1/ Notes from @Jesse_Livermore episode at @InvestLikeBest

If you are yet to listen to this episode, here's a friendly suggestion: Do not put the audio speed more than 1x. The guest in this episode already talks at 2x speed.

Perhaps that's by design to fit in all his insights.

If you are yet to listen to this episode, here's a friendly suggestion: Do not put the audio speed more than 1x. The guest in this episode already talks at 2x speed.

Perhaps that's by design to fit in all his insights.

2/ A few weeks ago, @Jesse_Livermore wrote an intriguing paper on "upside-down markets".

Here he explains what exactly an upside-down market is.

Here he explains what exactly an upside-down market is.

3/ Fiscal response materially differs from monetary response. Fiscal response increases people's unencumbered spending power.

4/ Covid may give license to make fiscal policy a permanent theme in policy toolkit going forward regardless of who wins the election.

Just one scenario Jesse later explains as negative for stocks: Biden Presidency + GOP Senate. All other combinations are likely positive

Just one scenario Jesse later explains as negative for stocks: Biden Presidency + GOP Senate. All other combinations are likely positive

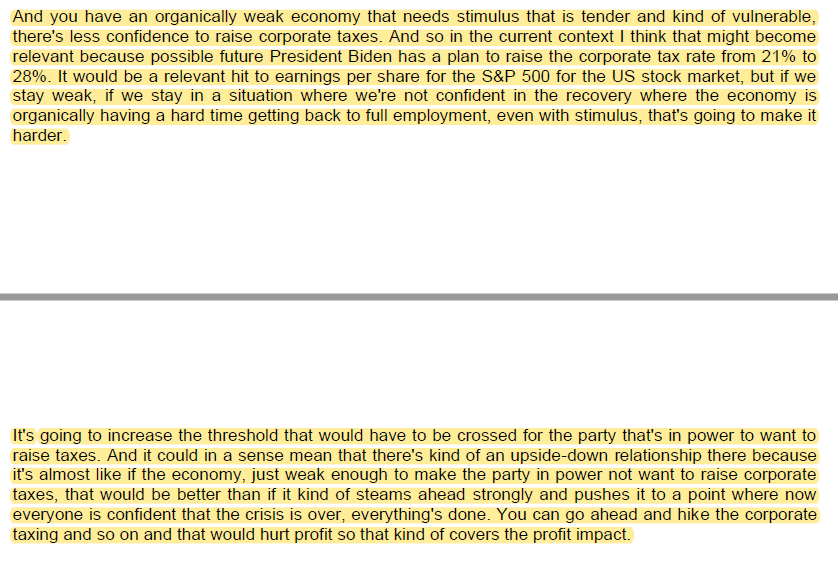

5/ Another upside-down scenario is potential tax hike by Biden. If economy stays weak, he may not do so, but if economy is out of the woods, he may raise corporate taxes which will test $SPY.

6/ This is such a neat and intuitive point. I became lot more comfortable with current market valuation after reading this argument in Jesse's piece a few weeks back.

7/ So why exactly upside down market theory was not at work back in 1929?

Here's why.

Here's why.

8/ Jesse is not concerned about inflation because of all the money injection that happened during Covid.

But this pollyannish view can get tested by a possible Minsky moment. The infamous gridlock in the US political system might come to the rescue of such runway fiscal response

But this pollyannish view can get tested by a possible Minsky moment. The infamous gridlock in the US political system might come to the rescue of such runway fiscal response

9/ Higher inflation itself might not cause too much problem for equities. But there can be some concerns regarding true earnings power as depreciation expense proves to be understated in an inflationary scenario.

But Fed might rescue us again.

But Fed might rescue us again.

10/ Risk in equity markets is never eliminated. It just gets shifted around.

End/ Episode link: investorfieldguide.com/jesse-livermor…

Transcript: investorfieldguide.com/wp-content/upl…

All my twitter threads: mbi-deepdives.com/twitter-thread…

Transcript: investorfieldguide.com/wp-content/upl…

All my twitter threads: mbi-deepdives.com/twitter-thread…

• • •

Missing some Tweet in this thread? You can try to

force a refresh