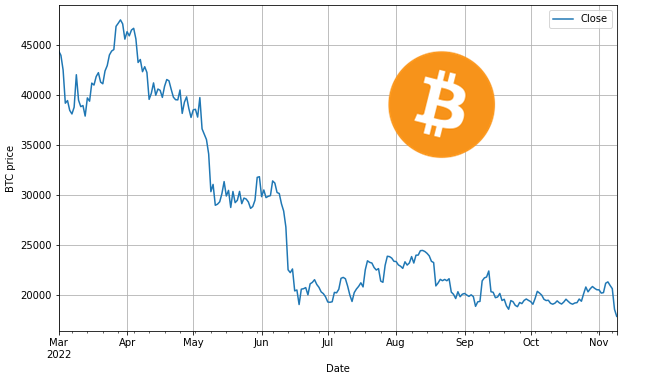

Is the #Bitcoin price a stationary times series? 🤔

Check 👇 how to find it out!

#DataScience #MachineLearning

Check 👇 how to find it out!

#DataScience #MachineLearning

We know that stationary means that the mean and variance of the time series data do not vary across time.

To be sure of that we can perform the Augmented Dickey-Fuller test.

To be sure of that we can perform the Augmented Dickey-Fuller test.

If you are familiar with #statistics here you have the hypotheses for this test:

H0️⃣ (Null hypothesis) = Time series non-stationary

H1️⃣ (Alternative hypothesis) = Time series is stationary

After the test, we will pay attention to the "p-value".

H0️⃣ (Null hypothesis) = Time series non-stationary

H1️⃣ (Alternative hypothesis) = Time series is stationary

After the test, we will pay attention to the "p-value".

This is how to perform the test in 🐍 #Python

You can import it from the statsmodels library.

If you don't have it in your environment, you can get it using "pip install statsmodels"

You can import it from the statsmodels library.

If you don't have it in your environment, you can get it using "pip install statsmodels"

We get lots of numbers out of this test, but which one should we care about?

We need to compare the second number, which corresponds to the p-value (0.5093) with our significance level α. This is generally set to 0.05.

We need to compare the second number, which corresponds to the p-value (0.5093) with our significance level α. This is generally set to 0.05.

We will have two scenarios:

1️⃣ p-value > 0.05 : we fail to reject the null hypothesis, which means that our time series is non-stationary.

2️⃣ p-value < 0.05 : we reject the null hypothesis, which for us means that our time series can be considered stationary.

1️⃣ p-value > 0.05 : we fail to reject the null hypothesis, which means that our time series is non-stationary.

2️⃣ p-value < 0.05 : we reject the null hypothesis, which for us means that our time series can be considered stationary.

In our case, the p-value is 0.5093.

It is greater than α = 0.05 → our time series data is non-stationary... 😢

It is greater than α = 0.05 → our time series data is non-stationary... 😢

What if we do the same but with the price returns instead of with the price? 🤔

We can calculate the returns as the percentage change.

We can calculate the returns as the percentage change.

This time the p-value is 0.0.

Which is lower than α = 0.05 → our time series data is stationary! 🥳

Which is lower than α = 0.05 → our time series data is stationary! 🥳

This means that we can use an ARMA model to forecast the returns.

Also, we can use an ARIMA model to forecast the prices if we use d=1.

Also, we can use an ARIMA model to forecast the prices if we use d=1.

https://twitter.com/daansan_ml/status/1590319971287998465?s=20&t=H6PTmUsrOM3MvRMhMyz1kw

Enough for today...

Follow me on @daansan_ml if you don't want to miss out!

Please support my content with a Retweet & Like on the first tweet of this thread.

Thanks!😉

Follow me on @daansan_ml if you don't want to miss out!

Please support my content with a Retweet & Like on the first tweet of this thread.

Thanks!😉

https://twitter.com/daansan_ml/status/1590688675821629440?s=20&t=CuS14-mkP14BSqn_dvYYlw

• • •

Missing some Tweet in this thread? You can try to

force a refresh