It's hard to believe we started Intrinsic Investing 5 years ago. Sharing our thoughts on investing has greatly improved our own thinking, forced us to better understand our own ideas and triggered excellent feedback from other investors.

A thread of some of our top posts of 2021

A thread of some of our top posts of 2021

We started the year laying out our portfolio construction/position sizing framework in detail. intrinsicinvesting.com/2021/01/05/pos…

We looked at how business quality, not just paying a low price for a stock, is a form of "margin of safety". intrinsicinvesting.com/2021/01/13/the…

After calling out excessive speculation in some parts of the market early in the year, we also explained why it can be easy to learn the wrong lessons from the Dot Com crash. intrinsicinvesting.com/2021/03/05/don…

At Ensemble we pursue what might be called a "humanist" approach to investment research. Companies are just collections of people and in the end analysis, we are all just part of a natural ecosystem. intrinsicinvesting.com/2021/03/22/ant…

In June, we argued that investing in a high pressure economy, like the one we are in today, means investors need to focus on very different aspects of a business/industry than was most relevant during the low pressure economy of the prior decade. intrinsicinvesting.com/2021/06/11/inv…

It isn't just excessive valuations that investors should avoid, but even more importantly investors need to be able to identify when a company is engaging in unsustainable activities. intrinsicinvesting.com/2021/06/25/com…

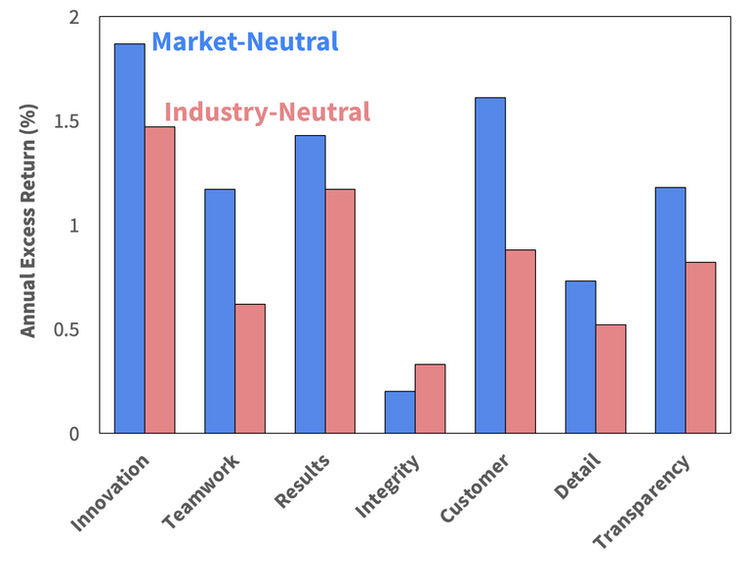

Ensemble is not an ESG investor, but we have long focused on the need for companies to generate value for all stakeholders. Yes it is the right thing to do, but it also is the best and most sustainable path to superior business performance. intrinsicinvesting.com/2021/07/22/ens…

While we're long term investors, with many stocks in our current portfolio owned for 5 to 10 years or more, we also think the concept of "buy and hold" can be misguided. intrinsicinvesting.com/2021/08/16/the…

Our five part series on how we approach forecasting corporate growth, blending together company level analysis with an understanding of the history of corporate growth, helped us clarify and formalize our own thinking. intrinsicinvesting.com/2021/10/04/for…

After you learn all the basics and you've been an investor for a decade or longer, effective pattern recognition because an immensely important part of successful investing. intrinsicinvesting.com/2021/10/27/15-…

We wish you all investment success as you seek to navigate another year of "unprecedented" economic and market dynamics! "May you live in interesting times" can be a curse, but it is also the source of much opportunity!

• • •

Missing some Tweet in this thread? You can try to

force a refresh