Global monetary debasement is setting the stage for a rude awakening.

Here is a thread.

👇👇👇

Here is a thread.

👇👇👇

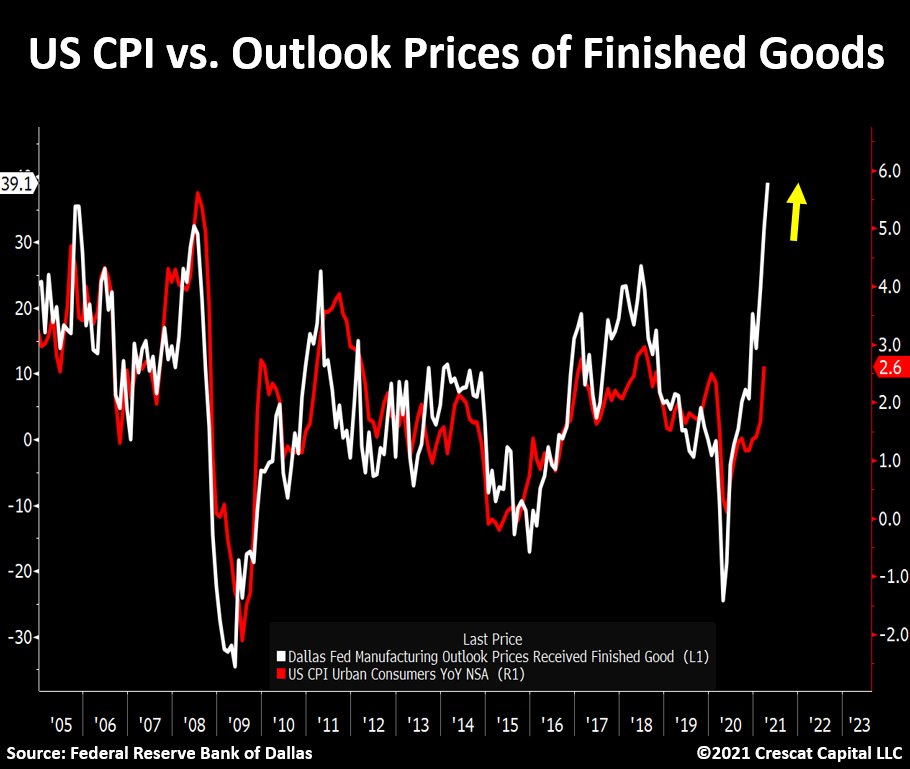

For the first time since the 1970s the sense of fiat currency erosion relative to financial assets and consumer prices due to misguided policies has penetrated the mindset of investors in a significant way.

The inflation genie is out of the bottle and policy makers are unable to sustainably ease off the liquidity pedal.

Financial repression has become essential to secure the health of the economy at the current levels of overall debt.

Financial repression has become essential to secure the health of the economy at the current levels of overall debt.

Nonetheless, easy and cheap access to capital has also been one of the key reasons for the historical disconnection between asset prices and fundamentals.

In fact, the sheer amount of financial assets today that trade at near record multiples is truly concerning.

In fact, the sheer amount of financial assets today that trade at near record multiples is truly concerning.

Preventing a collapse in risky assets has become a true policy constraint for monetary authorities.

Different than other times in history, the Fed’s ability to allow the cost capital to substantially rise is incredibly limited.

Different than other times in history, the Fed’s ability to allow the cost capital to substantially rise is incredibly limited.

Ultimately, policy makers have their hands tied and will be forced to counter deflationary pressures in financial assets with further liquidity.

Igniting an inflationary environment is the path of least resistance.

Igniting an inflationary environment is the path of least resistance.

To use the US stock market as an example:

The 5-year cyclically adjusted earnings yield is now near all-time lows.

In other words, investors are undeservedly paying excessive prices relative to bottom-line fundamentals.

The 5-year cyclically adjusted earnings yield is now near all-time lows.

In other words, investors are undeservedly paying excessive prices relative to bottom-line fundamentals.

Going back over a century of historical data:

Such depressed earnings’ yields have always led to very significant market meltdowns:

Great Depression.

1937-8 Recession

Tech Bubble.

Such depressed earnings’ yields have always led to very significant market meltdowns:

Great Depression.

1937-8 Recession

Tech Bubble.

For every one of these periods, the market unexpectedly reversed from very bullish multi-year trends with an average subsequent 3-year performance of -53%.

Naturally, as different opportunities present themselves over time, market positioning and capital allocation tend to change drastically every five years or so causing major reversal trends.

We strongly believe investors are poised to experience another one of these significant market rotations where capital allocation moves away from historically expensive equities to then find its way into cheap tangible assets, i.e. commodities.

Now let’s address the elephant in room.

You would think that a low interest rate environment would be positive for stocks, but that is far from the truth.

The problem is that inflation is running much higher than interest rates.

You would think that a low interest rate environment would be positive for stocks, but that is far from the truth.

The problem is that inflation is running much higher than interest rates.

When we look at valuations of equities versus 10-year real yields in the last 120 years, equity fundamental multiples significantly compressed when real yields were negative for a long period of time.

To be fair, however, this is the first time we have seen negative 10-year real rates with valuations at historic levels.

Also, to recall:

Commodities performed exceptionally well during the three highlighted times.

Also, to recall:

Commodities performed exceptionally well during the three highlighted times.

On the other hand, we believe inflation will continue to surprise to the upside in the following years.

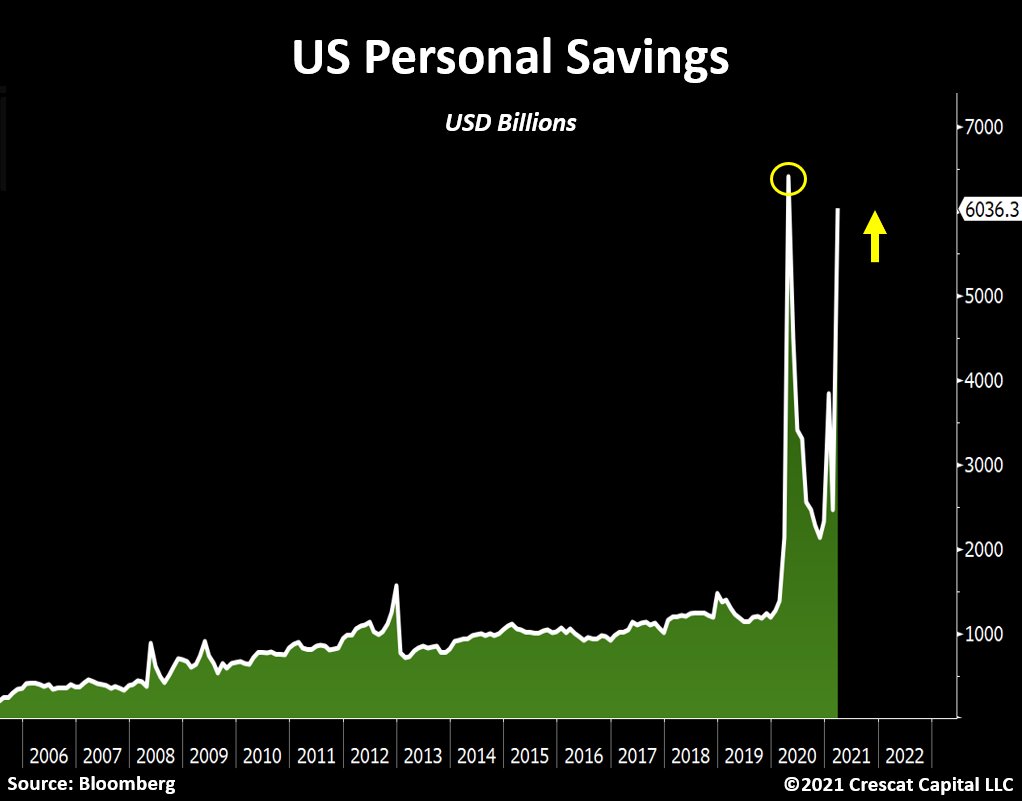

The combination of Fed stimulus to finance historical amounts of government spending has led to one of the largest wealth transfers in history.

The combination of Fed stimulus to finance historical amounts of government spending has led to one of the largest wealth transfers in history.

Since the GFC, the increase in government debt has been directly linked to the increase in net worth of the US population.

One important difference from prior years, however, is that fiscal policies are increasingly becoming more focused on the bottom 50%.

One important difference from prior years, however, is that fiscal policies are increasingly becoming more focused on the bottom 50%.

The US fiscal deficit problem has somewhat improved since March of this year.

The deficit now stands at -12% of GDP, which is 6 pct pts better than its prior lows at -18.5%.

The issue is that this number still is 2 pct pts lower than the worst levels reached during the GFC.

The deficit now stands at -12% of GDP, which is 6 pct pts better than its prior lows at -18.5%.

The issue is that this number still is 2 pct pts lower than the worst levels reached during the GFC.

The US government is determined to pursue a fiscal agenda that has four main fronts:

• The Green Revolution

• An Infrastructure Revamp

• Peak Inequality

• A Fiscal Arms Race with China

• The Green Revolution

• An Infrastructure Revamp

• Peak Inequality

• A Fiscal Arms Race with China

It is hard to believe that with such an ambitious agenda government spending will not remain aggressive going forward.

We think fiscal deficits will continue to run at double-digits for the next years.

We think fiscal deficits will continue to run at double-digits for the next years.

The issue, however, is that in addition to the extreme levels of government stimulus, the US trade balance is already turning significantly lower and likely to continue to deteriorate.

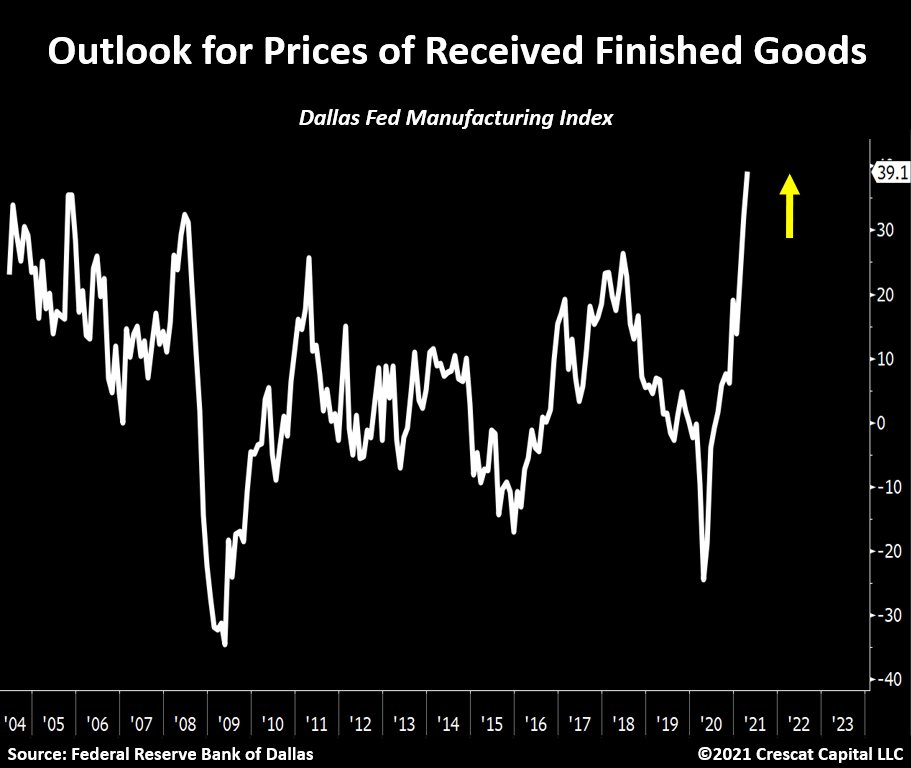

Now let’s get back to the inflation part of the thesis:

For the last four decades, cyclical increases in inflationary forces have been short lived.

For the last four decades, cyclical increases in inflationary forces have been short lived.

Aside from a steady downward trend in money velocity, one of the key reasons why inflation has not yet grown more sustainably is due to a secular decline in wage and salary growth since the late 1970s.

However, we think we are experiencing the beginning of a structural shift in the growth of workers’ remuneration.

Most investors have been paying close attention to the wage growth tracker by the Atlanta Fed which continues to show very muted changes since the pandemic started.

Most investors have been paying close attention to the wage growth tracker by the Atlanta Fed which continues to show very muted changes since the pandemic started.

The issue with this index is that it applies a sample of only 60,000 households or less than 0.04% of the total amount of employed Americans.

We think the most accurate calculation is to look at the wages and salaries aggregate number divided by the number of employed persons.

We think the most accurate calculation is to look at the wages and salaries aggregate number divided by the number of employed persons.

Our own measurement is now growing by 14% on a 24-month basis.

Similar to what Americans experienced in the early 60s to the late 70s, we think we are at the very beginning of an upward inflection in wages and salaries.

Similar to what Americans experienced in the early 60s to the late 70s, we think we are at the very beginning of an upward inflection in wages and salaries.

Finally, let’s talk about portfolio positioning.

What we view as particularly exciting in the current macro environment is the commodities market.

In our analysis, the natural resource industries have turned into remarkably profitable businesses in the last several quarters.

What we view as particularly exciting in the current macro environment is the commodities market.

In our analysis, the natural resource industries have turned into remarkably profitable businesses in the last several quarters.

Aside from the coal industry, we view the entire segment as an attractive investable opportunity.

The aggregate free-cash-flow now generated by commodity producers is growing at a pace we have not seen in the last 30 years.

The aggregate free-cash-flow now generated by commodity producers is growing at a pace we have not seen in the last 30 years.

In the table below, we provided 6 different fundamental metrics for commodity producers with a market cap above $1B in the Canadian & US stock exchanges.

Some key takeaways:

Oil and gas companies appear to be the cheapest on a free-cash-flow yield basis but are also significantly more levered.

Base metals’ stocks performed well recently and therefore show better growth but worse value metrics.

Oil and gas companies appear to be the cheapest on a free-cash-flow yield basis but are also significantly more levered.

Base metals’ stocks performed well recently and therefore show better growth but worse value metrics.

However, one thing stood out:

Precious metals’ companies were clearly the most attractive on a growth, balance sheet strength, valuation, and quality basis

Precious metals’ companies were clearly the most attractive on a growth, balance sheet strength, valuation, and quality basis

Aside from the strong bottom-line growth and relatively high free-cash-yield, the margins for gold and silver companies are significantly better than the other commodity producers.

Although natural resource companies are capital intensive businesses, precious metals’ producers have a much cleaner balance sheet profile than the others.

On a side note:

Among some of the important metrics to analyze how early we are in the precious metals cycle is the level of merger and acquisition activity in the industry.

Among some of the important metrics to analyze how early we are in the precious metals cycle is the level of merger and acquisition activity in the industry.

As shown in the chart below, the M&A cycle has not even started yet.

Senior miners have become true free-cash-flow machines at these metal prices.

Senior miners have become true free-cash-flow machines at these metal prices.

We have not seen this level of net cash accumulation in a long time, setting up a flood gate of liquidity for the following years.

In our view, it is just a matter of time before major producers look for high-quality exploration companies as acquisition candidates.

In our view, it is just a matter of time before major producers look for high-quality exploration companies as acquisition candidates.

To conclude:

We favor a larger exposure to gold and silver companies as we remain highly convicted that the underlying monetary metals will benefit the most from the current macro environment.

We favor a larger exposure to gold and silver companies as we remain highly convicted that the underlying monetary metals will benefit the most from the current macro environment.

Lastly, we have a sizeable position in base metals and also hold energy and agricultural companies in our large cap strategy.

Hope you enjoyed this thread.

Here is our latest research letter:

crescat.net/august-researc…

Hope you enjoyed this thread.

Here is our latest research letter:

crescat.net/august-researc…

• • •

Missing some Tweet in this thread? You can try to

force a refresh