Which date of the month is the best to do your SIP?

Some say it’s the start of the month.

Some say it’s the last Thu of the month, as markets are volatile due to F&O settlements.

We checked data for the first & last week. The returns were similar.

Is there a better date? A 🧵

Some say it’s the start of the month.

Some say it’s the last Thu of the month, as markets are volatile due to F&O settlements.

We checked data for the first & last week. The returns were similar.

Is there a better date? A 🧵

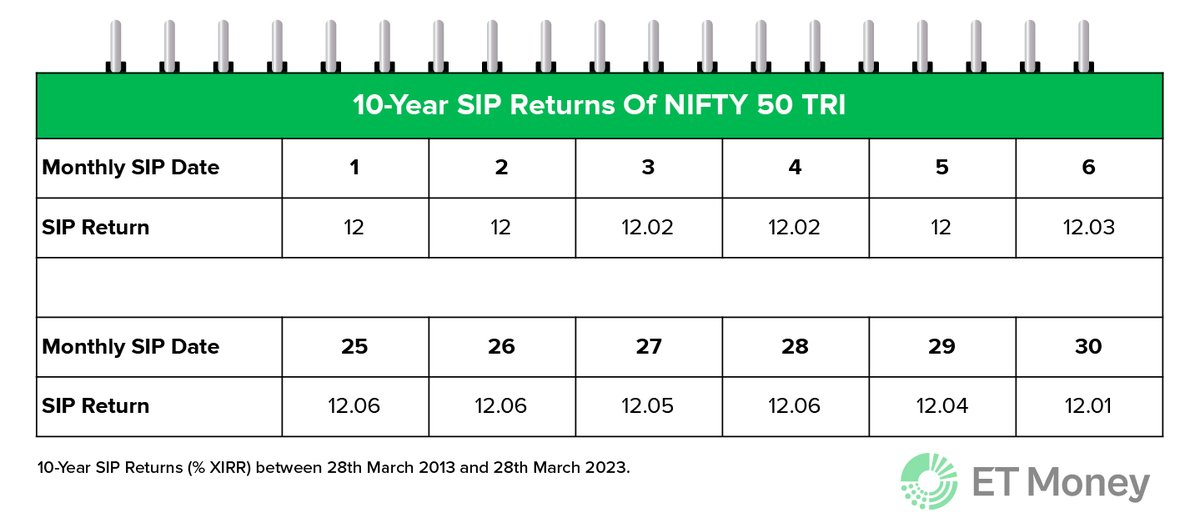

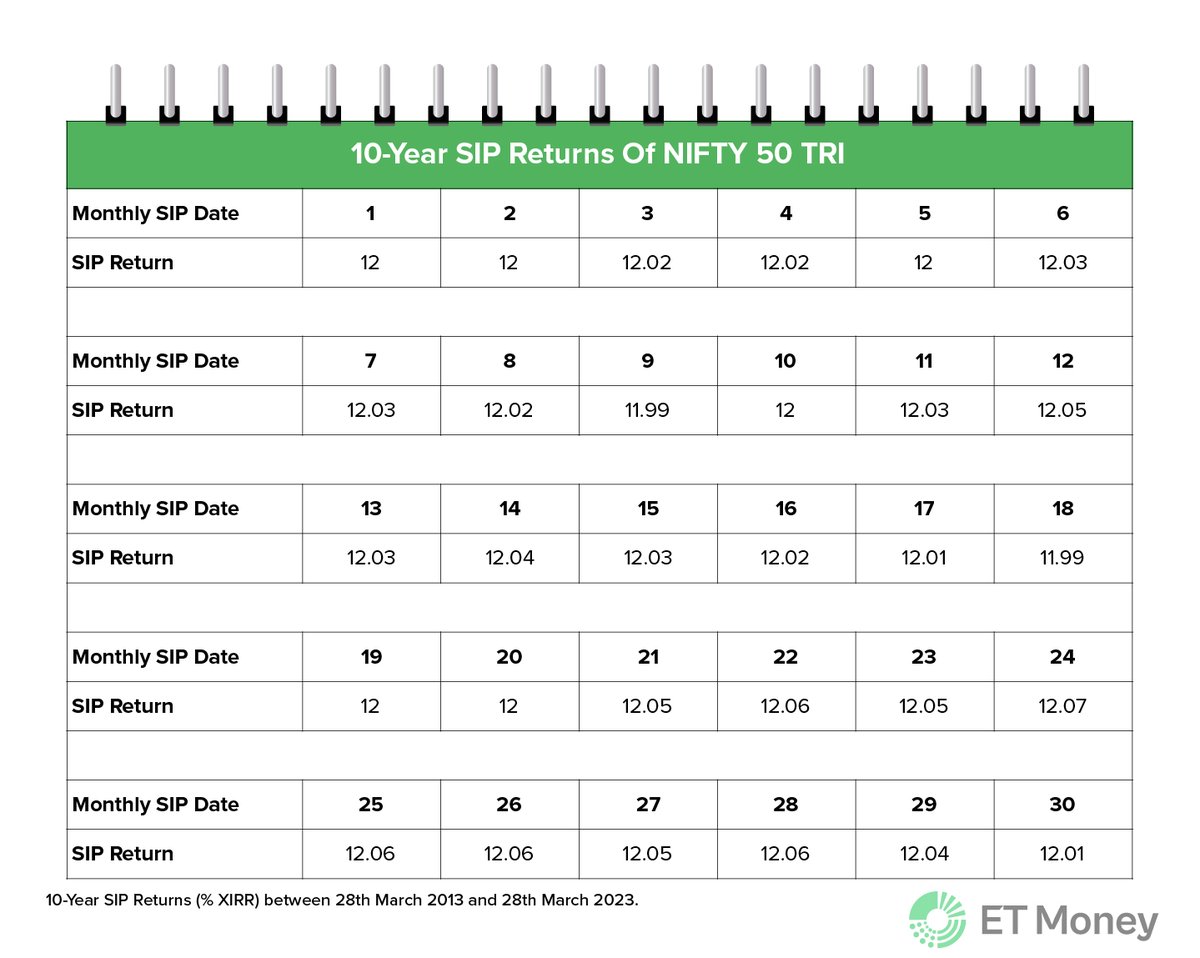

We looked at the #NIFTY50 TRI returns for the last 10 years

Over the last decade, there was hardly any difference in SIP returns scheduled on different dates of the month.

Details in the image. 👇

Over the last decade, there was hardly any difference in SIP returns scheduled on different dates of the month.

Details in the image. 👇

The highest return was 12.07% (on the 24th of every month)

The lowest returns turned out to be 11.99% (9th & 18th)

Overall, there was not much difference, irrespective of the date you picked.

But what about mid-cap & small-cap indices that are more volatile than large-caps?

The lowest returns turned out to be 11.99% (9th & 18th)

Overall, there was not much difference, irrespective of the date you picked.

But what about mid-cap & small-cap indices that are more volatile than large-caps?

We checked the 10-year SIP returns of NIFTY Midcap 150.

The trend was in line with its large-cap counterpart.

The highest return was 15.85% & the lowest return was 16%. (Check image)

So, hardly there’s any difference.

The trend was in line with its large-cap counterpart.

The highest return was 15.85% & the lowest return was 16%. (Check image)

So, hardly there’s any difference.

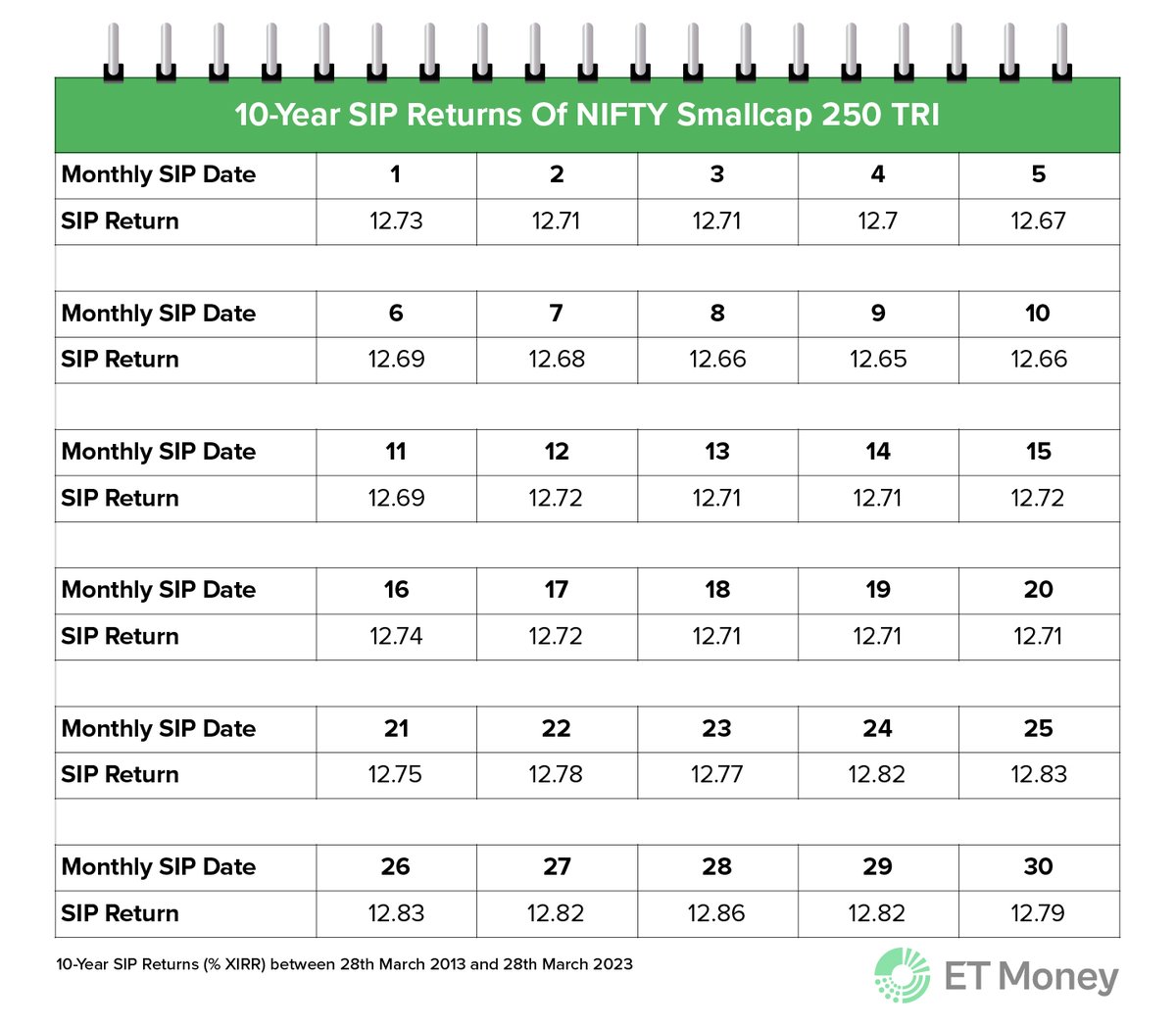

Even in the small-cap space, the trend was more or less similar.

The difference between the highest and lowest return was barely 20 basis points.

Check the table below.

The difference between the highest and lowest return was barely 20 basis points.

Check the table below.

If you are still confused about which date to pick, here’s a simple solution.

Pick a date at your convenience

For instance, if you have a regular income, you can set your SIP date within 2-3 days of receiving your salary.

Hope this helps.

Pick a date at your convenience

For instance, if you have a regular income, you can set your SIP date within 2-3 days of receiving your salary.

Hope this helps.

We put a lot of effort into creating such informative threads.

So, if you find this useful, show some love. ❤️

Please like, share, and retweet the first tweet.

For more threads, follow us.

Also, click on the bell icon in the profile section so you don't miss any threads.🔔

So, if you find this useful, show some love. ❤️

Please like, share, and retweet the first tweet.

For more threads, follow us.

Also, click on the bell icon in the profile section so you don't miss any threads.🔔

• • •

Missing some Tweet in this thread? You can try to

force a refresh