1/ Some helpful charts from Hayden Capital's 73 page piece on $COIN:

Users trade more frequently over time (grey is users trading 1x per month, blue is >5x per month):

Users trade more frequently over time (grey is users trading 1x per month, blue is >5x per month):

2/ Number of global crypto users continued to grow despite the 50% fall in #BTC etc from April to June 21. #ETH user adoption continued rapid growth too.

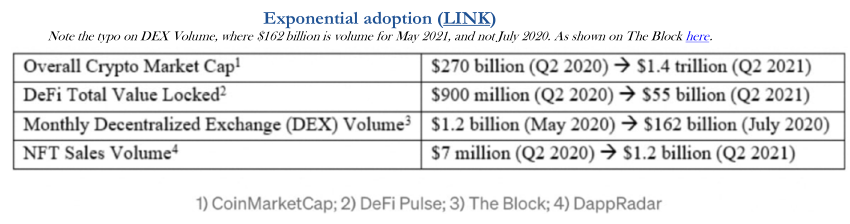

3/ Table shows some exponential adoption metrics since Q2 2020 (note the $162bn DEX Volume shown in July 2020 should be May 2021):

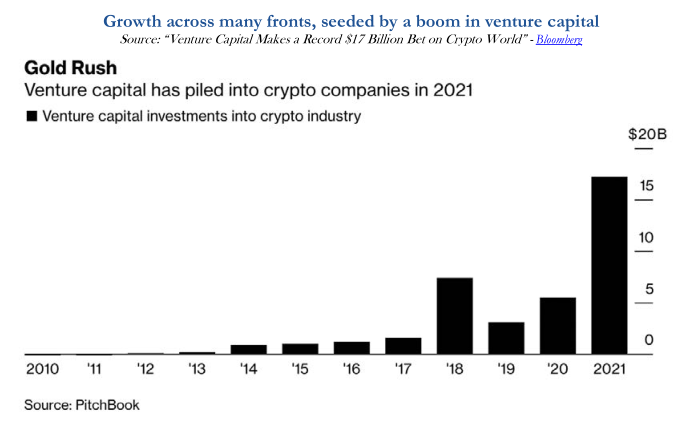

4/ VC firms have invested $17bn into crypto so far in 2021, up from $6bn in 2020:

5/ Hayden Capital adjust crypto exchange mkt shares to look at just US regulated spot markets. On that basis, $COIN has 55% share:

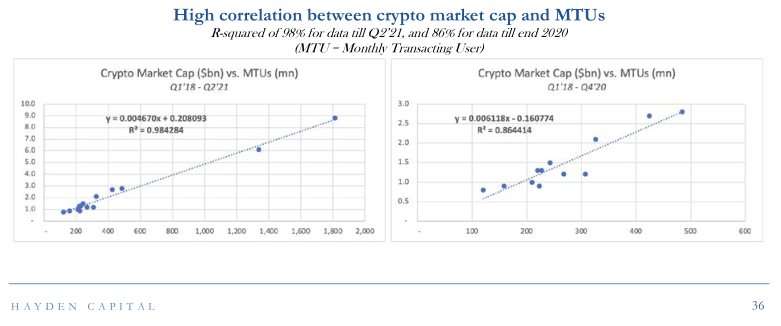

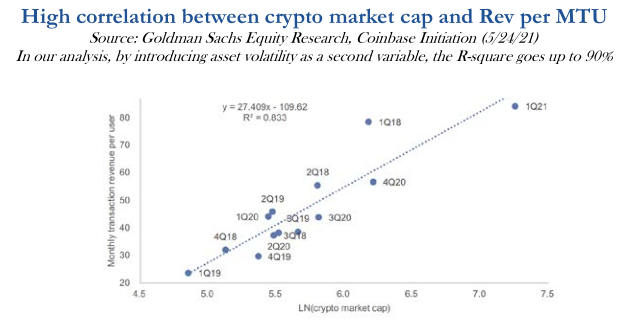

6/ Interesting charts that show the high correlation between total crypto market and monthly transacting users. r squared is 98% for data up until Q2 21 or 86% up until end 2020 (the recent extremely strong data reduces the variability in the earlier data):

7/ Also, there is a high correlation btw total crypto mkt cap and revenue per monthly transacting user. Thus $COIN doubly benefits from growth in total crypto mkt cap in terms of no of users and rev/ user:

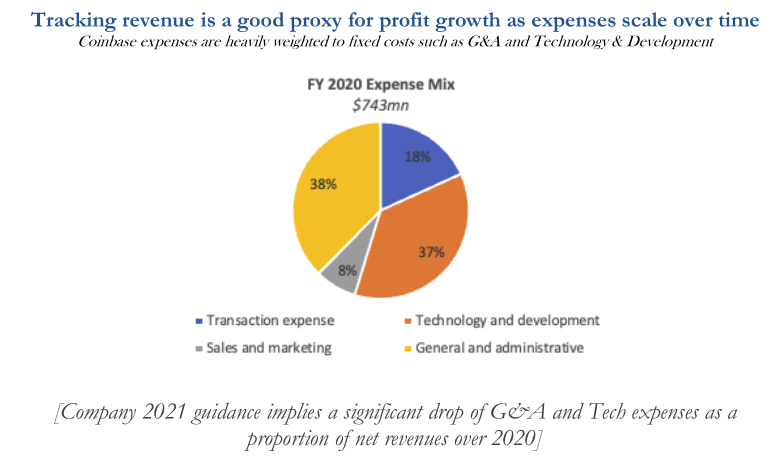

8/ Expense mix tilted heavily to fixed costs such as G&A and Technology & Development so operating leverage to revenue growth is very high:

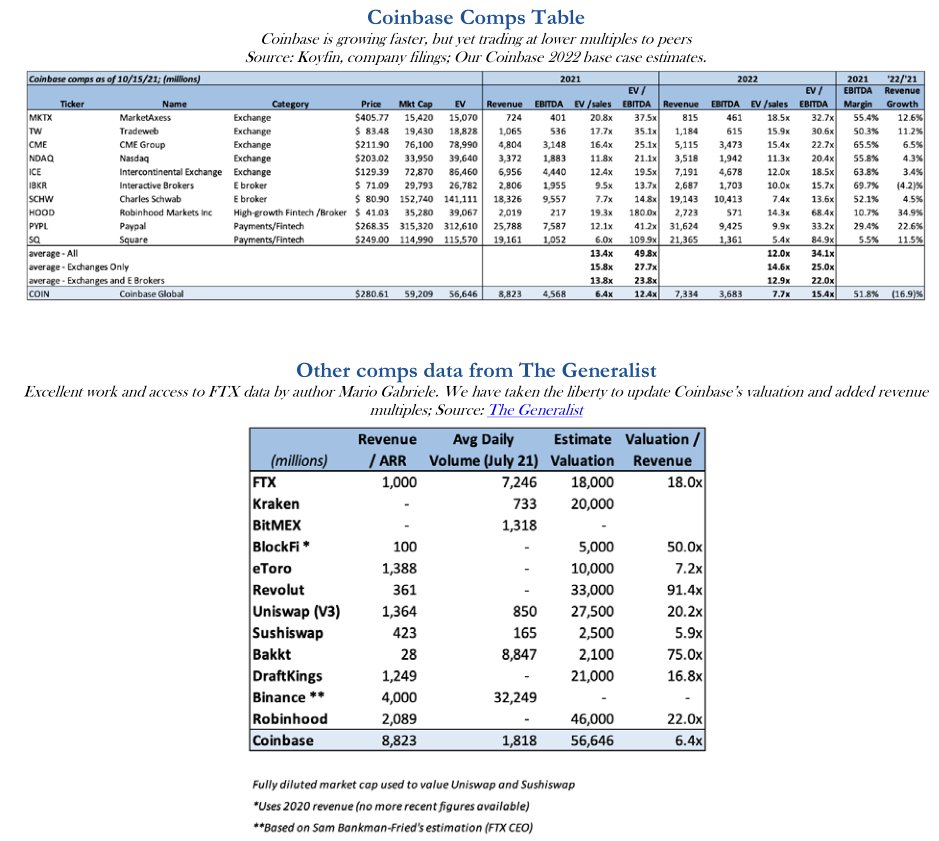

9/ Looking at comps, $COIN clearly cheaper than peers despite higher growth:

• • •

Missing some Tweet in this thread? You can try to

force a refresh