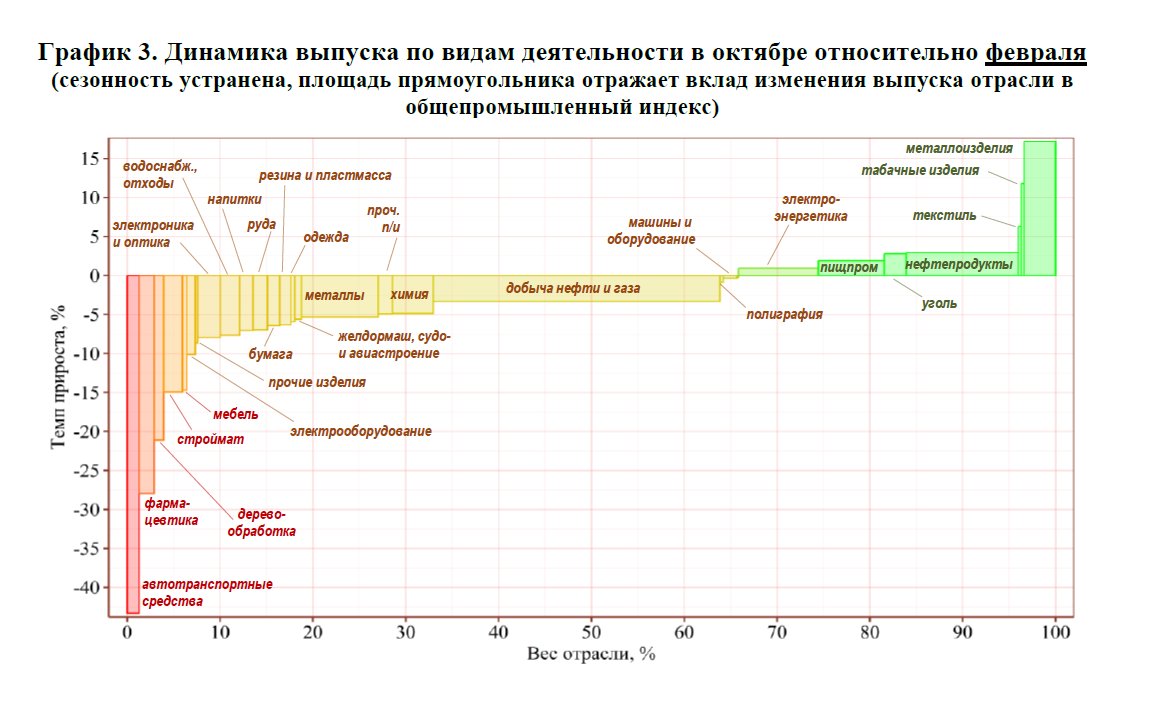

How #war production is boosting the Russian #economy: This chart shows changes in output relative to February 2022. The big green box on the very right: Weapons production! Textile and food also in the green, probably also war-related. 1/2

#Oil products is another relatively large green box. Russian oil companies were refining as much crude as possible, because refined products were easier to export than crude. This is about to change on Sunday, when the oil products embargo kicks in. 2/2

Source of the chart: forecast.ru/_ARCHIVE/Anali…

• • •

Missing some Tweet in this thread? You can try to

force a refresh