,

33 tweets,

18 min read

Read on Twitter

#USS has just released a document on contingent contributions👇. I'm now reading it. Comments below when I've finished reading.

One crucial question is what metric would trigger a higher contribution. The two metrics that have been suggested are: 1/

(i) Increase in the technical provisions (TP) deficit above a certain level. This is the deficit with which we're familiar.

(ii) Increase in short-term reliance (aka 'self-sufficiency' deficit) above a certain level. 2/

(ii) Increase in short-term reliance (aka 'self-sufficiency' deficit) above a certain level. 2/

I argued in this blog 👇 that the most defensible trigger is a rise in TP deficit, where this deficit is measured by the fundamental building blocks (FBB) model #USS uses to form best estimates of returns on assets at each triennial valuation. 3/

medium.com/@mikeotsuka/th…

medium.com/@mikeotsuka/th…

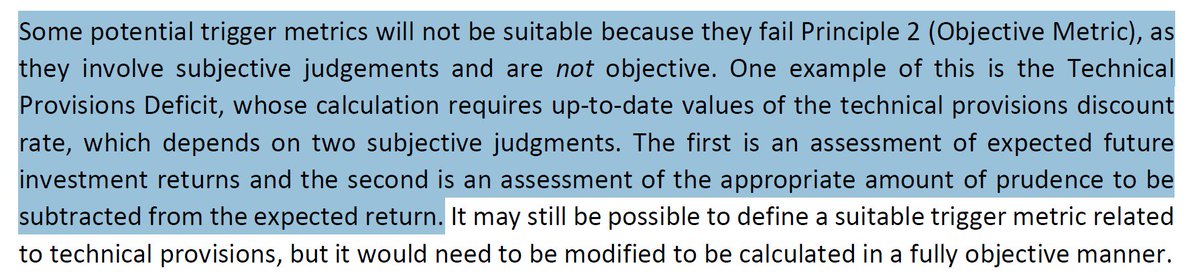

In this blue highlighted passage (p. 10) 👇, #USS rules out, as too subjective, a TP deficit trigger, where the deficit is measured via the FBB model. 4/

#USS's currently monitors the deficit between valuations on a gilts-plus basis. In this blog👇, I note the incoherence of this monitoring basis with their FBB model. I also note the volatility of a gilts-plus deficit. 6/

medium.com/@mikeotsuka/al…

medium.com/@mikeotsuka/al…

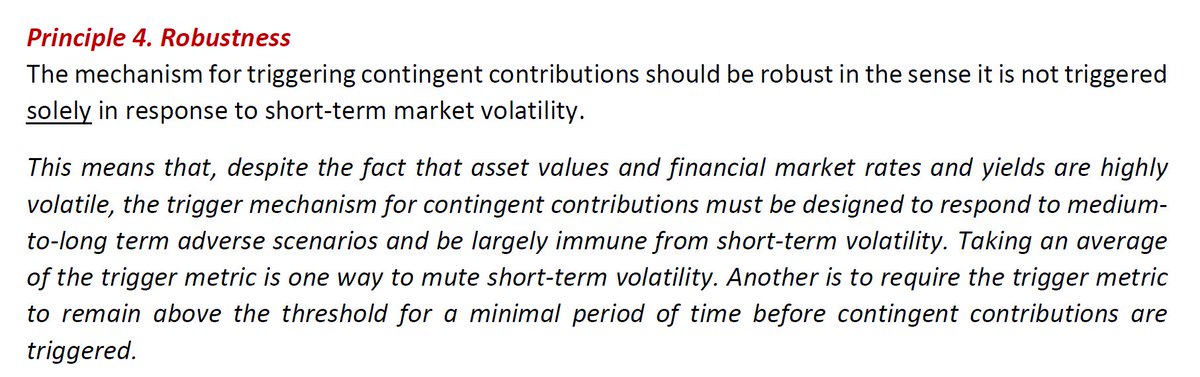

Sensibly, #USS affirms a principle of robustness👇, according to which volatility counts against a trigger. That would tell against a gilts-plus TP monitoring deficit as the trigger. 7/

The principle of robustness would also tell strongly against short-term reliance (aka the self-sufficiency deficit) as the trigger. See Sec II of this post 👇for a discussion of the volatility of a reliance trigger. 8/

medium.com/@mikeotsuka/wh…

medium.com/@mikeotsuka/wh…

A potential solution to the problem of lack of robustness (too much volatility) of either a reliance trigger or a gilts-plus TP trigger would be the adoption of a CPI-based TP trigger. 9/

The January consultation document on the 2018 valuation says: "The Trustee considers that measuring discount rates relative to CPI is the most appropriate approach, as the scheme’s liabilities for the main part are explicitly linked to CPI." (p. 13) 10/

Since a rise in CPI increases, rather than decreasing, the liabilities, the CPI assumption would not figure in a CPI-plus discount rate, since that would wrongly imply that an increase in CPI decreases the liabilities. 11/

Rather, a rise in the assumed level of CPI would correspond to a deterioration in the TP funding level, which might trigger a contribution increase. 12/

The assumed level of CPI would be "objectively" derived from market prices in the manner of USS's current CPI assumption, which is the spread between the nominal & the index-linked gilt yield, minus a fixed inflation risk premium & CPI-RPI wedge. 13/

Hence a CPI trigger would not involve the "subjective" approach of #USS's FBB approach to estimating returns on assets. It would be thoroughly grounded in "objective" market gilt yields, plus other parameters that would remain fixed. 14/

The market-derived CPI assumption is less volatile than the gilt yield. Hence it would better meet the criterion of robustness for a contribution trigger. 15/

A CPI trigger has the following further advantage over a gilts trigger: 16/

Changes in CPI correspond to changes in the value of the liabilities to a greater degree than do changes in the gilt-yield, given how little (only 12%) of the implemented USS portfolio is actually invested in IL gilts. 17/

A CPI-based TP trigger also avoids the huge problems that beset a reliance trigger, not least of which is that #USS's case for a reliance trigger collapses in the light of their "large and demonstrable mistake" over Test 1. See 👇. 18/

medium.com/@mikeotsuka/wh…

medium.com/@mikeotsuka/wh…

Short-term reliance (aka the 'self-sufficiency' deficit) is also an ill-motivated trigger metric for the following further reasons👇. 19/

medium.com/@mikeotsuka/wh…

medium.com/@mikeotsuka/wh…

I am hopeful that the document #USS has just released can provide the grounds for @USSEmployers to agree with #USS on a sensible CPI-based TP trigger of higher contributions, as best conforming to #USS's stated principles. 20/20

Especially given the low 12% investment of the currently implemented portfolio in gilts, any gilts-based trigger -- whether based on increase in 'reliance' or the gilts-plus TP deficit -- would appear to violate #USS's principle of alignment as well as robustness. 1/

A trigger tied to a gilts-plus discount rate (whether TP or self-sufficiency) magnifies a noisy indicator whose relevance to the financial soundness of an ongoing scheme such as #USS has not been demonstrated. 2/

A more accurate monitoring basis for TP funding between valuations would be one that hold the latest (2018) FBB projection of the long term returns on investments as reflected in the nominal discount rate fixed for the next 3 years, but... 3/

...adjusts the value of the liabilities in order to reflect a rise or fall in market-derived CPI & changes in the CMI mortality tables. The liabilities adjusted by just CPI & mortality would then be measured against assets at current market value. 4/

If, by this measure, TP funding goes below a certain level, expressed as a % of full funding, for a given period of time, that would trigger an increase in contributions. 5/

If triggers must also be sensitive to changes in the gilt yield, it would be more appropriate to adjust the expected returns of only the 25% of the reference portfolio designated as IL gilts by changes in the gilt yield. 6/

If the other components of the reference portfolio (e.g., the 62.5% in equities and the 10% in credit & emerging market bonds) also require adjustment, these can be based on designated market-based measure more appropriate to these classes of assets than the gilt yield. 7/

.@FirstActuarial's method 👇of estimating returns on equity, property, & corporate bonds might be adopted & updated simply to reflect market-based changes in the dividend yield, the corporate bond yield, or CPI. 8/

ucu.org.uk/media/8410/Fir…

ucu.org.uk/media/8410/Fir…

An algorithm could be entirely agreed in advance for how expected returns on these different asset classes in the reference portfolio would be adjusted by changes in specified market-based changes. 9/

Adjusting the expected returns of the discount rate in this manner would qualify as entirely "objective", but it would provide a far more accurate account of changes in the TP discount rate than a crude gilts-plus approach. 10/10