1/

It's funny when I have called some cos to reflect a ~65 pricing for example in the recent top, the counter argument has been many times that they are trading at a huge discount to the project NAV or NPV. How many of these ppl have actually done dcf analysis by themselves?

It's funny when I have called some cos to reflect a ~65 pricing for example in the recent top, the counter argument has been many times that they are trading at a huge discount to the project NAV or NPV. How many of these ppl have actually done dcf analysis by themselves?

https://twitter.com/BambroughKevin/status/1448998238481174531

2/

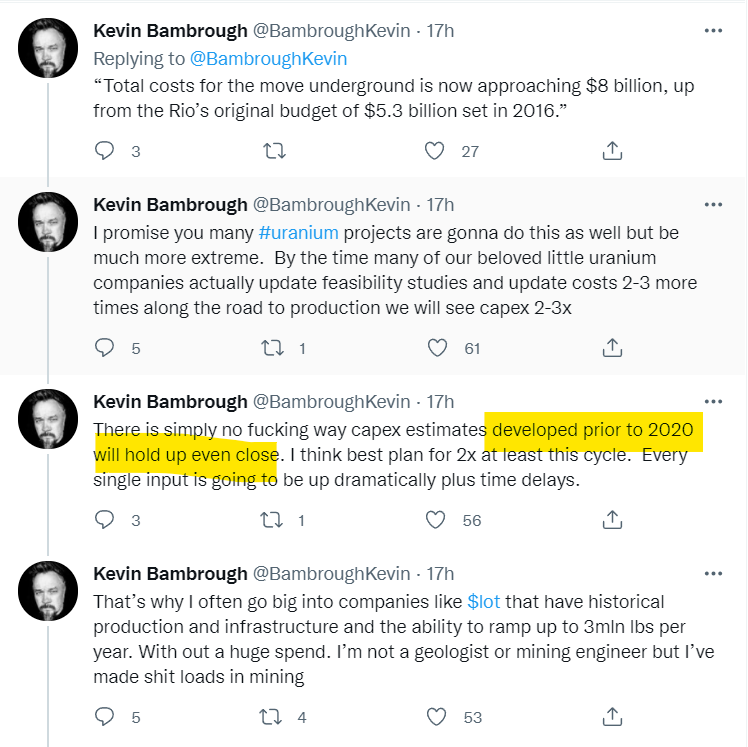

Depending on when these studies have been released and what parameters they have used, I think Kevin knows his stuff. Typically 1.5x to 2.5x is a reasonable factor to capex.

Depending on when these studies have been released and what parameters they have used, I think Kevin knows his stuff. Typically 1.5x to 2.5x is a reasonable factor to capex.

3/

Opex is affected by currency exchange rates, energy prices, labour availability and price among other things. Are these at par on how you see world going from here? Typically use growth rate for costs.

Opex is affected by currency exchange rates, energy prices, labour availability and price among other things. Are these at par on how you see world going from here? Typically use growth rate for costs.

4/

The product price might actually be the easiest thing to estimate in a NPV .

The product price might actually be the easiest thing to estimate in a NPV .

5/

Time and discount rates are huge factors in valuation. Typically add few years and use basic rate 8% to all, for comparison purposes.

Time and discount rates are huge factors in valuation. Typically add few years and use basic rate 8% to all, for comparison purposes.

6/

If a company NPV/NAV is robust through a proper sensitivity analysis, you are on to something.

If a company NPV/NAV is robust through a proper sensitivity analysis, you are on to something.

7/

Sure, valuation might not matter. It's most likely that we will overshoot all the valuations there are. Is cash flow or earnings valuation useless then? Well, thats up to you to decide. I think it has its place.

Sure, valuation might not matter. It's most likely that we will overshoot all the valuations there are. Is cash flow or earnings valuation useless then? Well, thats up to you to decide. I think it has its place.

• • •

Missing some Tweet in this thread? You can try to

force a refresh