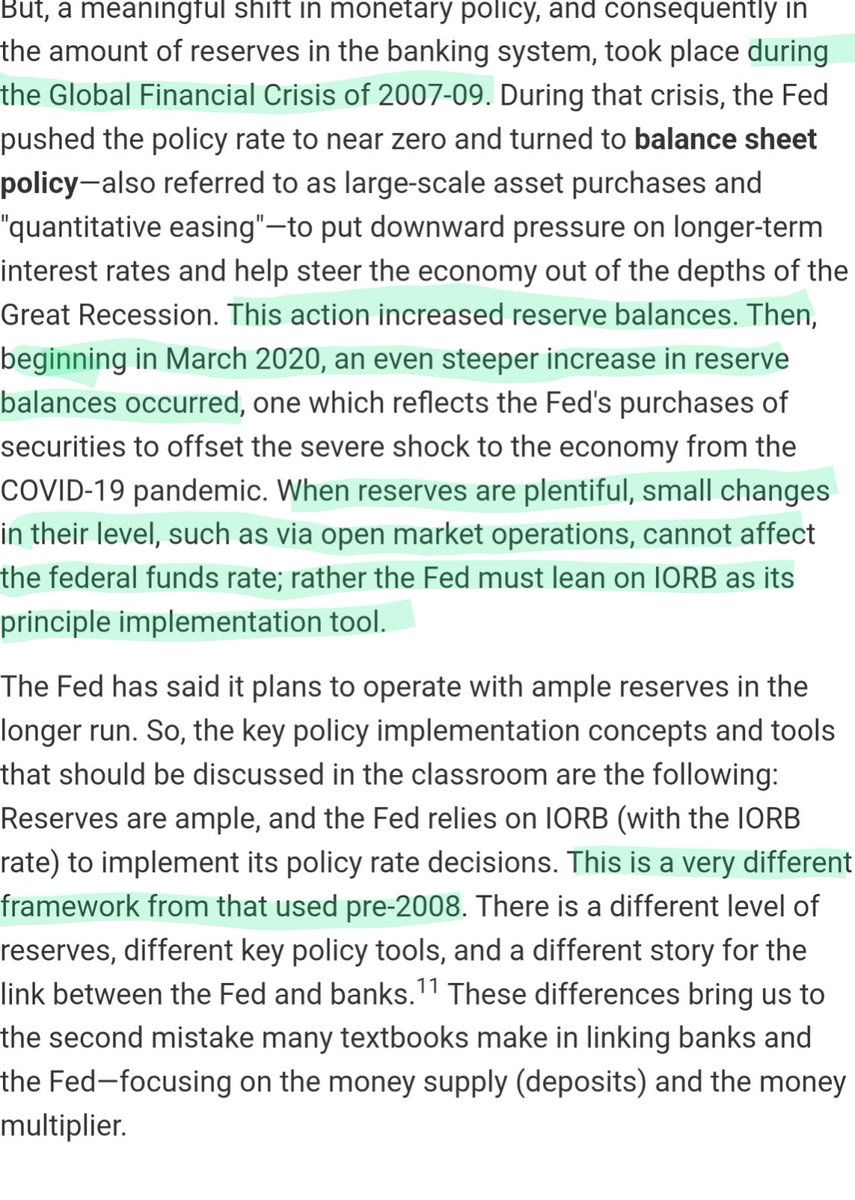

1/8

"artists can no longer appear real on their own" – a perverse notion of centralized platforms becoming gatekeepers for identity/authenticity verification...?

eh, the problem was that anyone thought appearance was reality to being with...

drorpoleg.com/artificial-mon… #AI #LLM

"artists can no longer appear real on their own" – a perverse notion of centralized platforms becoming gatekeepers for identity/authenticity verification...?

eh, the problem was that anyone thought appearance was reality to being with...

drorpoleg.com/artificial-mon… #AI #LLM

/2

...that's the idea behind @benthompson's 'Zero Trust Authenticity vs castle-and-moat' analogies, e.g.:

Just because a song looks and sounds like Drake doesn't mean it came from Drake – its authenticity must (obviously?) still be verified 👇

medium.com/adventures-in-… #media

...that's the idea behind @benthompson's 'Zero Trust Authenticity vs castle-and-moat' analogies, e.g.:

Just because a song looks and sounds like Drake doesn't mean it came from Drake – its authenticity must (obviously?) still be verified 👇

medium.com/adventures-in-… #media

/3

...but that's not obvious to everyone:

to whatever extent there's a crisis in the authenticity and verification of (mis/dis)information, it's concentrated among non-internet natives – i.e. Millennials/Zoomers aren't the problem 👇

stratechery.com/2020/zero-trus… #boomers #content

...but that's not obvious to everyone:

to whatever extent there's a crisis in the authenticity and verification of (mis/dis)information, it's concentrated among non-internet natives – i.e. Millennials/Zoomers aren't the problem 👇

stratechery.com/2020/zero-trus… #boomers #content

/4

...my point isn't inter-generational spats; it's creators/artists/brands growing more empowered than ever, with their owned-and-operated destinations (e.g. O&O websites and to some extent social followings) becoming ever more important primary sources for verification

#AI

...my point isn't inter-generational spats; it's creators/artists/brands growing more empowered than ever, with their owned-and-operated destinations (e.g. O&O websites and to some extent social followings) becoming ever more important primary sources for verification

#AI

/5

...farbeit from @drorpoleg's "it makes the most charismatic people dependent on corporate platforms in order to exist", it goes differently (doubly) for incumbent creators/artists/brands as opposed to new entrants/upstarts 👇

medium.com/adventures-in-…

...farbeit from @drorpoleg's "it makes the most charismatic people dependent on corporate platforms in order to exist", it goes differently (doubly) for incumbent creators/artists/brands as opposed to new entrants/upstarts 👇

medium.com/adventures-in-…

/6

...for more on that dichotomy, see:

🅰️ "differentiated [stars who] are destinations unto themselves" and "broad scale or niche focus" and "discovery" problem (medium.com/swlh/the-athle…)

🅱️ "The Four Winds of Modern Media" (medium.com/adventures-in-…)

...for more on that dichotomy, see:

🅰️ "differentiated [stars who] are destinations unto themselves" and "broad scale or niche focus" and "discovery" problem (medium.com/swlh/the-athle…)

🅱️ "The Four Winds of Modern Media" (medium.com/adventures-in-…)

/7

...TLDR:

Kids these days (😏) know how to and do verify whether that hot new song is Drake himself; licensed by Drake himself; or generative AI unauthorized by Drake himself – so the content commons aren't dependent on platforms as "artificial monopolies" of authentication

...TLDR:

Kids these days (😏) know how to and do verify whether that hot new song is Drake himself; licensed by Drake himself; or generative AI unauthorized by Drake himself – so the content commons aren't dependent on platforms as "artificial monopolies" of authentication

🏁/8

...TLDR (cont'd):

but that doesn't mean that platforms cannot and should not facilitate authentication/verification/identification as a service for producers and consumers alike – Trustless Verification can help remove centralized platform risk 👇

...TLDR (cont'd):

but that doesn't mean that platforms cannot and should not facilitate authentication/verification/identification as a service for producers and consumers alike – Trustless Verification can help remove centralized platform risk 👇

https://twitter.com/AnthPB/status/1526292299541536770?s=20

...see also:

• weak opinions weakly held regarding LLM libel, safe harbor, and copyright/fair use

• derivative and transformative works

• digital rights management (DRM) and YouTube ContentID

• AI transformer mechanics and the 4 part fair use test

medium.com/adventures-in-…

• weak opinions weakly held regarding LLM libel, safe harbor, and copyright/fair use

• derivative and transformative works

• digital rights management (DRM) and YouTube ContentID

• AI transformer mechanics and the 4 part fair use test

medium.com/adventures-in-…

• • •

Missing some Tweet in this thread? You can try to

force a refresh