Thanks for comments/thoughts, I'll ponder them.

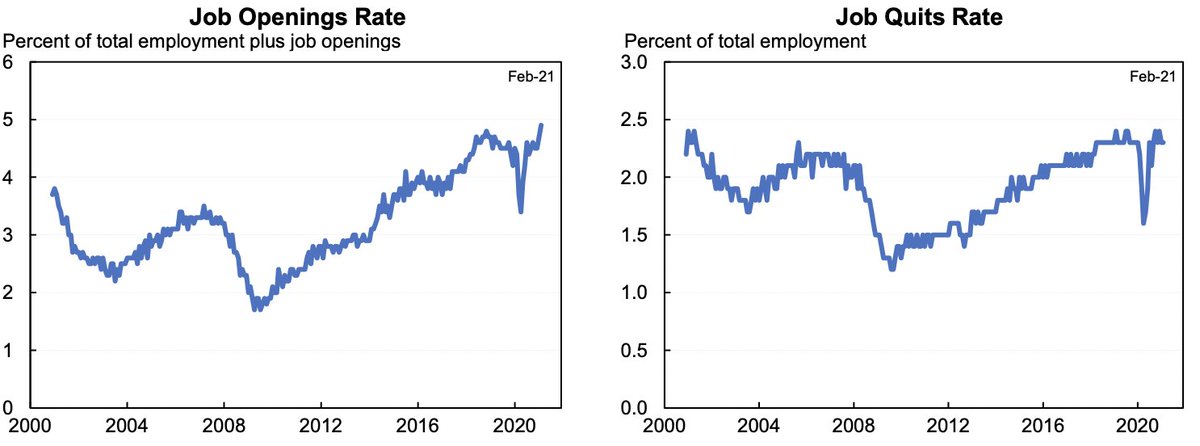

This all started out because I see mixed signals in the labor market: (1) lots of jobs down is the most obvious (you cite it), but also (2) openings up and (3) wages up.

Moreover that was 2 months ago, improved rapidly since then.

This all started out because I see mixed signals in the labor market: (1) lots of jobs down is the most obvious (you cite it), but also (2) openings up and (3) wages up.

Moreover that was 2 months ago, improved rapidly since then.

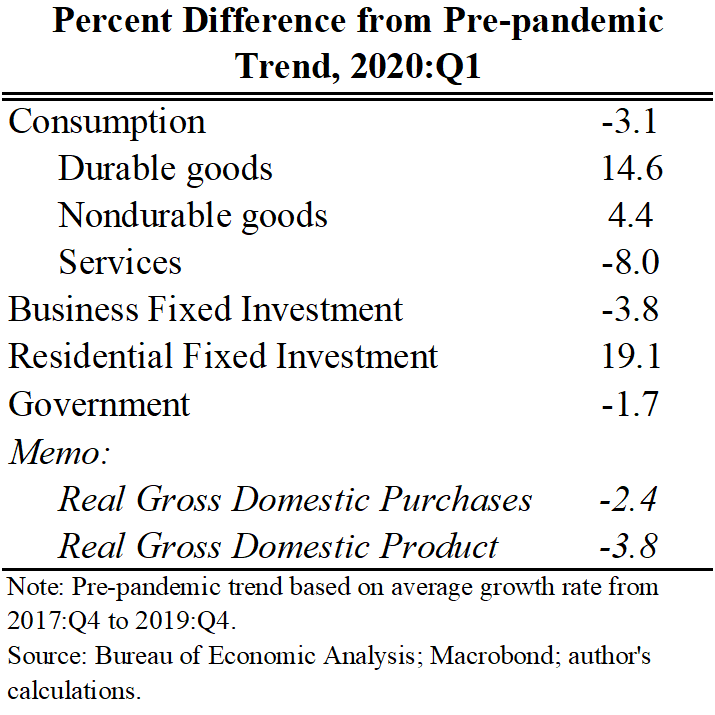

https://twitter.com/joshbivens_DC/status/1389965411798638595

Some of the tone, even of your tweets, sounds like the economy is like it was in 2010 or 2011. But it was more like somewhere in the 2017 period plus or minus and moving forward rapidly.

I'm a big believer in rebalancing policy towards fiscal, both for stimulus, social insurance, growth and more. Monetary policy can help support that rebalancing. Whatever you think about the appropriate time for interest rate liftoff it was moved up by the stimulus. That is good.

We have a lot of demand. At this stage I am more worried about supply. The main levers on supply are vaccines, reopening, childcare, etc.

And, I know you disagree, but I don't understand why UI will be more generous in July than it was during the massive COVID wave in January.

And, I know you disagree, but I don't understand why UI will be more generous in July than it was during the massive COVID wave in January.

I don't think Keynes is exactly right for this because he was talking about a demand shock. But what we have now is a positive demand shock (thanks for fiscal and monetary policy) and a lingering negative supply shock.

Finally, I'm surprised you appear reject the notion that reservation wages matter. If a worker's outside option goes up then their reservation wage goes up, labor supply falls, and wages rise. That is a dynamic I've seen you praise before.

Which is to say, reservation wages are a real thing. You might have some story about why raising reservation wages won't negatively impact employment (and it might be a non crazy story, although would be stronger in the absence of so much stimulus from fiscal policy).

Not saying I want people to be paid less. Just saying it is silly to say unemployment definitionally doesn't exist because of reservation wages. Of course unemployment exists.

So also silly to say labor shortages definitionally don't exist because employers won't raise wages.

So also silly to say labor shortages definitionally don't exist because employers won't raise wages.

• • •

Missing some Tweet in this thread? You can try to

force a refresh