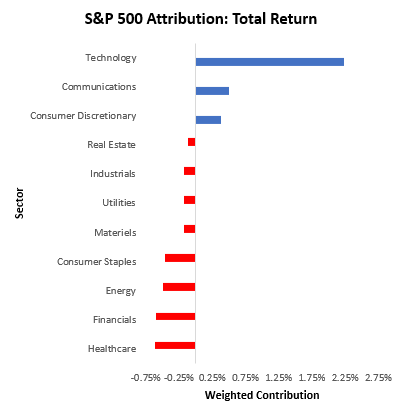

On PMIs

1. Recently, we received new PMI data, which feeds into our PMI composite, whose readings continue to show a weak environment for growth assets (stocks, commodities, & high yield credit). As of the latest available data, our PMI composite now shows a reading of -10.93.

1. Recently, we received new PMI data, which feeds into our PMI composite, whose readings continue to show a weak environment for growth assets (stocks, commodities, & high yield credit). As of the latest available data, our PMI composite now shows a reading of -10.93.

2. This was a sequential deceleration from one month prior and a decline in the three-month trend. PMIs are generally strong directional indicators of where we are in the profit cycle, as PMI respondents manage inventories and orders in response to their outlook on profitability.

3. PMI indicators are typically biased toward the manufacturing sector. While this does indeed make sense since production is largely driven by the manufacturing sector, it is important to also separate these sub-indexes to understand the pervasiveness of the current trend .

4. Currently, our Manufacturing and Services composites are sow readings of -13.7 & -5.9, respectively, signaling consistency within the current trend:

5. Zooming out, we think it is important to note that PMIs have generally been weak, though ISM and S&P Services PMIs have remained resilient. Nonetheless, 9/11 PMIs we track are negative. We show some of the major PMI indices below:

6. S&P Services has been the strongest of the PMIs, while Empire State Mfg has been the weakest. While services PMIs have shown some resilience, we think it is important to note that the trend in PMI remains lower and cyclical conditions continue to weaken.

7. These conditions do not support taking on #medium-term equity risk, despite recent trends in markets. To illustrate this concept, we show a simple cyclical rotation strategy that leverages our understanding of #cyclical conditions to choose between #equities and #cash.

8. When cyclical conditions are likely to deteriorate, it switches into cash; if not, it stays long the S&P 500. Below we show the performance of the strategy:

9. As we can see above, this strategy has #outperformed equity markets significantly while offering much lower #drawdowns. This strategy can be applied in a #long/ #short fashion as well.

10. Overall, continue to believe that it is not an ideal time to take on equity risk unless you have the ability to change positions on a week-to-week basis. Data will likely continue to deteriorate, and this strategy remains in #cash until it improves.

• • •

Missing some Tweet in this thread? You can try to

force a refresh