All ECB QE data are out. A thread in charts.

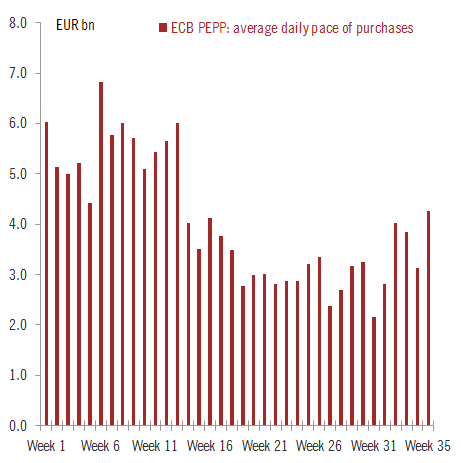

First things first, the pace of PEPP purchases halved to €10.6bn last week, the lowest this year post Christmas break. I'm sure it's all due to Easter and that "significantly higher" purchases are just around the corner.

First things first, the pace of PEPP purchases halved to €10.6bn last week, the lowest this year post Christmas break. I'm sure it's all due to Easter and that "significantly higher" purchases are just around the corner.

I mean, seriously. The ECB hasn't even started to front-load PEPP purchases in any meaningful way, and the hawks are already talking about tapering? Here's another Daft Punk reference for you: Doin' it right.

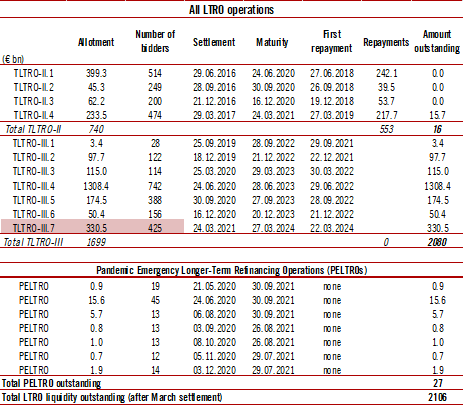

Moving on to the monthly QE data breakdown.

Big picture: ahead of the expected pick-up in PEPP purchases, it's still very much a *Public* Pandemic Emergency Purchase Programme, although corporate debt purchases have increased slightly in Feb-Mar. CP continue to roll off.

Big picture: ahead of the expected pick-up in PEPP purchases, it's still very much a *Public* Pandemic Emergency Purchase Programme, although corporate debt purchases have increased slightly in Feb-Mar. CP continue to roll off.

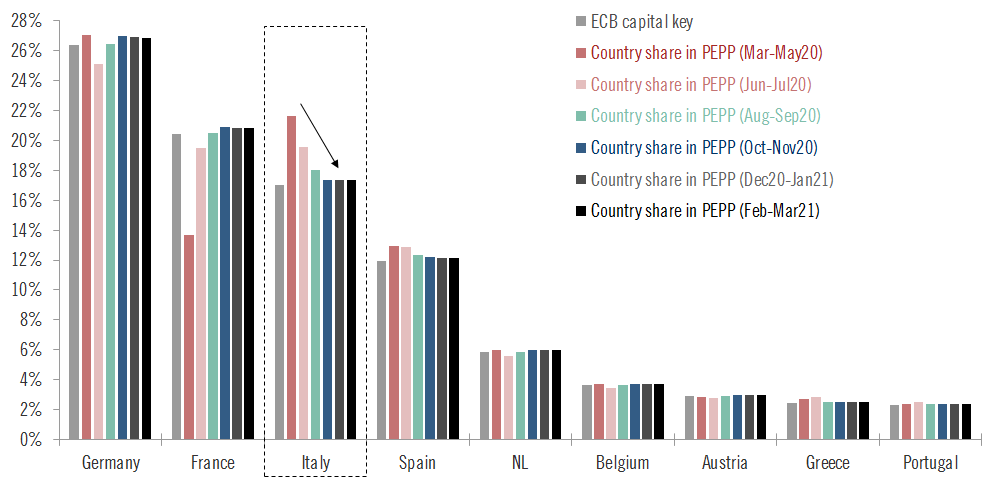

In terms of the breakdown of PEPP purchases across countries, there has been no change in composition in 6 months. The ECB is sticking to capital keys almost perfectly. The PEPP's flexibility is no longer being used.

The average maturity of German/core PEPP purchases continues to rise, but it's still below the maturity of the eligible universe (with the exception of Austria).

In terms of PEPP breakdown, note that Supranationals made up for 10.2% of total public debt purchases (€13.4bn) for four months in a row, yet not enough to compensate for a slow start in 2020 (5-7%) despite EU bonds issuance.

Moving to the APP, no big change either in terms of overall pace or composition of purchases. Deviations from capital keys were small in March, leaving the cumulative deviations broadly unchanged.

• • •

Missing some Tweet in this thread? You can try to

force a refresh