1) "Federal Reserve developed the #MainStreetLending Program to help credit flow to small and medium-sized businesses that were in sound financial condition before the pandemic."

2) after initial announcement of #MainStreetLending Program, Fed Reserve expanded it to: Create a 3rd loan option, w/increased risk sharing by lenders for borrowers with greater leverage &

Lowered the minimum loan size for certain loans to $500,000

federalreserve.gov/newsevents/pre…

Lowered the minimum loan size for certain loans to $500,000

federalreserve.gov/newsevents/pre…

3) this resulted in 3 loan (🍕) options: plain, pepperoni & mushroom: "termed new, priority, & expanded" 4 year loans:

New: $500K Minimum Loan Size

Priority: Ditto

Expanded: $10M Minimum Loan Size & up to a TON!

New: $500K Minimum Loan Size

Priority: Ditto

Expanded: $10M Minimum Loan Size & up to a TON!

4) the Max under these loans is complex: the lesser of a hard $# "or an amount that, when added to outstanding & undrawn available debt, doesn't exceed __x adjusted 2019 EBITDA"

New: Max = lesser of $25M or 4x 2019 EBITDA

Priority: Max = lesser of $25M or 6x 2019 EBITDA

&

New: Max = lesser of $25M or 4x 2019 EBITDA

Priority: Max = lesser of $25M or 6x 2019 EBITDA

&

5) Expanded: Max = "lesser of $200M, 35% of existing outstanding & undrawn available debt, or an amount that, when added to outstanding & undrawn available debt, does not exceed 6.0x adjusted 2019 EBITDA"

for all 3, payments deferred for yr 1

for all 3, payments deferred for yr 1

6) the govt❤️acronyms. "Main Street Expanded

Loan Facility=MSELF"

On May 15, Federal Reserve: "The Board continues to expect that the MSELF will not result in losses to the Federal Reserve." I too will not blame MSELF!

federalreserve.gov/publications/f…

Loan Facility=MSELF"

On May 15, Federal Reserve: "The Board continues to expect that the MSELF will not result in losses to the Federal Reserve." I too will not blame MSELF!

federalreserve.gov/publications/f…

7) Unlike PPP, lenders retain some risk: Federal Reserve Bank of Boston will commit to lend to a single common special purpose vehicle (SPV) on a recourse basis

The SPV will buy 95% participations in Eligible Loans from

Eligible Lenders. Those Lenders will keep 5% of each Loan.

The SPV will buy 95% participations in Eligible Loans from

Eligible Lenders. Those Lenders will keep 5% of each Loan.

8) Unlike PPP, #MainStreetLendingProgram: "The availability of additional credit is intended to help companies that were in sound financial condition prior to the onset of the COVID-19 pandemic maintain their operations and payroll until conditions normalize." #MSLP (from FAQs)

9) Also unlike #PPPLoans, #MainStreetLoans "are full-recourse loans and are not forgivable." FAQ 3

federalreserve.gov/monetarypolicy…

federalreserve.gov/monetarypolicy…

14) that doesn't stop an Eligible Lender from extending maturity of an existing loan to get it to 18 months for purposes of #MSELF eligibility (also FAQ D1) - so you can extend & upsize

15) #ELIGIBILITY requirements for #MSLP are in FAQ E1 & include: 15k or $5B:

The Business must EITHER have (a) 15,000 employees or fewer, or (b) 2019 annual revenues of $5B or less.

YOU MUST "aggregate with the employees & revenues of its AFFILIATED entities"

The Business must EITHER have (a) 15,000 employees or fewer, or (b) 2019 annual revenues of $5B or less.

YOU MUST "aggregate with the employees & revenues of its AFFILIATED entities"

16) #MSLP is truly for🇺🇸business: "created or organized in the US or under the laws of the US with significant operations in & a majority of their employees based in the US." FAQ E.1(4)

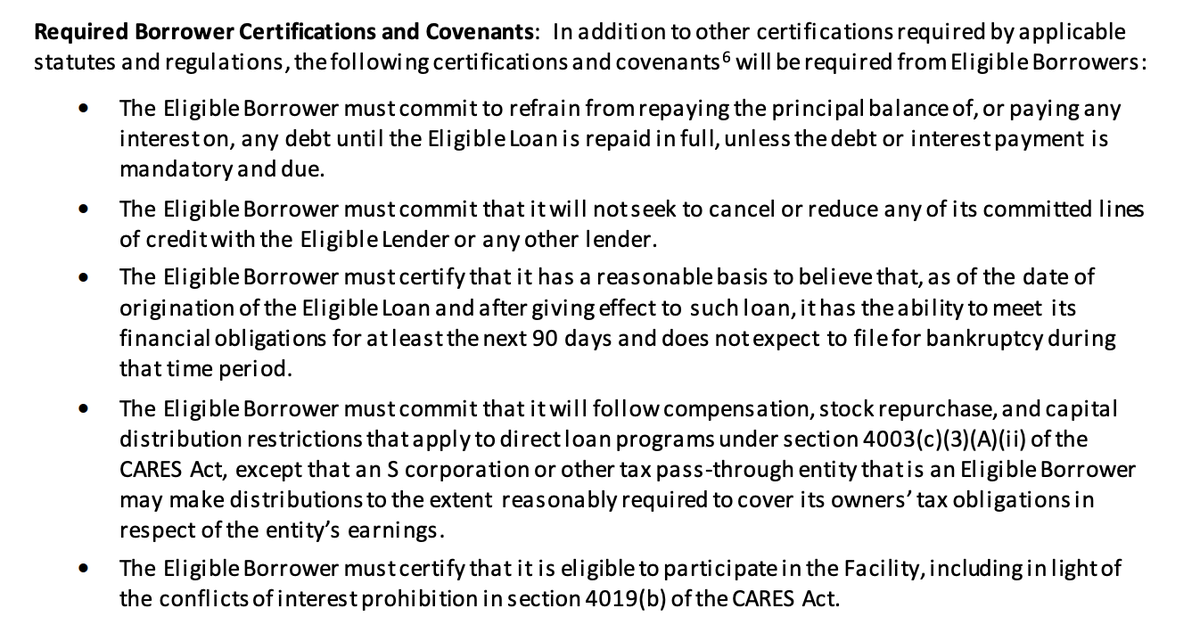

18) There are required borrower certifications: I've attached the #MSNLF certifications, available on page 3 here: federalreserve.gov/newsevents/pre…

19) #MSNLF also obligates borrowers to "make commercially reasonable efforts to maintain its payroll & retain its employees during the time the Eligible Loan is

outstanding." Remember - these are 4 year loans!

outstanding." Remember - these are 4 year loans!

20) as in PPP, Treasury &, in this case, Federal Reserve are expressly entitling lenders to "rely on an Eligible Borrower’s

certifications & covenants, as well as any subsequent self-reporting by the Eligible Borrower." So we will also have some compliance issues...

certifications & covenants, as well as any subsequent self-reporting by the Eligible Borrower." So we will also have some compliance issues...

21) Just in case it wasn't clear - PPP & Main Street are NOT mutually exclusive: p10 of the FAQ "For the avoidance of doubt, a Business that has received PPP loans, or that has affiliates that have received PPP loans, is permitted to borrow under Main Street,"

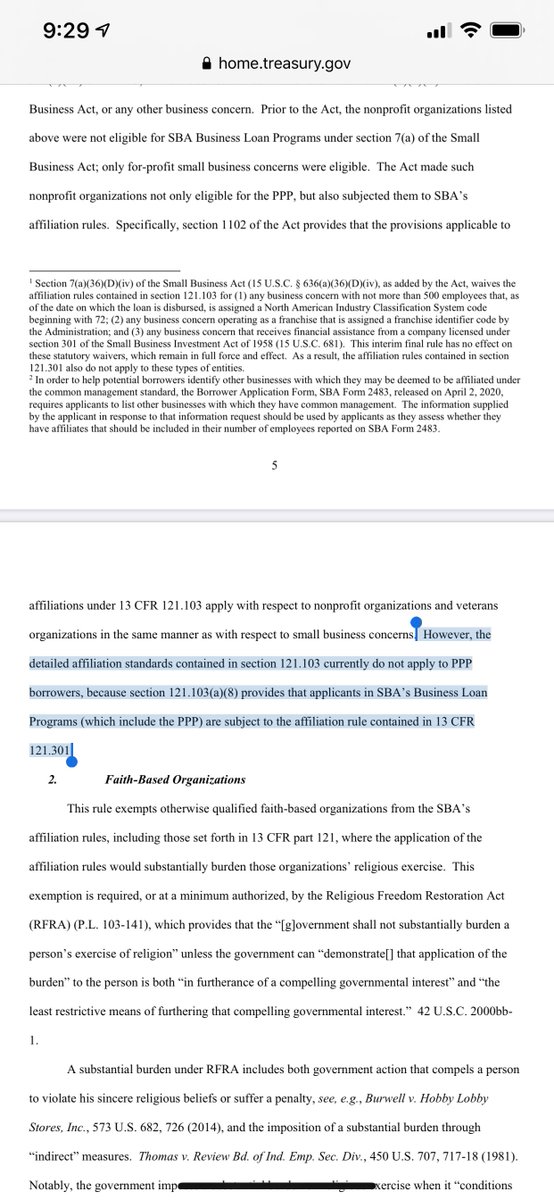

22) Affiliation issues will be even more complex under Main Street because these are larger organizations and the revenue cut off / employee headcount limits BOTH require aggregating with ALL AFFILIATES. We're using 301(f), just as with PPP Loans:

federalreserve.gov/monetarypolicy…

federalreserve.gov/monetarypolicy…

23) FAQ E.5) "Business’s employees & 2019 revenues are calculated by aggregating the employees & 2019 revenues of the Business itself with those of the Business’s affiliated entities in accordance with the affiliation test set forth in 13 CFR 121.301(f) (1/1/2019 ed.)

24) FAQ E6&7 recognize that "EBITDA is the key

underwriting metric required for #MSNLF #MSPLF & #MSELF" so #nonprofits are out for now & they're figuring out what to do about "asset-based borrowers"

underwriting metric required for #MSNLF #MSPLF & #MSELF" so #nonprofits are out for now & they're figuring out what to do about "asset-based borrowers"

25) FAQ G explains that for calculating EBITDA, there's an emphasis on past practices by that lender, esp for that borrower.

Calculating outstanding debt has some twists & turns, & is also discussed in FAQ G

Calculating outstanding debt has some twists & turns, & is also discussed in FAQ G

26)"'Existing outstanding&undrawn available debt' includes all amounts borrowed under any loan facility, including unsecured or secured loans from any bank, non-bank financial institution,or private lender, as well as any publicly issued bonds or private placement facilities" BUT

27) there are exclusions too, so CFOs will sharpen pencils. Also, the calculation date matters:

"Existing outstanding & undrawn available debt should be calculated as of the date of the loan application."

"Existing outstanding & undrawn available debt should be calculated as of the date of the loan application."

28) G5 speaks to #amortization & could be clearer. There's definitely no payment during yr 1 across ANY of the 3 loans & then:

#MSNLF=1/3 each @ end of yrs 2,3&4

#MSPLF & #MSELF=15% of principal due @ end of each of years 2&3,& 70%🎈balloon payment at maturity (end of year 4)

#MSNLF=1/3 each @ end of yrs 2,3&4

#MSPLF & #MSELF=15% of principal due @ end of each of years 2&3,& 70%🎈balloon payment at maturity (end of year 4)

29)SECURITY

All 3 loans may be secured or unsecured, but

"An MSELF Upsized Tranche MUST be secured if the underlying loan is secured." If secured, any

collateral securing the underlying loan "must

secure the MSELF Upsized Tranche on a pro rata basis"

open.spotify.com/track/1j1HxIXx…

All 3 loans may be secured or unsecured, but

"An MSELF Upsized Tranche MUST be secured if the underlying loan is secured." If secured, any

collateral securing the underlying loan "must

secure the MSELF Upsized Tranche on a pro rata basis"

open.spotify.com/track/1j1HxIXx…

31) "Borrower should undertake good-faith commercially reasonable efforts to maintain payroll & retain employees during the term of the loans?

"in light of its capacities, the economic environment, its available resources, and the business need for labor."

FAQ G8

"in light of its capacities, the economic environment, its available resources, and the business need for labor."

FAQ G8

32) the govt knows some of you have already done layoffs, & they understand:

"Borrowers that've already laid-off/furloughed workers as a result of disruptions from COVID-19 are eligible to apply for #MainStreetloans"

"Borrowers that've already laid-off/furloughed workers as a result of disruptions from COVID-19 are eligible to apply for #MainStreetloans"

34) some restrictions on comp & stock buybacks & paying down debt. For instance: borrower must "commit to refrain from repaying principal or interest on any debt until #MSNLF or #MSELF #UpsizedTranche is repaid in full, unless the debt or interest payment is

mandatory&due"

mandatory&due"

36) that shouldn't stop you from drawing/paying down line of credit in ordinary course or getting/using equipment/inventory financing "provided that such debt is secured by newly acquired property..." & is junior or pari passu to the MS loans

& you can refi maturing debt

& you can refi maturing debt

37) & when @federalreserve says “Upsize” the Tranche, am I the only 1 who thinks of rapper’s delight by #SugarhillGang “up jump the boogie to the rhythm of the...”? open.spotify.com/track/0FWhGmPV…