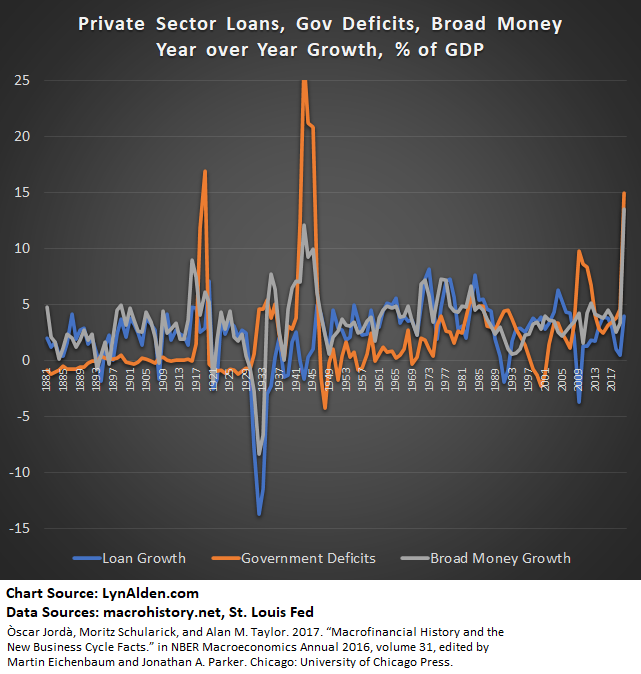

Several people have correctly pointed out that bank loans haven't kept up with bank deposits.

However, if you add bank holdings of Treasuries to their loans, the gap fills by quite a bit. The rest is mainly excess reserves.

This is because, as @LukeGromen has elegantly pointed out a number of times, banks *are* lending, albeit mainly to the federal government.

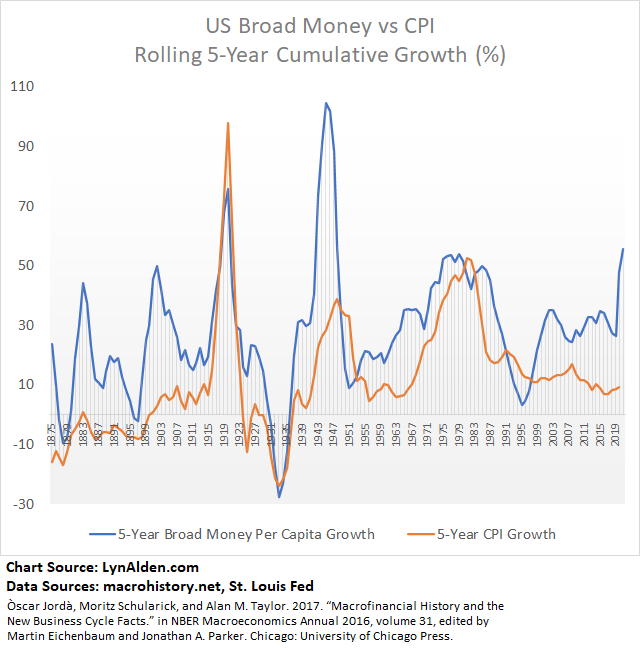

It's like the 1940s more-so than the 1970s.

It's like the 1940s more-so than the 1970s.

Treasuries and agencies, to be specific.

• • •

Missing some Tweet in this thread? You can try to

force a refresh