Last week Arsenal announced that they will redeem their outstanding bonds, which had been part of the debt taken on to fund the construction of the Emirates Stadium. This will be financed by owner Stan Kroenke’s company KSE. The following thread explains what this means #AFC

The first thing to appreciate is what this transaction does not mean. It will not make #AFC debt-free, nor does it mean that Kroenke is finally investing into the club. Instead, it is simply a restructuring of the club’s current debt by changing the lender.

This is similar to where you take out a mortgage at a certain interest rate with one bank, but a few years later realise that interest rates on new mortgages are much lower, so decide to remortgage with another bank – even though you have to pay a penalty for early repayment.

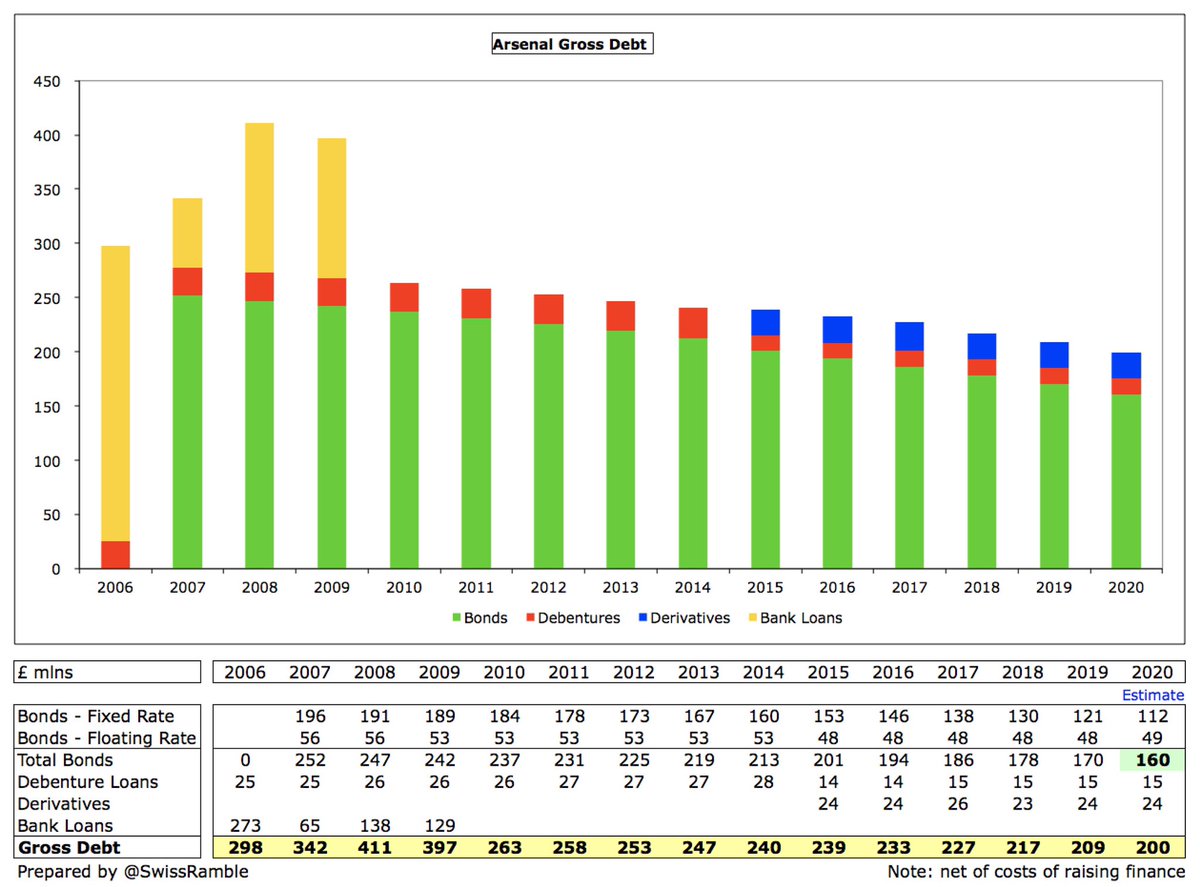

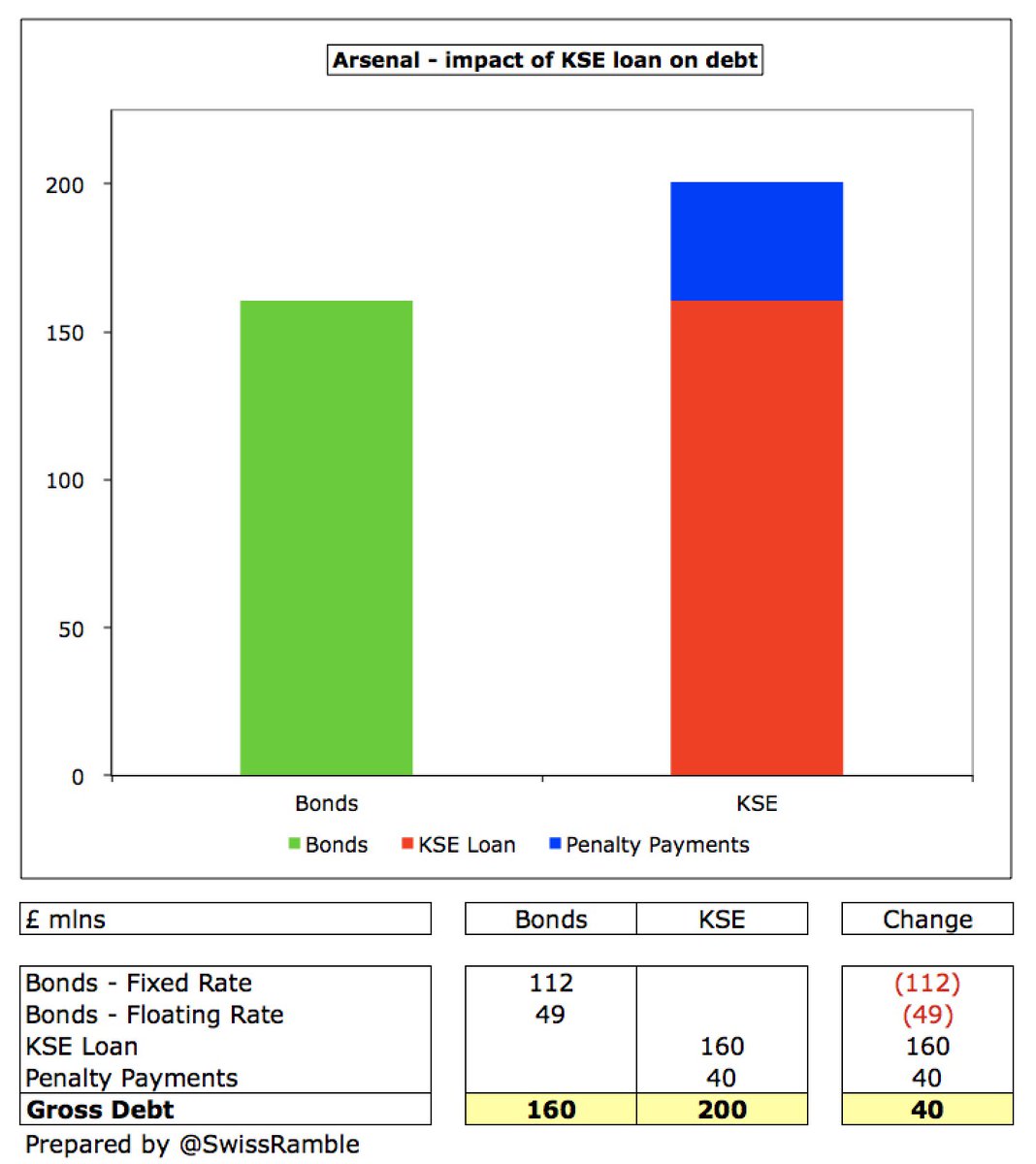

#AFC issued £260m of bonds in 2006 (£210m fixed rate and £50m floating rate, to be repaid in 2029 and 2031 respectively) and have been making annual repayments every year since. Remaining balance was £170m at 31st May 2019, so I estimate that the current balance is around £160m.

The £160m still owing on the bonds is the lion’s share of #AFC outstanding debt, but the club also has another £40m of debt (£15m debentures and £24m derivatives). Therefore, the total debt as at 31st May 2019 was £209m, down to around £200m now.

Although this is effectively a remortgage, it is likely that #AFC debt will increase, as the KSE loan will probably also include penalties paid for early bonds repayment (net present value of future payments, discounted at current interest rate). The AST estimates this as £40m.

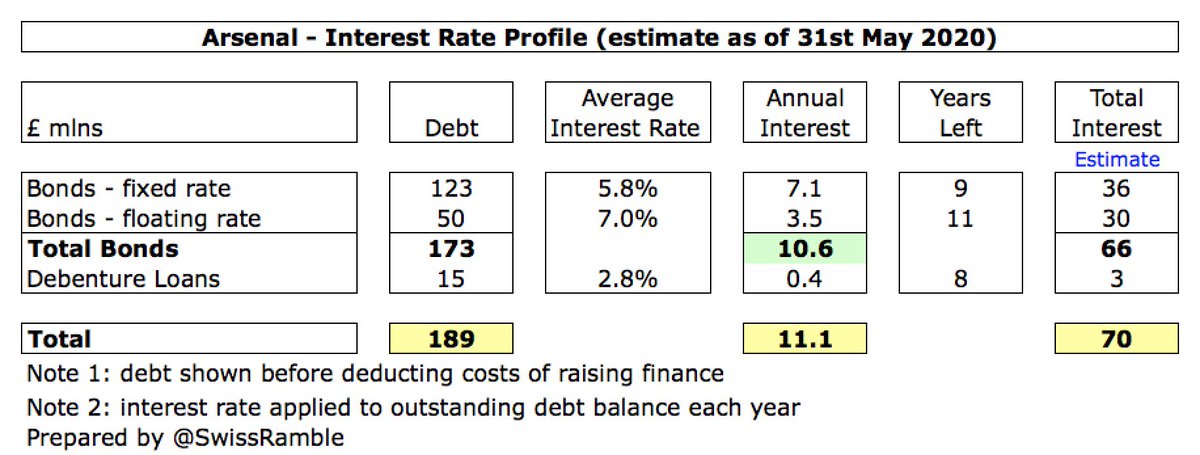

The interest rates on #AFC bonds are very high, compared to today’s record low rates. Including guarantee fees to the bond provider, the interest rate for the fixed rate bonds averages 5.8%, while the floating rate bond is 7%. This works out to an £11m annual interest payment.

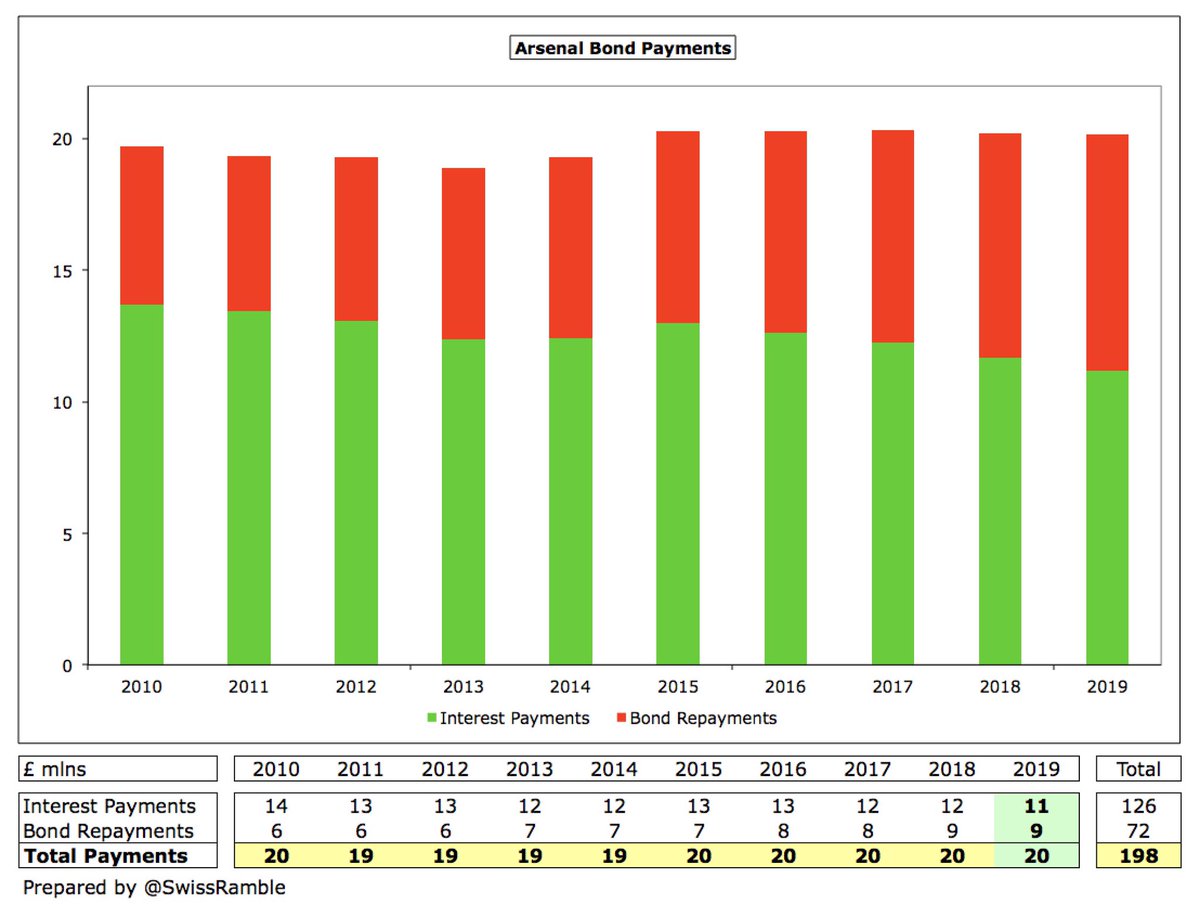

In addition to the £11m interest payment, #AFC have also been making annual repayments to reduce the loan of £9m, so the total cash outlay to service the bonds has been a hefty £20m a year.

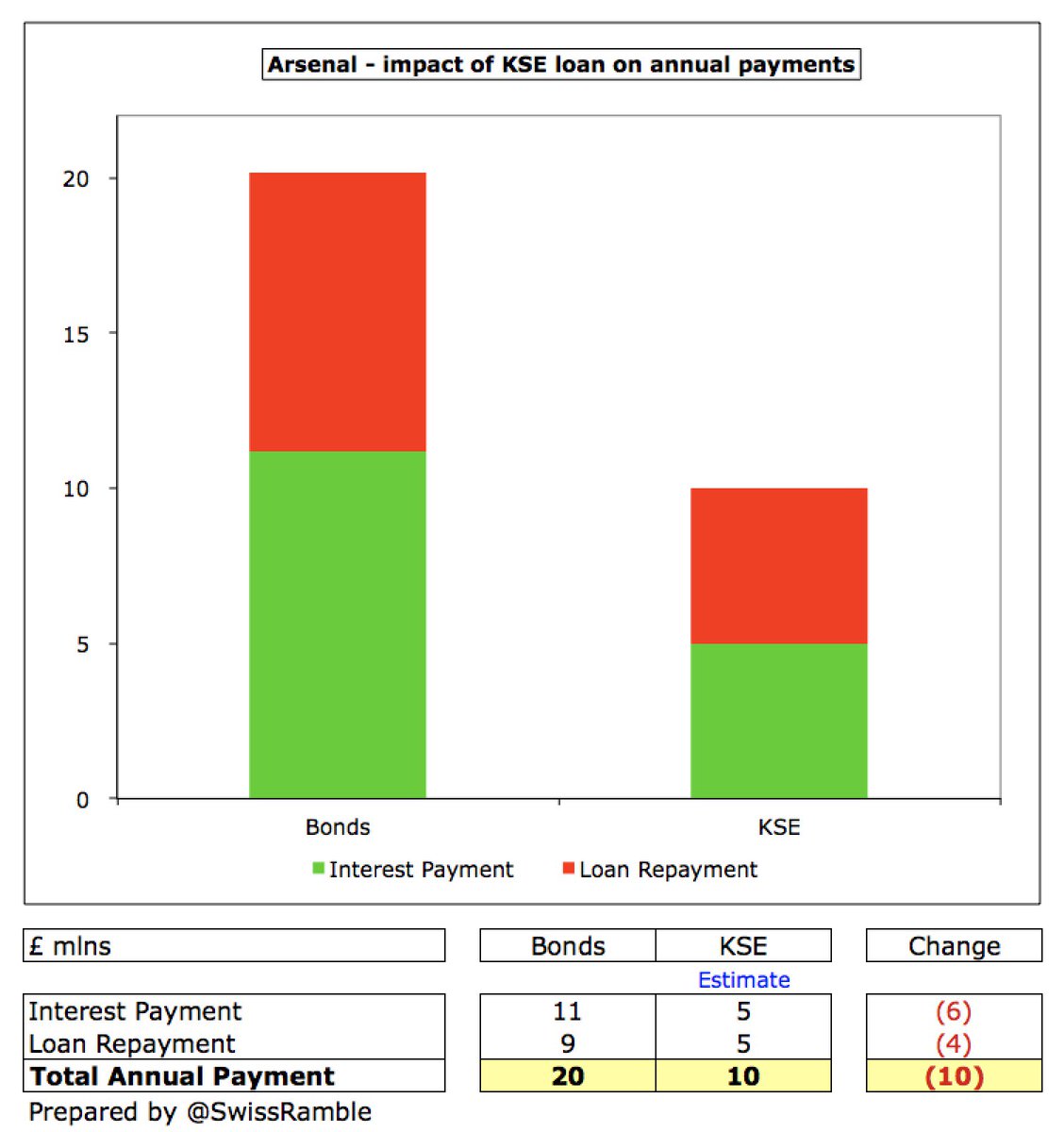

Ideally, the KSE loan will be interest-free, so annual saving on interest would be £11m, but my guess is that it will probably be market rate, so the saving is more likely to be around £6m. Potentially, Kroenke could charge a higher interest rate, but that would be surprising.

KSE might also extend the repayment schedule beyond 2029 and 2031 (as Kroenke did with his LA Rams loan), which would mean smaller annual repayments, thus reducing the current £9m cost. There could conceivably also be a payment holiday over the next couple of challenging years.

Based on these assumptions, #AFC annual cost of servicing the loan would be halved from £20m (interest £11m + repayment £9m) to £10m (interest £5m + repayment £5m).

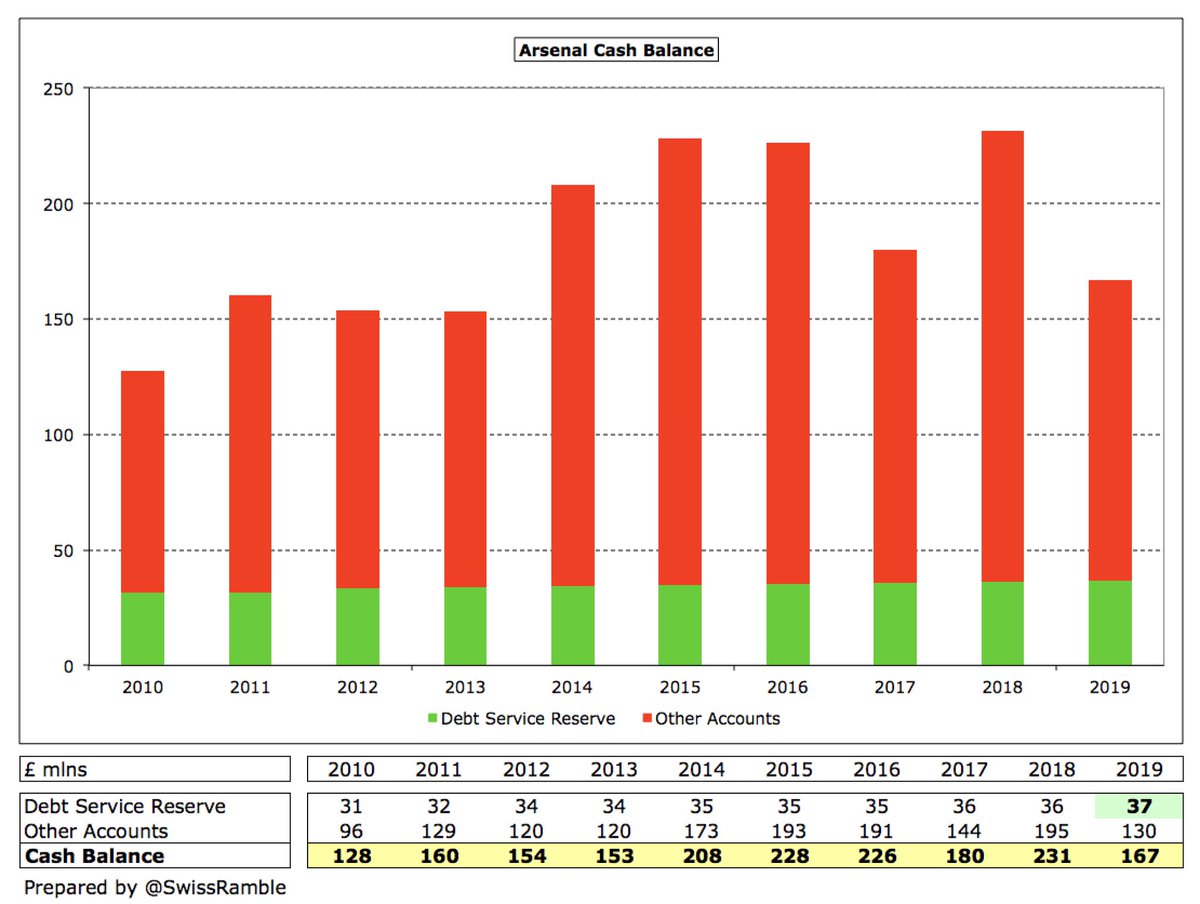

One of the requirements of the bonds was that #AFC had to hold a debt service reserve as security for future payments, accounting for £37m of the £167m cash balance in 2019. This will no longer be required, so can be freed up as a once-off boost to available cash.

KSE previously took out a £500m loan from Deutsche Bank to finance the buy-out of Alisher Usmanov, so this means their overall debt is up to £700m. To date, #AFC has not borne the cost the £500m debt, so it is hoped that they still only have to service the new debt in future.

Interestingly, Kroenke’s Deutsche Bank loan was short-term, maturing in August 2020, so it is possible that the new loan to #AFC will be linked to the refinancing of his existing loan.

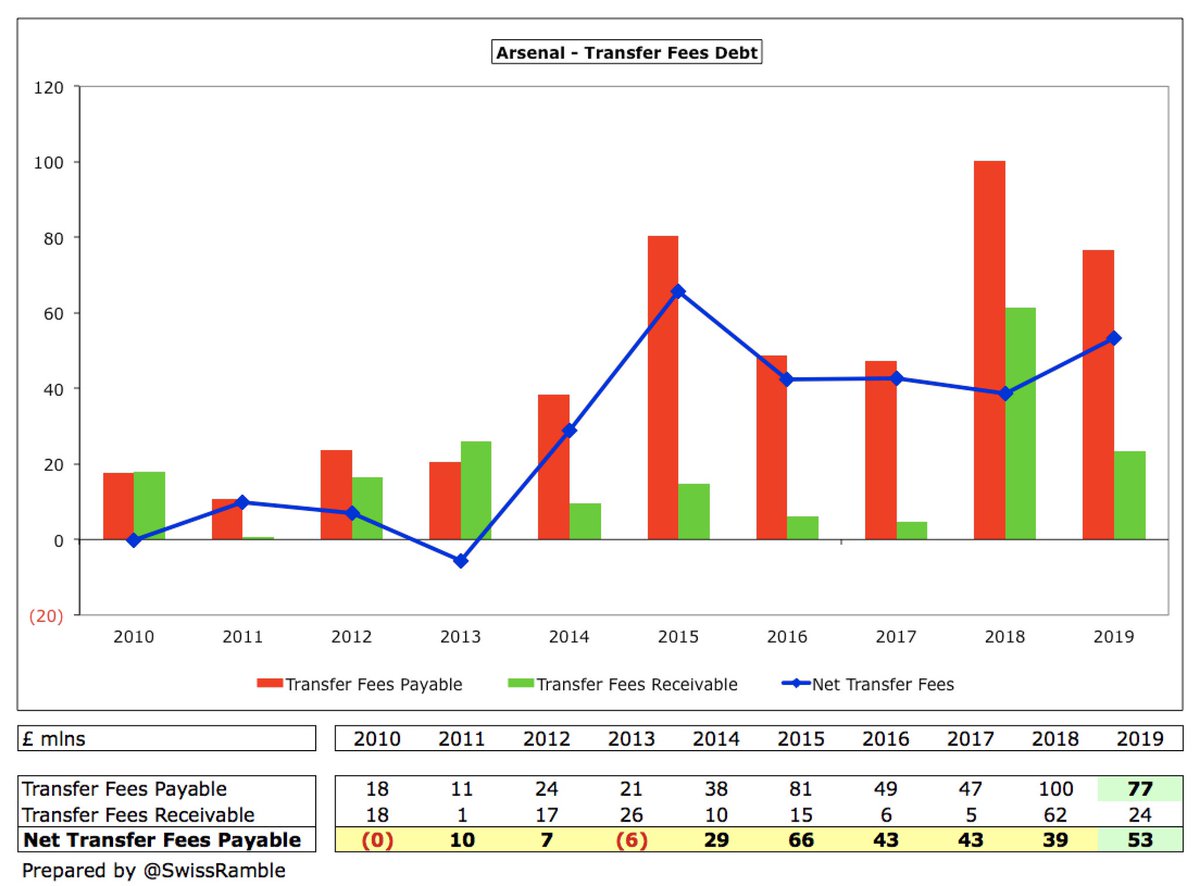

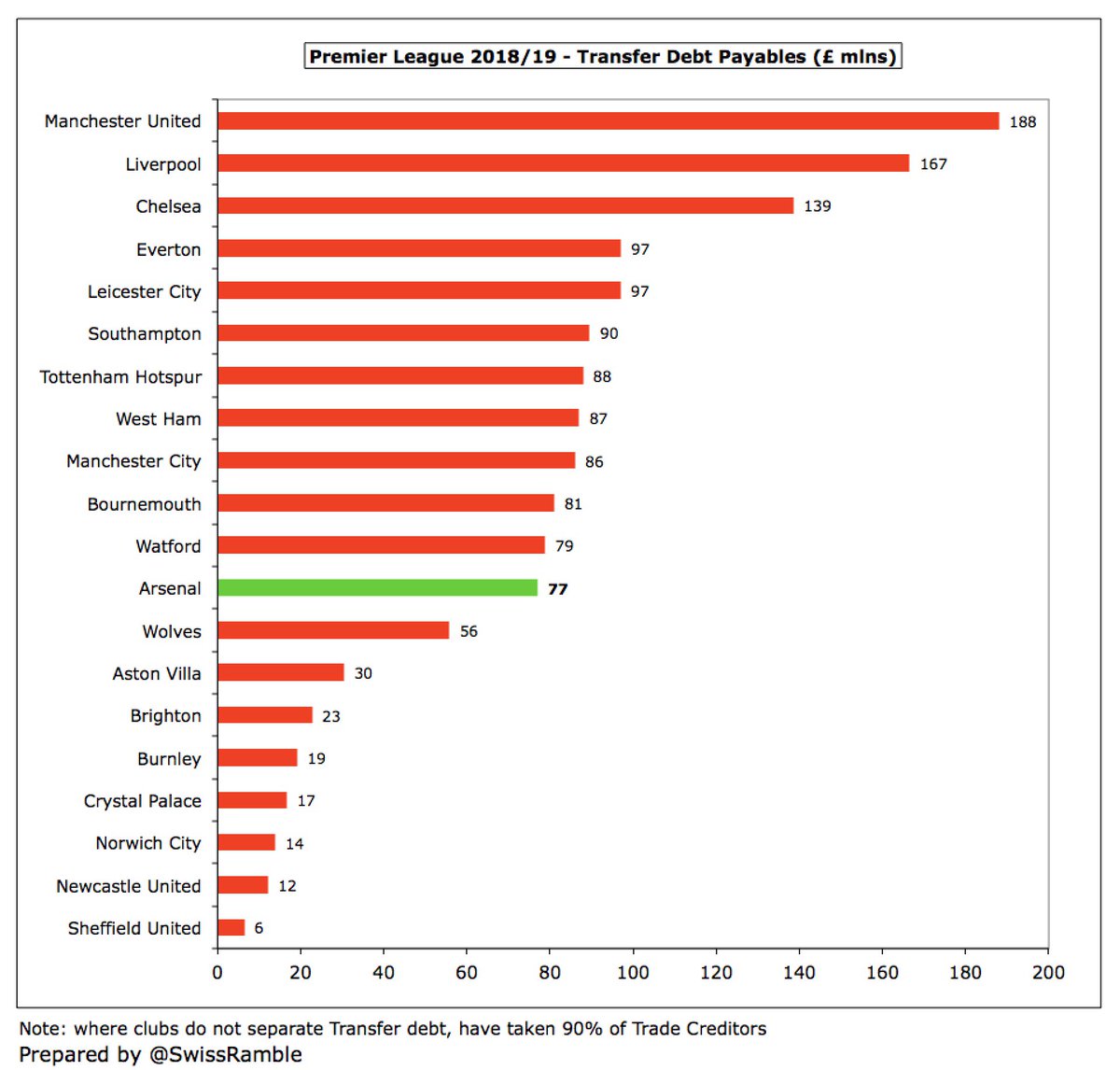

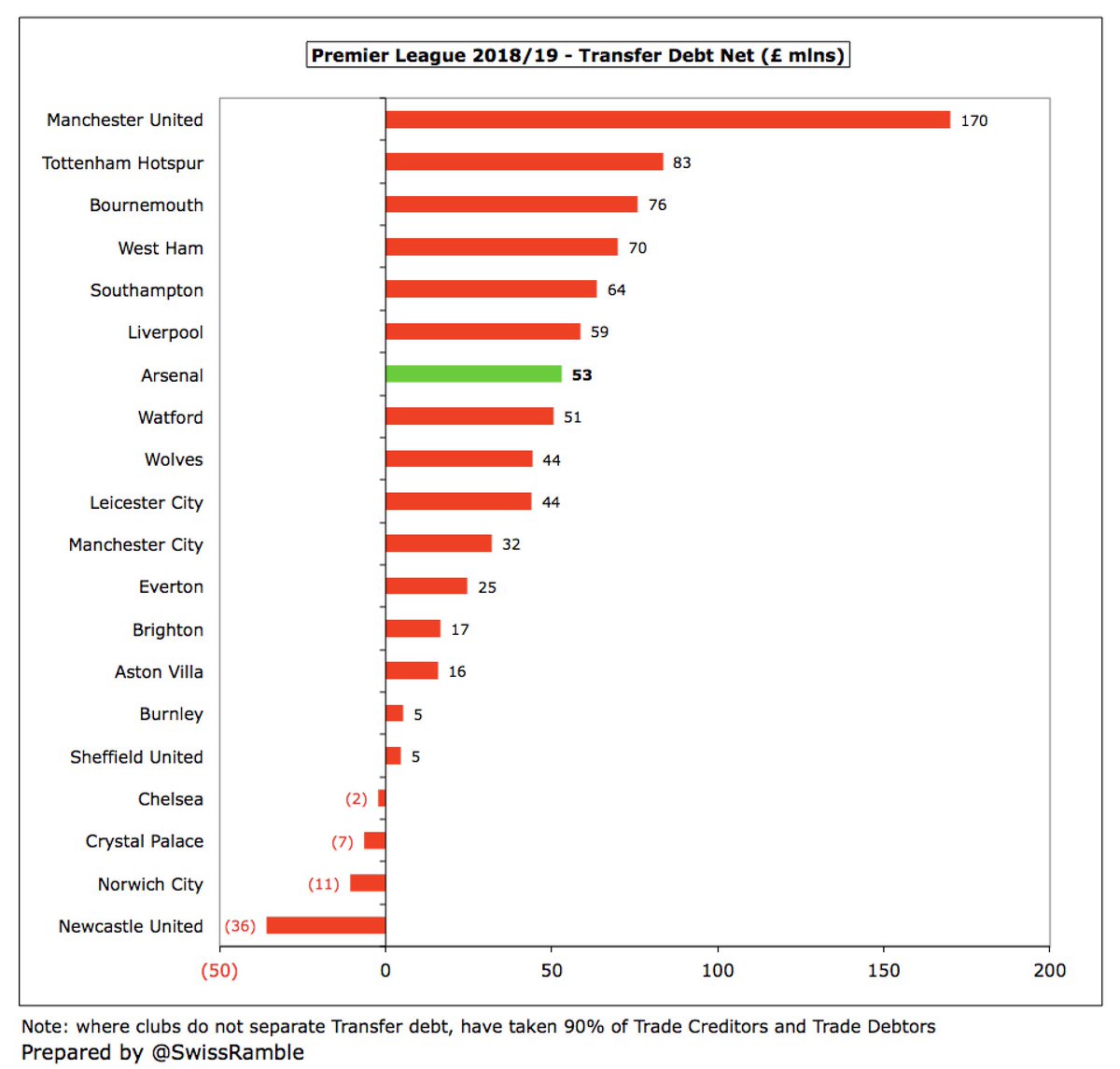

In addition to financial debt, #AFC also have transfer debt for outstanding stage payments on previous signings. This was £77m gross as at May 2019, £53m net of amounts other clubs owe Arsenal, but must be higher now after last summer’s £140m spend (Pépé, Saliba, Tierney, etc).

Although some #AFC fans might hope that the KSE loan will drive player purchases, it unlikely to produce the proverbial “war chest”. Instead, it is far more likely to be used to shore up finances in this challenging period, as COVID-19 has had a dramatic impact on revenue.

KSE loan might help a little, but #AFC transfer budget is more dependent on European qualification (Champions League or Europa League). As Mikel Arteta said, “I am planning for two or three different scenarios. Depending on that, we will be able to do more, less or nothing.”

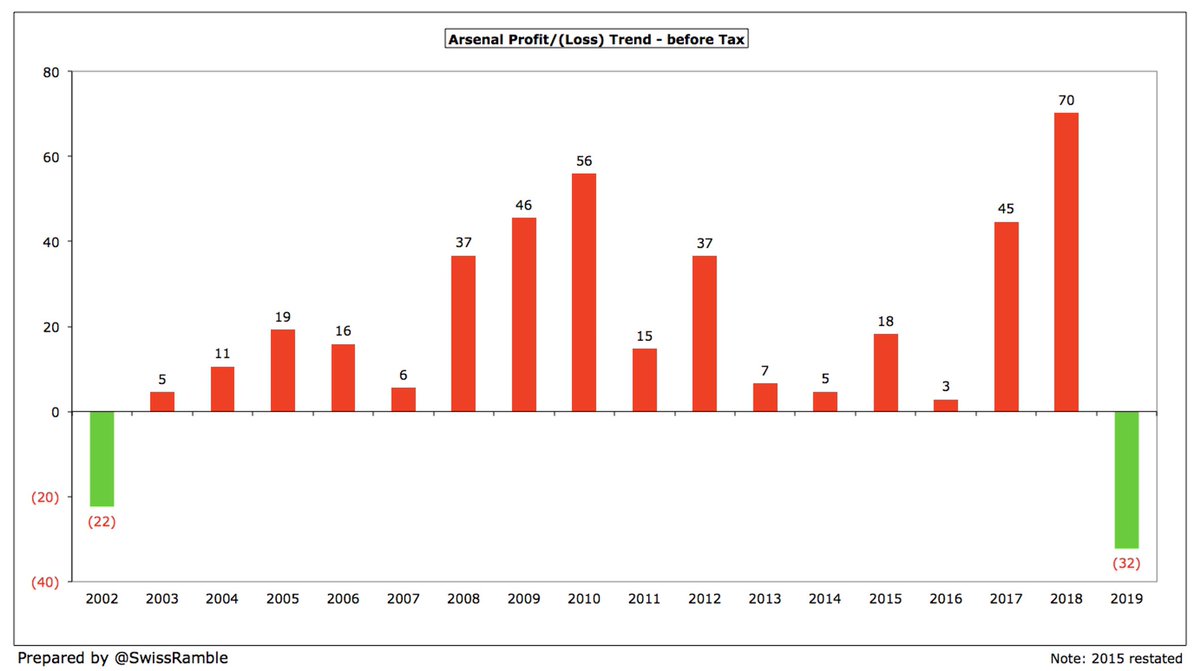

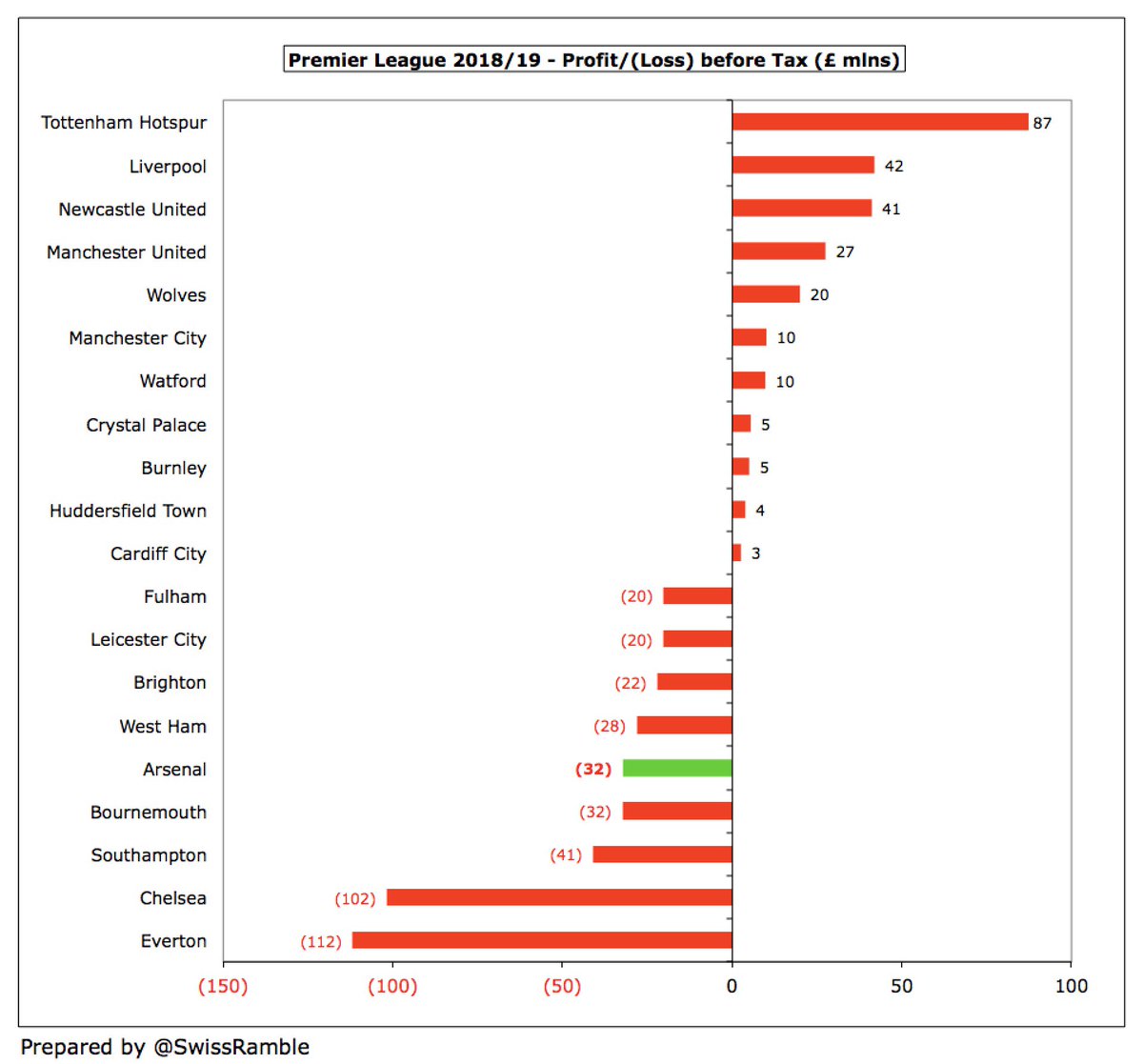

Even before the pandemic, in 2019 #AFC posted their first loss since 2002. In fact, their £32m pre-tax loss was one of the worst financial performances in the Premier League with only four clubs reporting higher losses than the Gunners.

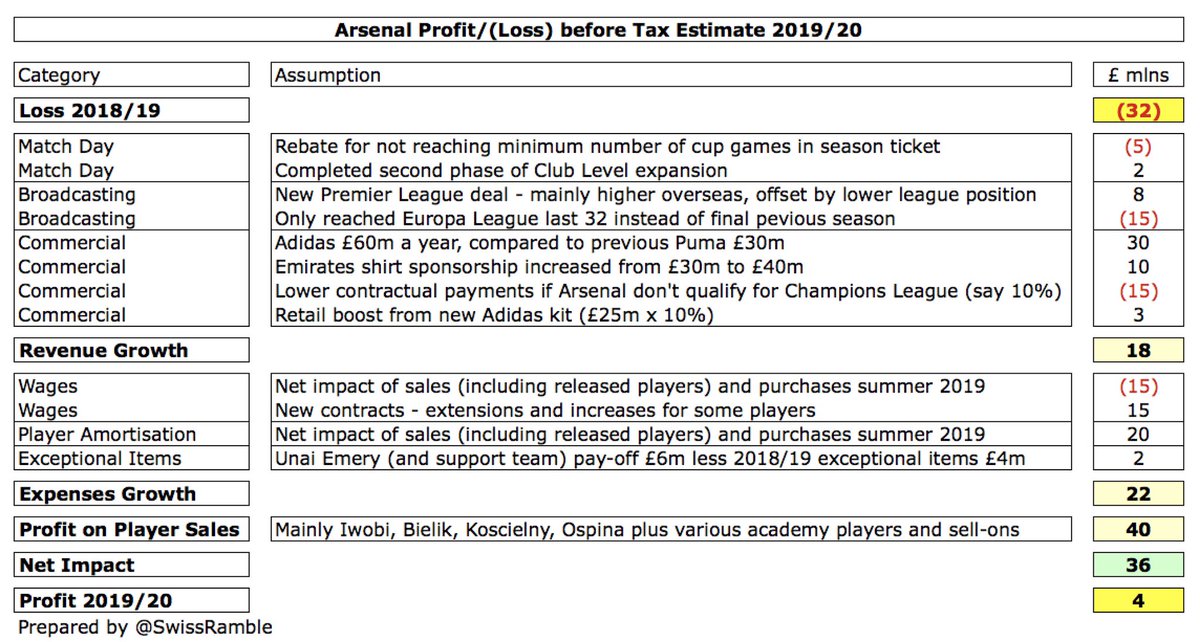

My estimate for 2019/20 pre-lockdown was a small £4m profit for #AFC. Revenue was set to increase, mainly due to new sponsorship deals, offset by the earlier Europa League exit. Higher player amortisation (wages assumed to be flat), but profit on player sales around £40m more.

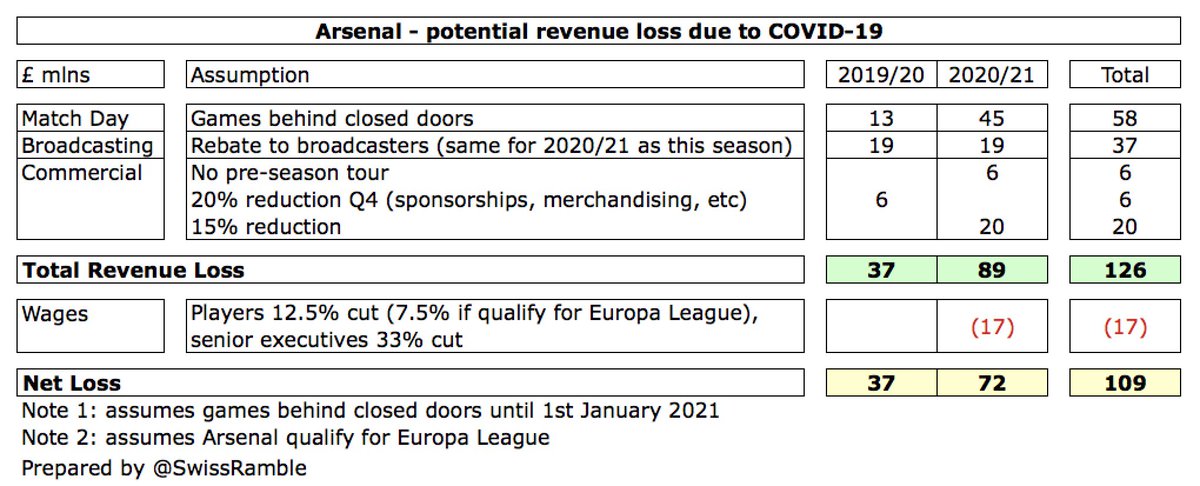

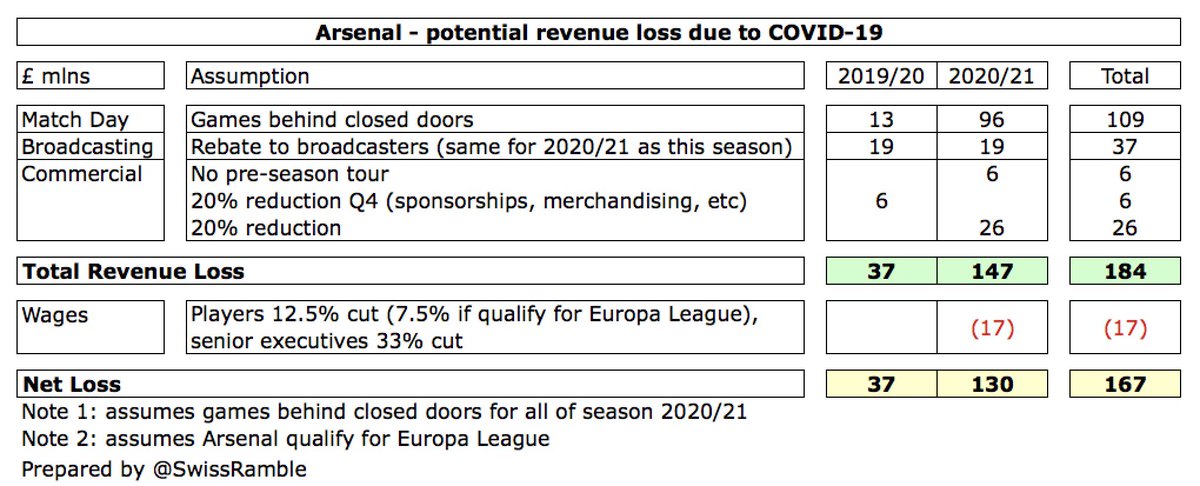

However, COVID-19 will lead to an estimated £37m reduction in #AFC 2019/20 revenue, made up of falls in match day £13m, TV £19m & commercial £6m. Similarly, in 2020/21 I have modeled revenue decrease of £89m (games behind closed doors until January) or £147m (BCD whole season)

Let’s walk though the assumptions behind those figures to see whether they are reasonable, as there are many factors to consider. To be very clear, this is not an exact science, but an “educated estimate”.

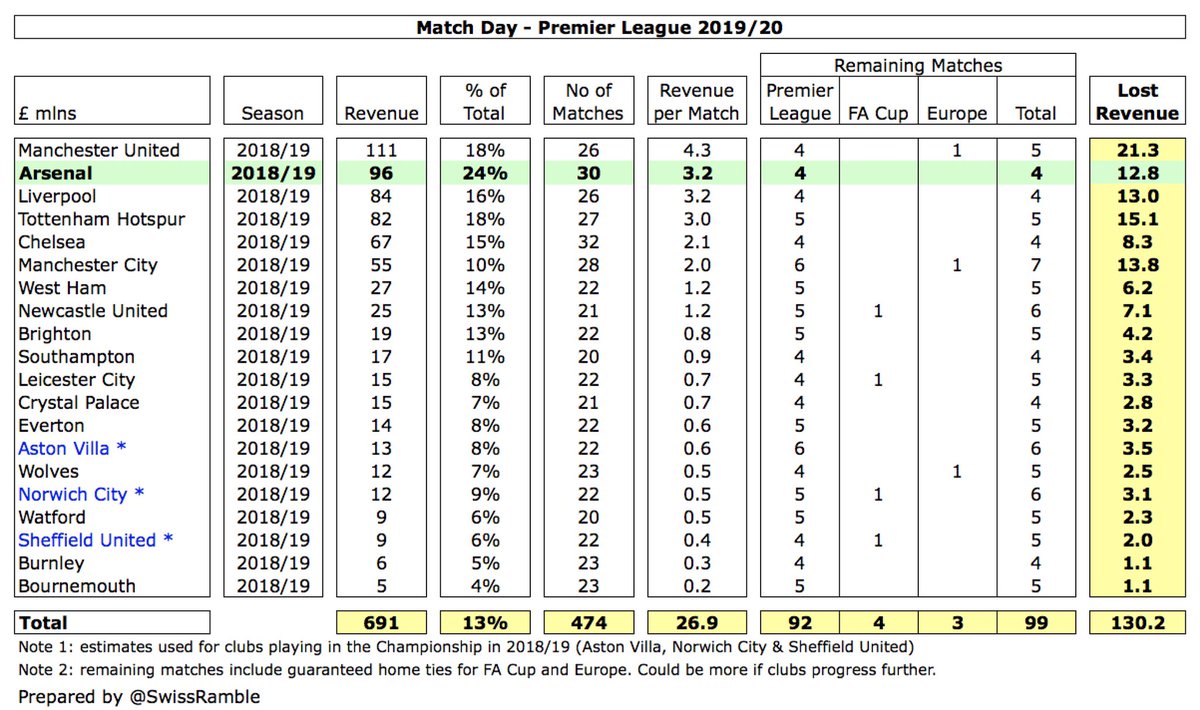

Based on £3.2m average revenue per game, #AFC will lose £13m match day income in 2019/20, as the 4 remaining Premier League home games after the restart are played behind closed doors. For 2020/21, if games are BCD for rest of 2020, loss would be £45m; up to £96m if whole season.

The lockdown likely means a fall in commercial income, due to lower exposure for sponsors and fewer retail sales. Assuming 20% cut for last 3 months would give £6m fall in 2019/20 revenue. If we go for 15% cut (on higher base) and no pre-season tour, 2020/21 revenue down £26m.

Against that, #AFC players agreed 12.5% wage cut for next year (down to 7.5% if they qualify for Europa League and zero if they secure Champions League football), while senior executives accepted a cut of around a third. Europa League would mean £17m cut in wages, no Europe £29m.

In other words, the savings from the wage cuts will be nowhere near enough to offset the steep reductions in #AFC revenue.

Putting that together, #AFC are facing a significant revenue loss of £126m over the next two seasons (2019/20 £37m plus 2020/21 £89m) – but this assumes that fans can attend games as normal from January.

If games were to be played behind closed doors for the whole of next season, #AFC 2-year revenue loss would be a massive £184m (2019/20 £37m plus 2020/21 £147m). Given that the maximum annual savings from the KSE loan are £20m, this shows the magnitude of the club’s challenge.

So this debt restructuring is much more about dealing with the issues caused by the pandemic and easing the club’s cash flow challenges. Normally at this time of the year, the cash balance is boosted by season ticket payments, but that is obviously not the case at present.

It’s doubtful whether Kroenke would have restructured #AFC debt without the pandemic, but in fairness it is more than just guaranteeing a higher loan, though not as attractive as injecting new equity/capital. He could also have sold a stake in the club, but it’s a buyer’s market.

Unfortunately, KSE has not yet published the loan details, so much of this analysis is inevitably speculative. We will only know for sure after #AFC publish 2020/21 accounts (normally February 2022), though they might include as a post balance sheet event in this year’s report.

To summarise, the KSE loan is probably a positive development for #AFC in that it will likely lead to lower annual payments (interest and debt) and free up the debt service reserve, but it is unlikely to fuel the level of transfer spend that some fans would like to see.