Data Driven Trader | Featured on @cnbc_awaaz, @moneycontrolcom & @timesnow

1. Imagine turning $10,775 into $42,000,000 in less than 2 years.

1. Imagine turning $10,775 into $42,000,000 in less than 2 years. 1. Knight Capital wasn’t reckless or inexperienced.

1. Knight Capital wasn’t reckless or inexperienced.

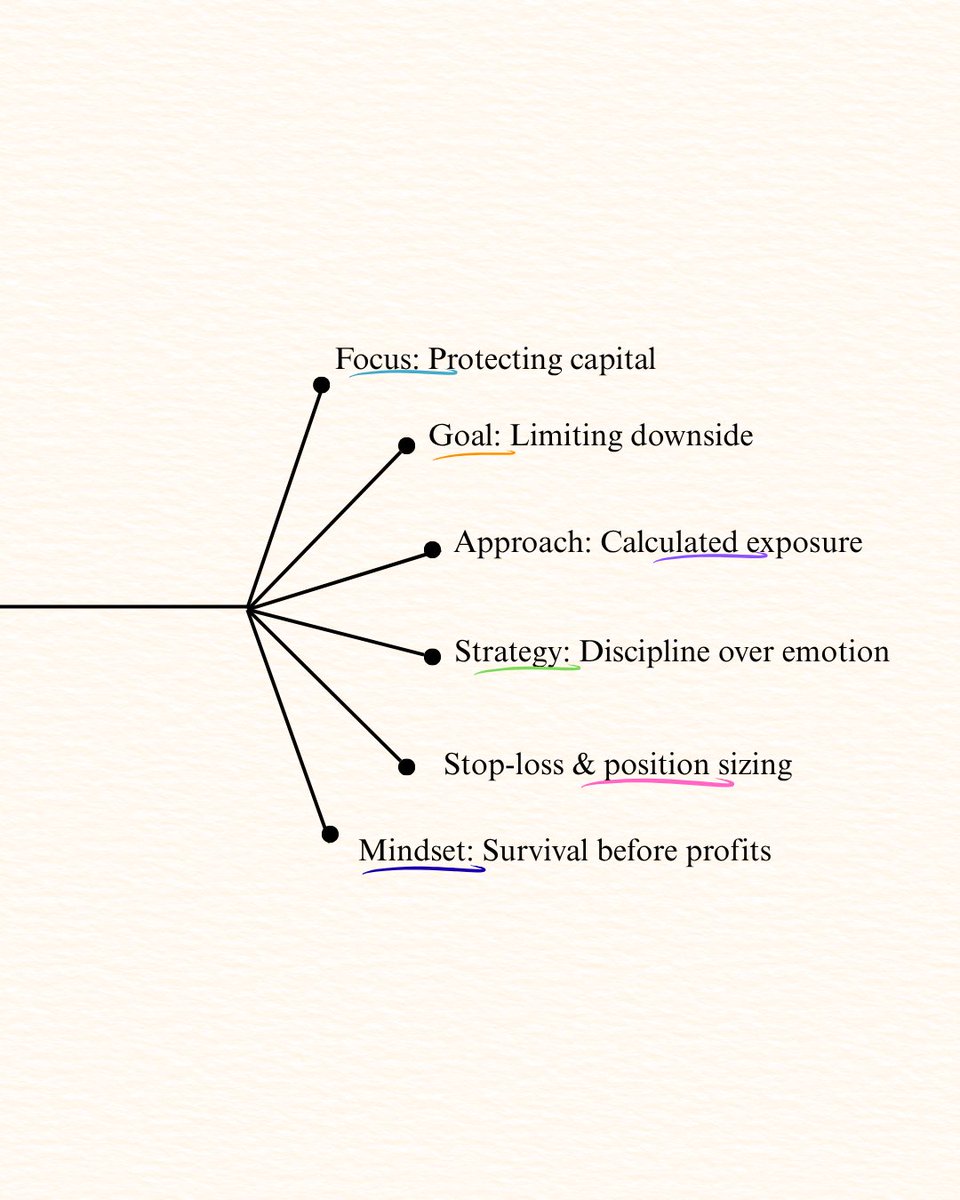

Most traders focus on making money. The pros focus on not losing it. Let’s talk about risk management the unsung hero of trading.

Most traders focus on making money. The pros focus on not losing it. Let’s talk about risk management the unsung hero of trading.

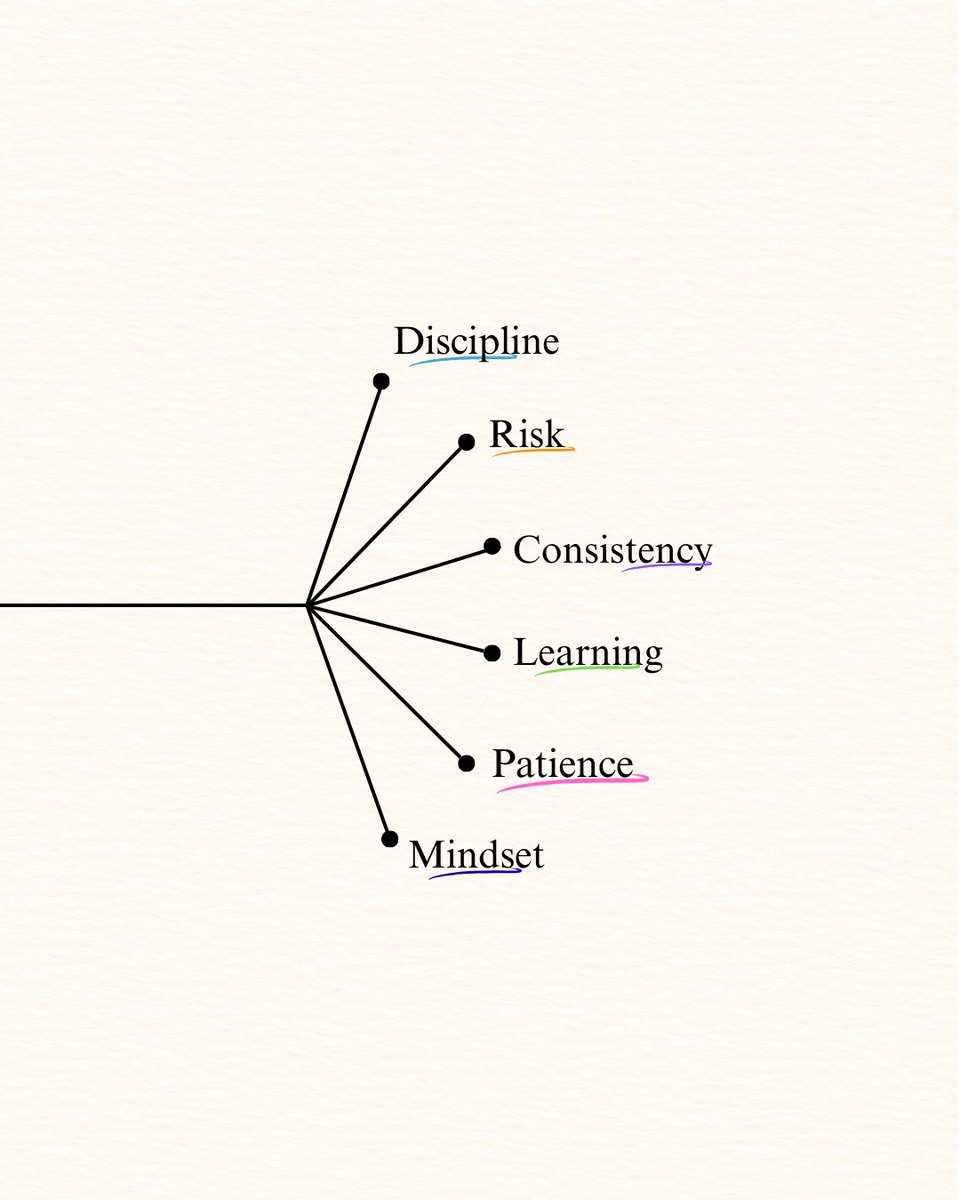

1) Trading is a skill, not a gamble

1) Trading is a skill, not a gamble Trading success isn’t about the best strategy, it’s about mastering yourself:

Trading success isn’t about the best strategy, it’s about mastering yourself:

1) What is Position Sizing

1) What is Position Sizing

1) Young Buffett thought he struck gold

1) Young Buffett thought he struck gold

1)The Core Idea

1)The Core Idea 1) Lets see last Nifty expiry on 8th May

1) Lets see last Nifty expiry on 8th May 1. “Anything can happen.”

1. “Anything can happen.”

1) I was able to enter and ride uptrend but unable to exit when trend changes.

1) I was able to enter and ride uptrend but unable to exit when trend changes.

2) While

2) While

1)Monitors :

1)Monitors :

1) “A smooth sea never made a skilled sailor.”

1) “A smooth sea never made a skilled sailor.”

Market breadth looks at the relative change of advancing to declining securities in a market.

Market breadth looks at the relative change of advancing to declining securities in a market. 1) The real breakthrough in my trading didn’t come from picking better stocks or reading charts more accurately.

1) The real breakthrough in my trading didn’t come from picking better stocks or reading charts more accurately.

1) Sensex opened at 83,611 and dropped 400 points in just 20 minutes!

1) Sensex opened at 83,611 and dropped 400 points in just 20 minutes!

2) 18th may 2009

2) 18th may 2009 2) I was having a great month & that made me more complacement as I made around 24% returns in last 4 months

2) I was having a great month & that made me more complacement as I made around 24% returns in last 4 months

2) Look at his stance on the crease. Look at the balance. Perfect. Simply elegant. Looks so pleasing to the eye.

2) Look at his stance on the crease. Look at the balance. Perfect. Simply elegant. Looks so pleasing to the eye.

2) Didnt' do anything all day and it's 11:58 PM?

2) Didnt' do anything all day and it's 11:58 PM?