This is a long, wonky post, but it also includes the simplest explanation I could give of how #SilverLoading works and why a lot of people were eligible for $0 premium Bronze or *Gold* plans even before the #AmRescuePlan expanded them further.

acasignups.net/21/03/29/old-l…

acasignups.net/21/03/29/old-l…

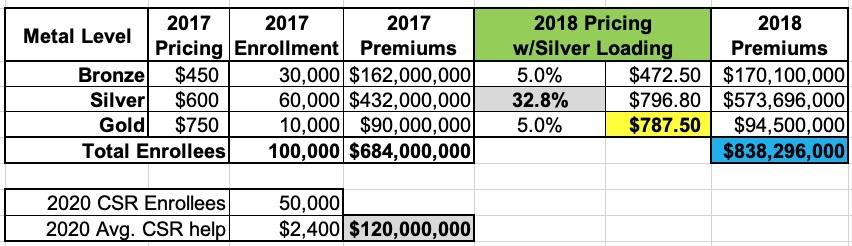

In short: Here's some sample 2017 Bronze, Silver & Gold premium & enrollment data. Let's say 2018 medical trend went up 5%. Meanwhile, let's say 1/2 the enrollees received CSR help averaging $2,400 apiece.

That's $120M in CSR reimbursements owed to the carriers from the feds.

That's $120M in CSR reimbursements owed to the carriers from the feds.

In late 2017, Donald Trump cuts off CSR reimbursements, figuring this will cause millions of low-income enrollees to lose their subsidies *or* for all the carriers to drop out of the ACA market (causing it to "blow up" and "collapse"), or both, to avoid eating a $120M loss.

INSTEAD, the carrier does something unexpected (by Trump, not by anyone who understands how the ACA works): They simply *jack up the premiums by enough to make up for the $120M which Trump was gonna stiff them out of*.

If they do this evenly, it's called Broad Loading, like so:

If they do this evenly, it's called Broad Loading, like so:

Broad Loading would mean EVERY plan (Bronze, Silver, Gold) would have their premiums jump by an ugly 23%. Some carriers in some states did this. However, MOST carriers in MOST states did something more clever: They dumped ALL of the "lost CSR cost" on Silver plans exclusively.

This is called #SilverLoading, and it looks like this: Bronze & Gold go up the normal amount, but Silver skyrockets by 33%. This is basically what happened in 2018.

Result? Bronze & Gold enrollees are held harmless by the CSR cut-off, while Silver enrollees are hosed, right?

Result? Bronze & Gold enrollees are held harmless by the CSR cut-off, while Silver enrollees are hosed, right?

Well, if it weren't for the #ACA's subsidy system, yes...but since most enrollees are subsidized, and the subsidies are based on the price of Silver plans, guess what happens instead? The subsidies go up by roughly the same amount to keep the net Silver price the same.

This also caused *another* very strange effect as well, however: the *Gold* plan now cost *less* than the Silver plan. Gold has just become a better value for many people. Furthermore, because the increased subsidies can be applied to Bronze, Silver *or* Gold...

...this means that a lot of people can get a Bronze plan for free, or a Gold plan for next to nothing (or even for free as well in some cases).

That's #SilverLoading in a nutshell.

Read the piece for the rest of the story before & after that, however: acasignups.net/21/03/29/old-l…

That's #SilverLoading in a nutshell.

Read the piece for the rest of the story before & after that, however: acasignups.net/21/03/29/old-l…

• • •

Missing some Tweet in this thread? You can try to

force a refresh