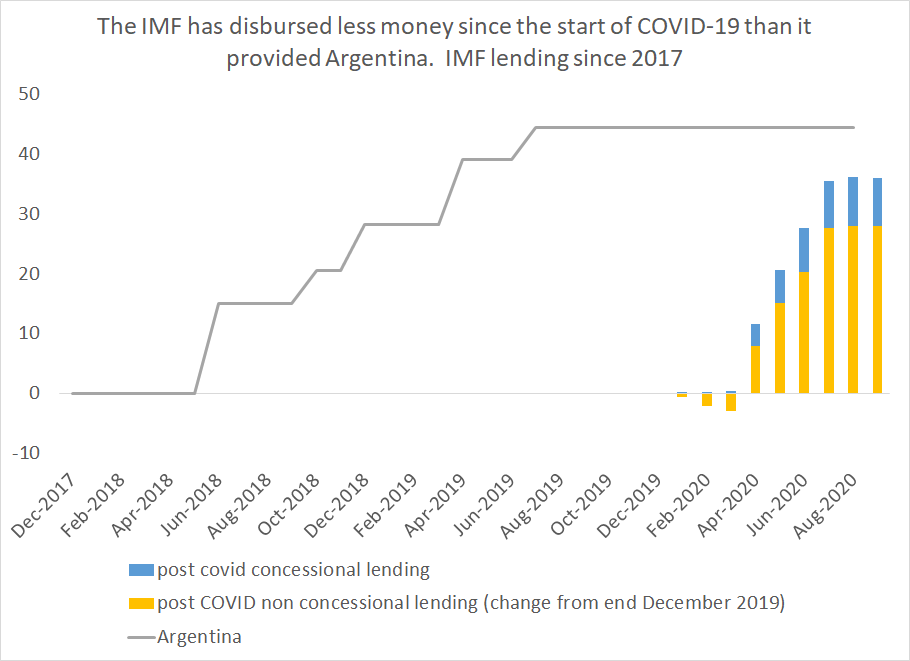

The rapid increase in the U.S. current account account should be hard to miss.

Yet the IMF missed it, throwing off its global forecast

cfr.org/blog/chinas-su…

Yet the IMF missed it, throwing off its global forecast

cfr.org/blog/chinas-su…

The enormous rise in the U.S. trade deficit, the deficit in August was over $200 billion larger than its 2019 average level, has made the U.S. the engine of global demand again ...

(the US current account is likely to be over a percentage point larger than the IMF's forecast)

(the US current account is likely to be over a percentage point larger than the IMF's forecast)

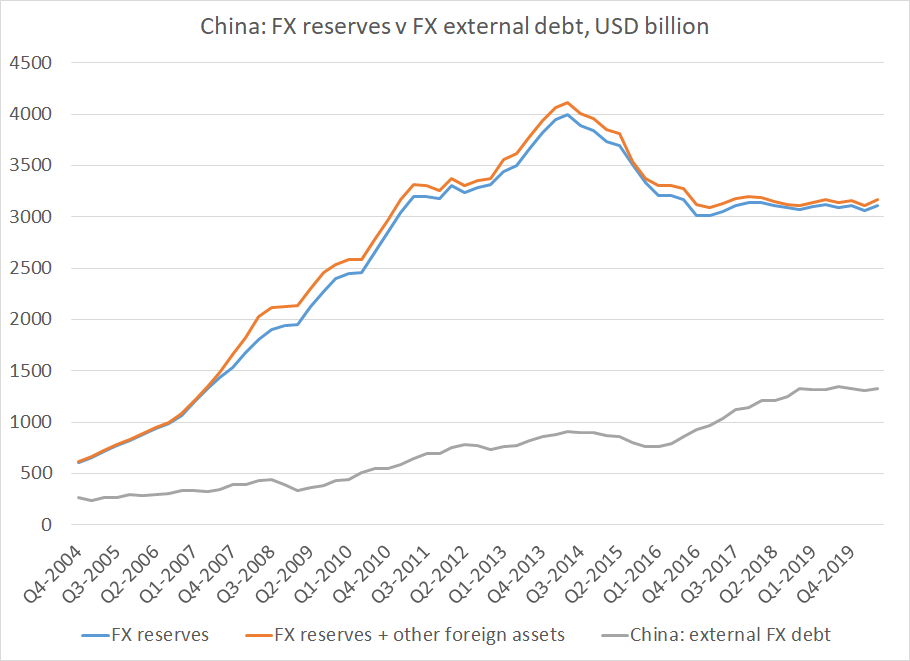

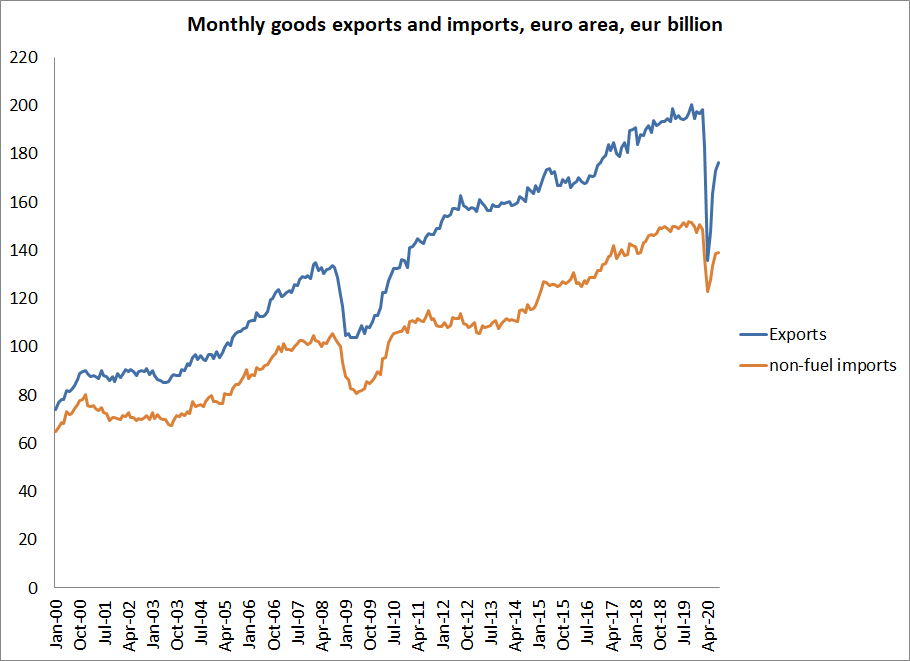

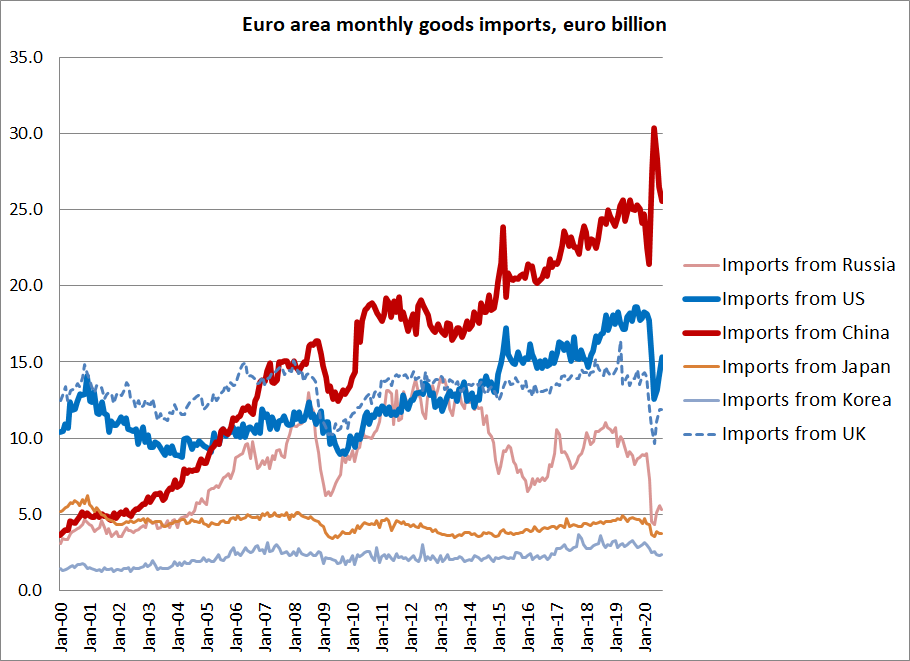

Rather than shrinking, as the IMF argues, Asian imbalances are growing -- propelled by the rise in the U.S. deficit ...

In effect, strong U.S. demand allowed Asia to recover without doing all that much stimulus of its own (especially of household income)

In effect, strong U.S. demand allowed Asia to recover without doing all that much stimulus of its own (especially of household income)

And with broad weakness in the emerging world, capital is again flowing uphill. The emerging economies outside of East Asia are now running a big trade surplus (Turkey excepted)

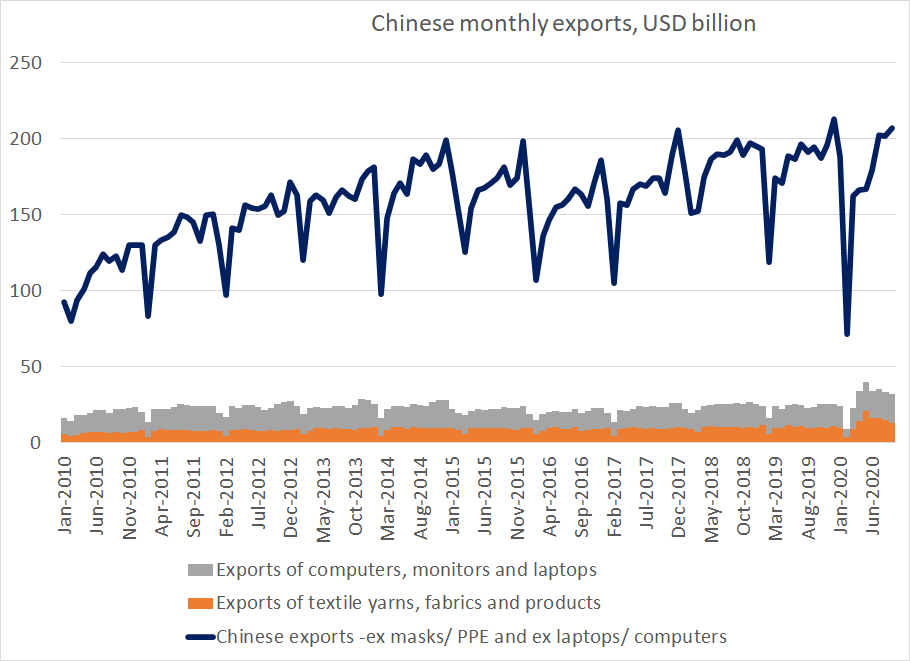

As @DanielAlpert has noted, different trade performance in turn explains the different paths of the industrial recovery in the US and China ...

These are all quite large and interesting swings in the global flow of funds that the IMF essentially ignored -- its section around "imbalances" was framed around "shrinking trade and shrinking imbalances" a story that is now out of date!

imf.org/en/Publication…

imf.org/en/Publication…

• • •

Missing some Tweet in this thread? You can try to

force a refresh