At 11:00am, the House @EnergyCommerce Committee will be holding marathon hearings on not one, not two, but *18* different healthcare bills which would repair & strengthen the #ACA, #Medicaid & #CHIP. Here's the first 9 on the agenda: acasignups.net/21/03/17/prepa…

#HR1790 would reverse the Trump Admin's decision to modify how ACA subsidies & maximum out of pocket expenses are calculated. The Trump version made subsidies weaker/costs higher; reversing it would make subsides stronger/costs lower.

#HR1796 would provide several hundred million dollars in grants for states to streamline their data sharing, set up auto-enrollment & pre-populated applications for enrollment, and help states establish their own state-based individual mandate requirements/penalties.

#HR1872 would reverse the Trump Admin's gutting of HealthCare.Gov's marketing/ outreach budget by codifying $100M/yr to be used specifically for promoting ACA plans. It would also *prevent* promotion of junk plans, & would require language- & audience-specific outreach.

#HR1874 would reverse the Trump Admin's gutting of HC.gov's Navigator/Counselor program budget by codifying $100M/yr for it as well as stopping grants from going to profit-based orgs which promote junk plans.

#HR1875 is an eyebrow-raiser. An Obama exec. order allowed "Short-Term, Limited Duration" plans (#ShortAssPlans) to keep being offered, but restricted them to 90 days & said they couldn't be renewed within the same year (i.e., they had to be short-term & of limited duration).

A *Trump* XO *reversed* Obama's, allowing #ShortAssPlans to be kept all year & letting them be renewed (which, aside from everything else, means they're no longer "short-term" or of "limited duration"). These are the *exact* type of junk plans the ACA was designed to discourage.

Several prior bills would have reset #ShortAssPlan restrictions back to the Obama Admin policy & codified them as such...but #HR1875, which is just 1 sentence long, does something quite different:

It legally categorizes STLDs as INDIVIDUAL HEALTH INSURANCE. This is a Big Deal.

It legally categorizes STLDs as INDIVIDUAL HEALTH INSURANCE. This is a Big Deal.

Right now, "short-term, limited duration" plans aren't technically considered "individual health insurance coverage"...which also means they're not subject to a lot of ACA regulations. Like guaranteed issue. Or community rating. Or essential health benefits...get the picture?

#HR1875 doesn't actually ban #ShortAssPlans. It doesn't even restrict them to 90 days. What it *does* do is require them to meet the same minimum standards of #ACA policies...

...which basically means they'd no longer have any reason to exist in the first place.

...which basically means they'd no longer have any reason to exist in the first place.

The *only* "advantage" #ShortAssPlans have over #ACA plans (amidst a laundry list of shortcomings) is that they have cheaper premiums...*because* of those shortcomings. Make them stop being junk & that advantage goes away.

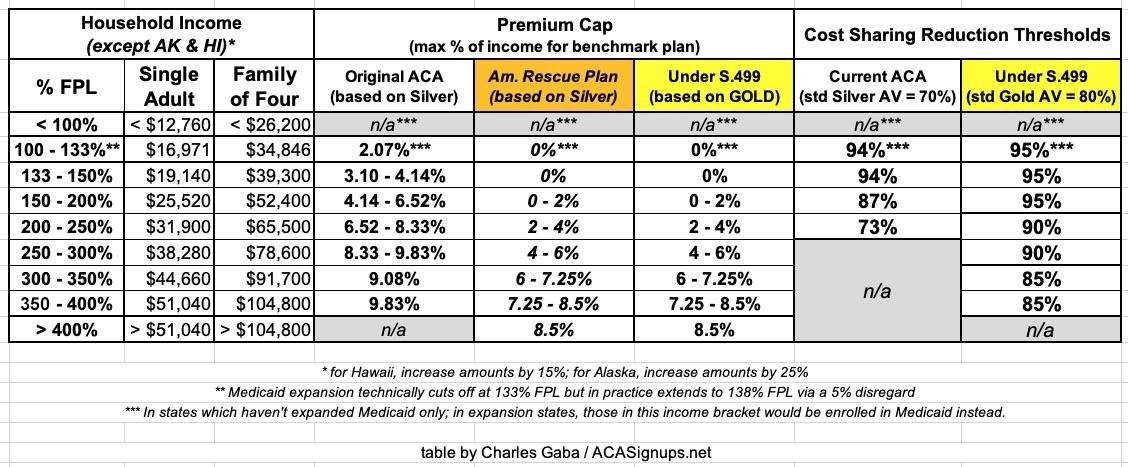

However, if #S499 passes into law as well, there'd be *no further need* for #ShortAssPlans anyway, since #ACA-compliant coverage would be affordable for *everyone*, even those who haven't qualified for subsidies until now.

Sign #S499 & I'm fully onboard w/#H1875.

Sign #S499 & I'm fully onboard w/#H1875.

#HR1878's heart is in the right place, but could actually prove to be a BAD thing depending how it's implemented.

It would provide $10 BILLION/yr for EITHER reinstating a federal *reinsurance* program *or* for direct out-of-pocket assistance.

It would provide $10 BILLION/yr for EITHER reinstating a federal *reinsurance* program *or* for direct out-of-pocket assistance.

More direct assistance would be awesome, but reinsurance can be awkward. I'll write up an explainer soon, but in short, reinsurance can be helpful in some circumstances but *harmful* in others.

#HR1890 attempts to tackle the #SkinnyNetwork problem many #ACA plans have by making the HHS Sec. develop minimum network adequacy standards. It also gives the HHS Sec. the power to step in & regulate rates in states where regulators are seen as being asleep at the switch.

These are both worthy goals, but don't be surprised if a bunch of state insurance commissioners cry foul over the second one and sue over States Rights for what they'd see as HHS stepping on their turf.

#HR1896 would provide $200M in grants for states to establish their own #ACA exchanges. Some states like Oregon & Hawaii flushed a ton of grant money down the toilet in the early days of the ACA, but these days states like NV, PA & NJ are setting them up with (relative) ease.

#HR1896 is interesting because it's a genuinely BIPARTISAN bill to expand the #ACA. It was introduced by @RepAndyKimNJ (D) & @RepBrianFitz (R), both of whom introduced the same bill 2 years ago.

#HR340 would effectively bribe the 12 states which haven't expanded Medicaid yet with even MORE money to do so than the $16 billion they're already being offered under the #AmRescuePlan.

The #AmRescuePlan would increase the federal share of Medicaid spending by 5 points for 2 years if these states stop being assholes & expand Medicaid under the #ACA. That 5 point bump is *more* than the 10% expansion cost they'd have to pay, so they'd actually come out ahead.

#HR340 would have the feds *also* cover that 10% of expansion cost for 3 years, +5-9% for a few years after that, which means if all 12 states took the offer, they'd walk away with the full $16 billion in *pure gains* just for doing something they should've done 7 years ago.

Here's the OTHER 9 healthcare bills to be discussed at today's House @EnergyCommerce Committee hearing. Many of these are more about Medicaid & CHIP than the #ACA specifically, but there's obviously a lot of overlap. Several of these are also BIPARTISAN:

acasignups.net/21/03/20/prepa…

acasignups.net/21/03/20/prepa…

#HR1738: Right now, depending on the state/status, Medicaid/CHIP enrollees have to verify eligibility *every month* which is a royal pain in the ass for them & a massive amount of red tape/admin overhead for the state. This would make them eligible for 12 mo. after starting.

#HR1784: This is another way to pressure the remaining non-expansion to FINALLY expand Medicaid: It would require detailed annual reports on the uninsured who they're screwing over, and would penalize them by up to 1.5 pts of federal funding if they don't issue those reports.

#HR1025: Another bipartisan bill! This would require Medicaid to keep paying at least Medicare rates to primary care physicians. I think it'd make this permanent; could be wrong about that.

#HR66 & #HR1791: Both appear to do the same thing: They'd MAKE CHIP FUNDING PERMANENT instead of letting the GOP hold it hostage every few years. Interestingly, HR66 is *bipartisan*, w/GOP Rep. Vern Buchanan joining Rep. Lucy McBath. The other one is from Rep. Barragan.

#HR1888: This would require 100% FMAP funding for Indian healthcare providers. I assumed the INS was already fully federally funded, but apparently not? I may be misunderstanding, but it sounds like this would expand 100% funding to providers *outside* of reservation territory?

#HR1717: This would make the "spousal impoverishment" Medicaid provision *permanent*, which it really should've been all along. Another bipartisan bill from MI @RepFredUpton & @RepDebDingell.

#HR1880: This is also from @RepDebDingell: It would permanently codify the "Money Follows the Person" program, which requires Medicaid funding to follow enrollees as they move from nursing homes/etc. to home/community-based services.

FINALLY, there's #HR1390 from @RepSusanWild, which would beef up #CHIP funding for another 2 years in response to the COVID pandemic.

SO THERE YOU HAVE IT: 18 bills to be discussed in a day-long marathon session by the @EnergyCommerce Health subcommittee starting right about...NOW: energycommerce.house.gov/committee-acti…

Note: If you'd like to support my healthcare policy analysis/advocacy work, you can do so here: acasignups.net/donate:

P.S. One bill which *isn't* on the agenda today is @RepUnderwood's #HR369, which would make the #AmRescuePlans' #ACA subsidy expansion *permanent*. I'm pretty sure that's because hearings on it were already baked into the #ARP itself.

I'm also a bit surprised that none of the bills on today's agenda tackle the #FamilyGlitch. The Biden Admin's HHS is supposedly gonna attempt to fix this via regulatory changes, but it would still be much better to codify that fix via legislation.

P.P.S. Also, as much of a bummer as it is to remind folks of this on #ACA11, there's STILL a pending Supreme Court decision which could potentially strike down the ENTIRE #ACA. The ruling is expected sometime between now and July.

acasignups.net/21/02/05/democ…

acasignups.net/21/02/05/democ…

• • •

Missing some Tweet in this thread? You can try to

force a refresh