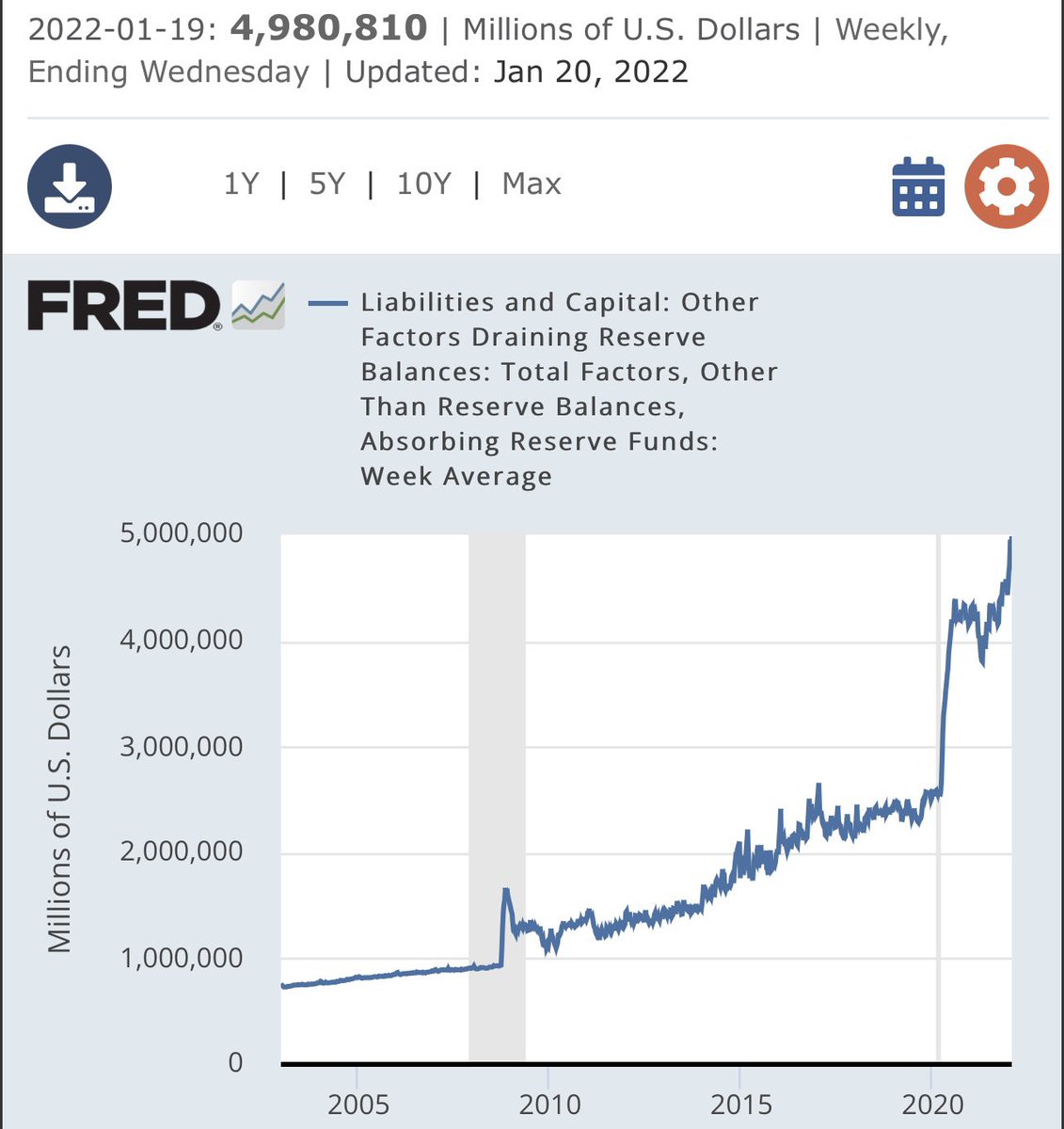

Reserves up to $4.98B as of the 19th

If the thesis is QT is causing the Sell Off… maybe look at Reserves. Market Liquidity is Up… Not Down.

+$129B WoW $XLF #Reflation

+$129B WoW $XLF #Reflation

Bank Liquidity has gonna Bananas… the Wall of Cash is coming…. So are Rate Hikes. $XLF #Reflation

Another $400B came in from Fed RRP.

Which is why $BAC came with another Preferred issue at 4.5%.

Which is why $BAC came with another Preferred issue at 4.5%.

• • •

Missing some Tweet in this thread? You can try to

force a refresh