Amplitude is the first pure-play analytics SaaS company to IPO in quite a while

It's growing a stunning 57% at $150m+ ARR ... and that's up from 50% just a year ago

It's a $7B leader so many of us rely on in our products

5 Interesting Learnings: 🔽🔽🔽🔽🔽

It's growing a stunning 57% at $150m+ ARR ... and that's up from 50% just a year ago

It's a $7B leader so many of us rely on in our products

5 Interesting Learnings: 🔽🔽🔽🔽🔽

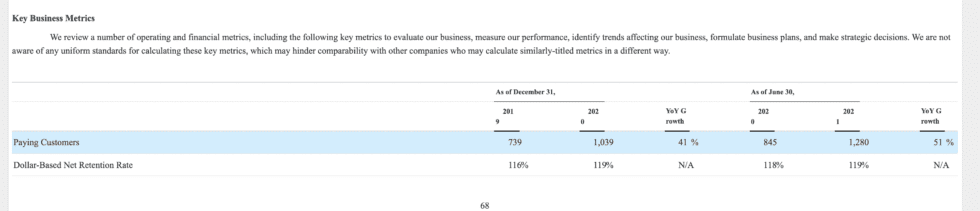

#1. 1,200 total paying customers, with 300 of them at $100k ARR and 22 at $1m+ ARR

Amplitude has consistently gone upmarket, but not radically. This is the sort of organic upmarket path a lot of us see, growing more enterprise each year:

Amplitude has consistently gone upmarket, but not radically. This is the sort of organic upmarket path a lot of us see, growing more enterprise each year:

#2. Customer count growing as fast as revenue — rare, & a great sign for future

New customers grew from +41% in 2020 to +51% in 2021! Most leaders at scale with high NRR get more & more revenue from existing base. Having that high a ratio is a strong sign of future growth.

New customers grew from +41% in 2020 to +51% in 2021! Most leaders at scale with high NRR get more & more revenue from existing base. Having that high a ratio is a strong sign of future growth.

#3. Use overages to renegotiate contracts -- but not so much to charge per event

While Amplitude charges per volume, in part, it doesn’t make a material amount from overages. Rather, it uses overage events to trigger a call from sales to buy more.

While Amplitude charges per volume, in part, it doesn’t make a material amount from overages. Rather, it uses overage events to trigger a call from sales to buy more.

#4. 119% NRR. Strong, but not at crazy levels of some developer apps.

119% is strong NRR, but on its own, not the crazy high we’ve seen with some adjacent Cloud players. But plenty strong to fuel growth for a decade. A good comp if you are like Amplitude.

119% is strong NRR, but on its own, not the crazy high we’ve seen with some adjacent Cloud players. But plenty strong to fuel growth for a decade. A good comp if you are like Amplitude.

#5. Amplitude is accelerating — from 50% growth to 57% at $150m ARR.

This is super impressive and what we’re seeing from so many Cloud leaders. The best of the best are not just maintaining growth rates we haven’t seen before -- they’re growing even faster at scale. Amazing

This is super impressive and what we’re seeing from so many Cloud leaders. The best of the best are not just maintaining growth rates we haven’t seen before -- they’re growing even faster at scale. Amazing

And a few bonus notes:

#6. 245 employees in Sales & Marketing — vs. 101 in Engineering / R&D. It does take an army to support an analytics platform, even with a free edition.

#7. Founders own about 16% together at IPO. CEO Spencer Skates owns 8.5%, CTO Curtis Liu 8.0%

#6. 245 employees in Sales & Marketing — vs. 101 in Engineering / R&D. It does take an army to support an analytics platform, even with a free edition.

#7. Founders own about 16% together at IPO. CEO Spencer Skates owns 8.5%, CTO Curtis Liu 8.0%

• • •

Missing some Tweet in this thread? You can try to

force a refresh