I have been discussing the trends in inflation lately.

Today's report showed more of the same.

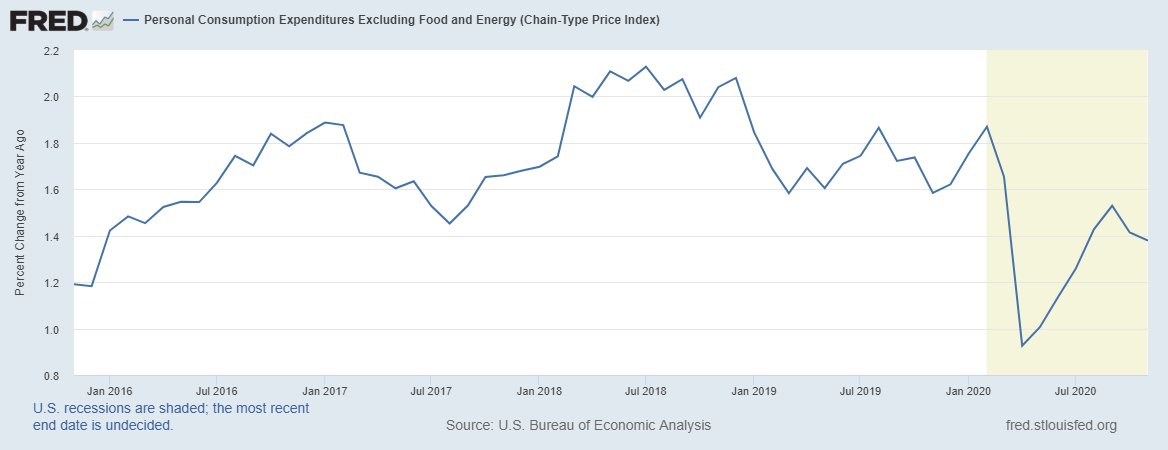

Inflation is coming from the industrial upturn, concentrated in the goods sector while the services sector is showing declining rates of inflation.

1/

Today's report showed more of the same.

Inflation is coming from the industrial upturn, concentrated in the goods sector while the services sector is showing declining rates of inflation.

1/

https://twitter.com/EPBResearch/status/1349072113009713153

Headline inflation ticked up slightly and is mostly a balancing act between rising goods inflation and falling services inflation.

2/

2/

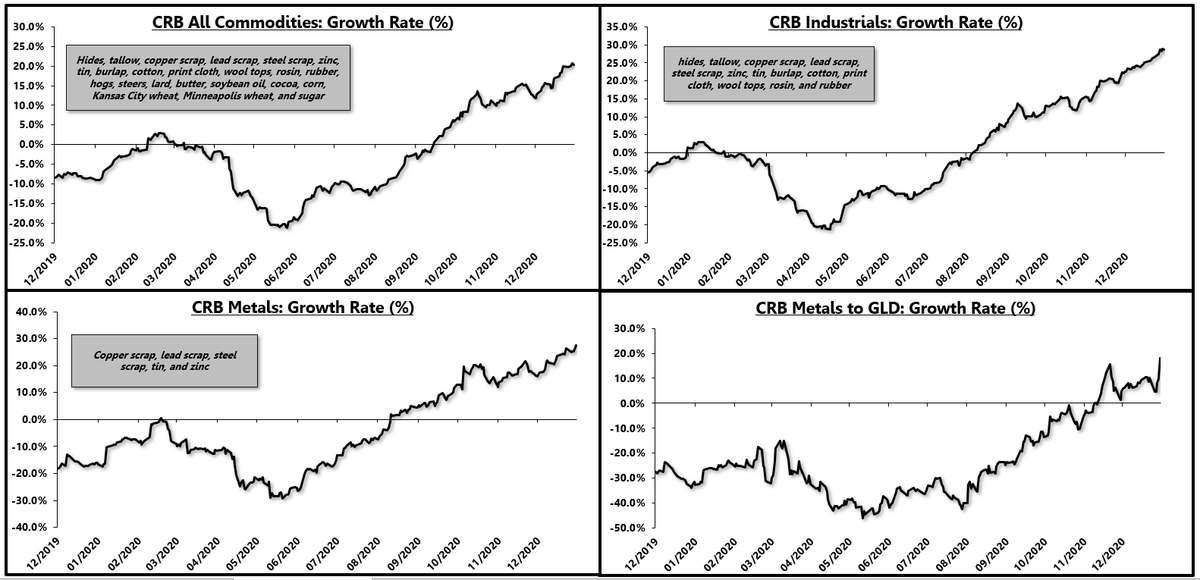

Goods inflation continues to rise, jumping to nearly 4% on a year over year basis.

Goods inflation (and industrial commodities) are rising due to manufacturing backlogs caused by shutdowns and the overall shift to at-home goods consumption and away from services consumption.

3/

Goods inflation (and industrial commodities) are rising due to manufacturing backlogs caused by shutdowns and the overall shift to at-home goods consumption and away from services consumption.

3/

Services inflation was nearly always above the average rate of headline inflation but the trend has reversed with goods inflation now the driver and services inflation dragging down the headline and core.

4/

4/

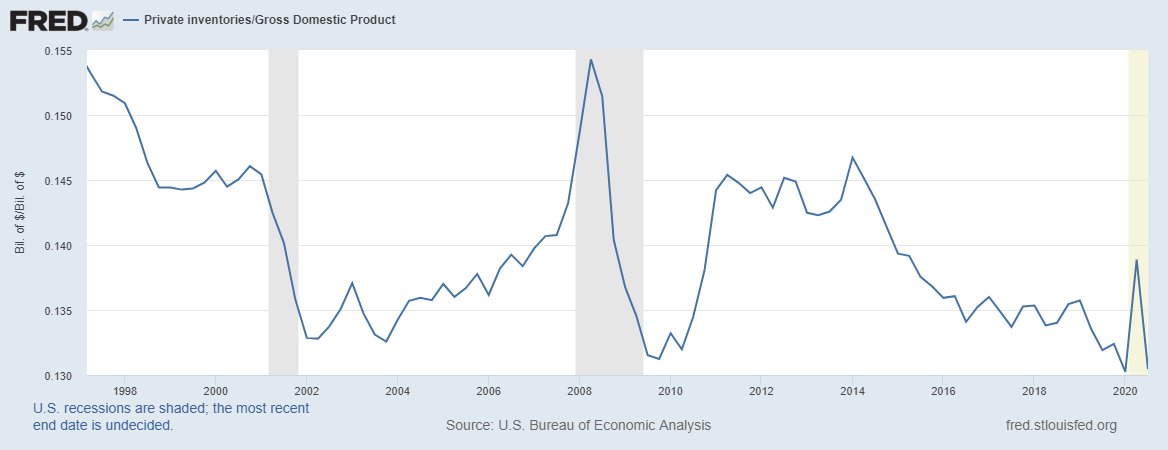

Once the economy re-opens, supply chains are freed and inventories are restocked, goods inflation will start to decline again.

The question is whether services inflation rises to balance the trend or if the permanent damage to the service sector causes a structural decline.

5/5

The question is whether services inflation rises to balance the trend or if the permanent damage to the service sector causes a structural decline.

5/5

• • •

Missing some Tweet in this thread? You can try to

force a refresh