Extracts from the investor presentation by the company for March 2021

Extracts from the investor presentation by the company for March 2021

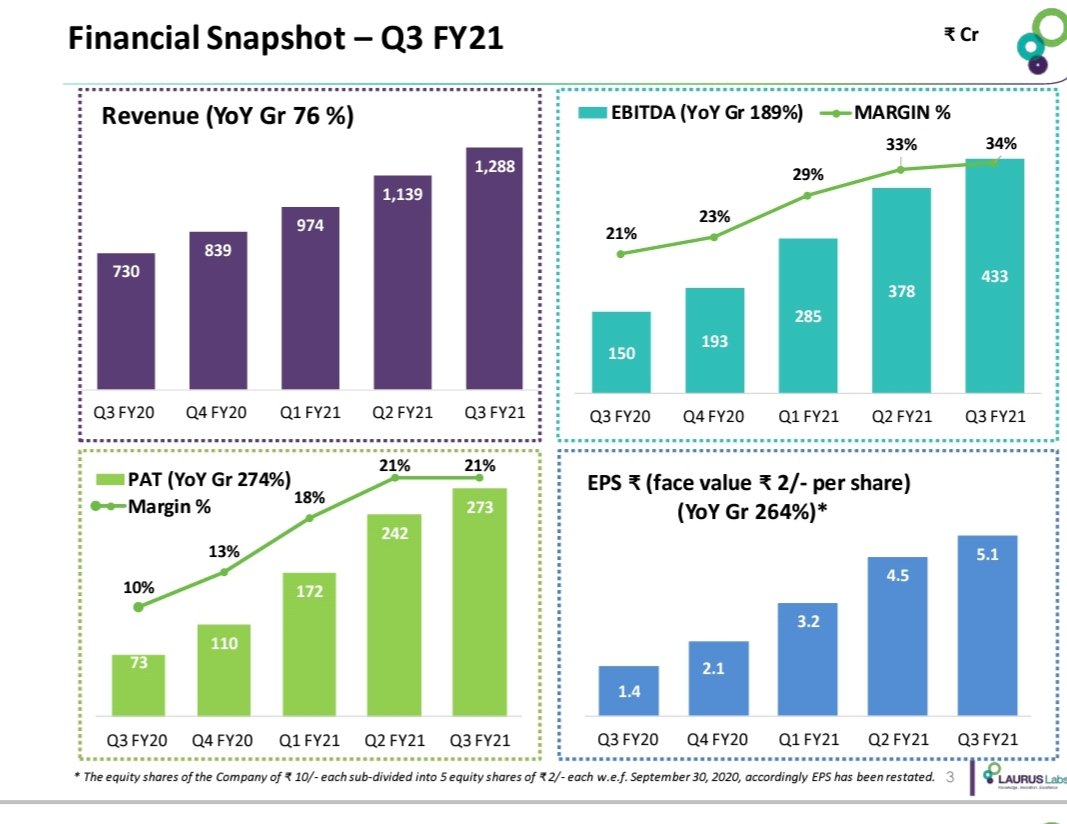

#lauruslabs

#lauruslabs

#lauruslabs 396

#lauruslabs 396

Revenue HLs

Revenue HLs

Formulations

Formulations

API Business

API Business

Airtel Business rev up by 9.2% yoy back of strong demand for connectivity and solutions

Airtel Business rev up by 9.2% yoy back of strong demand for connectivity and solutions 3 horizon strategy

3 horizon strategy

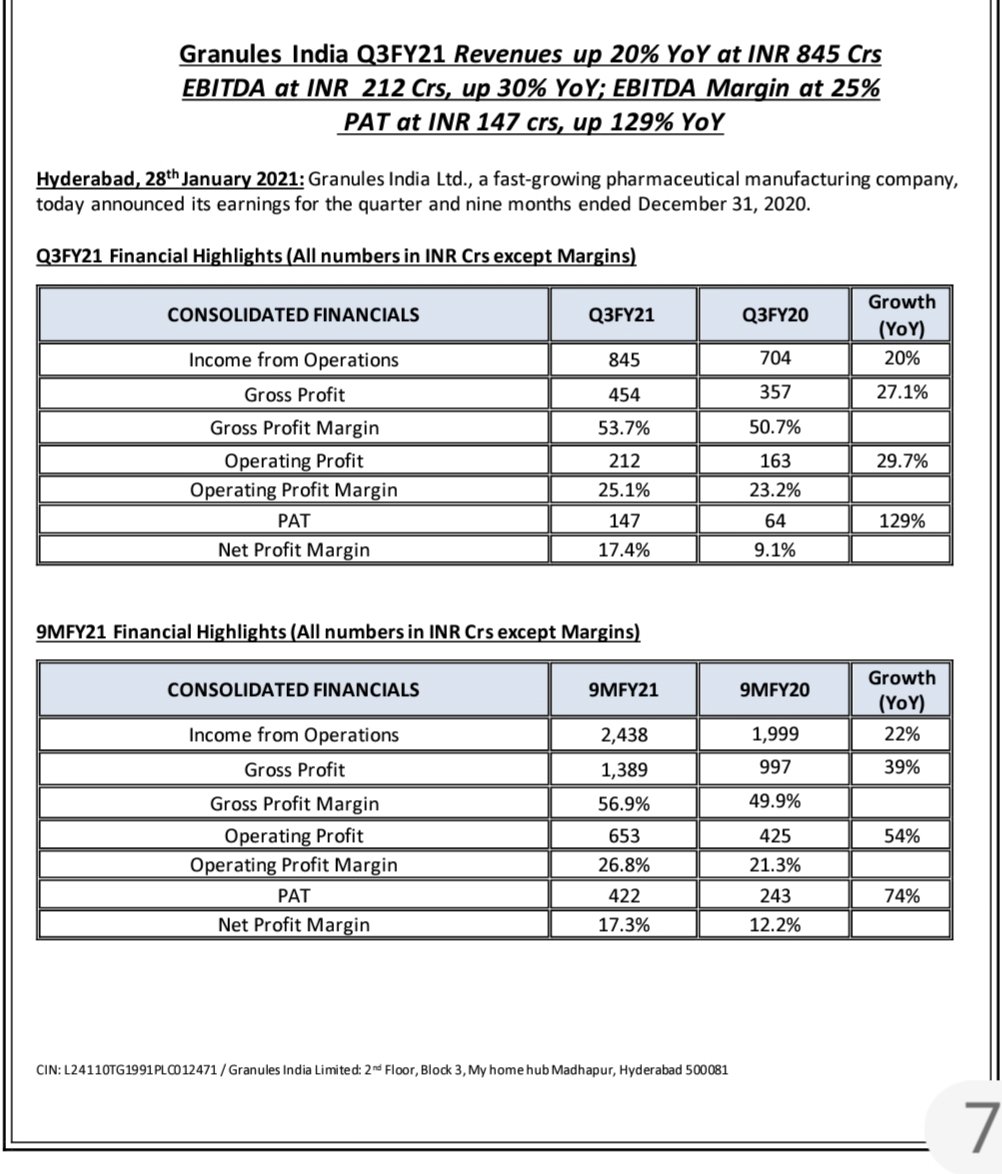

Generic APIs

Generic APIs EBITDA up 29.7% yoy, +190 bps margin expansion yoy on changing product mix with higher contribution from FD and PFI , improved operational efficiencies from higher capacity utilization

EBITDA up 29.7% yoy, +190 bps margin expansion yoy on changing product mix with higher contribution from FD and PFI , improved operational efficiencies from higher capacity utilization

Popular segment sales down 6.7%, led by decline 5.7% in priority states Increased consumer prices, unfav state mix contributed to decline

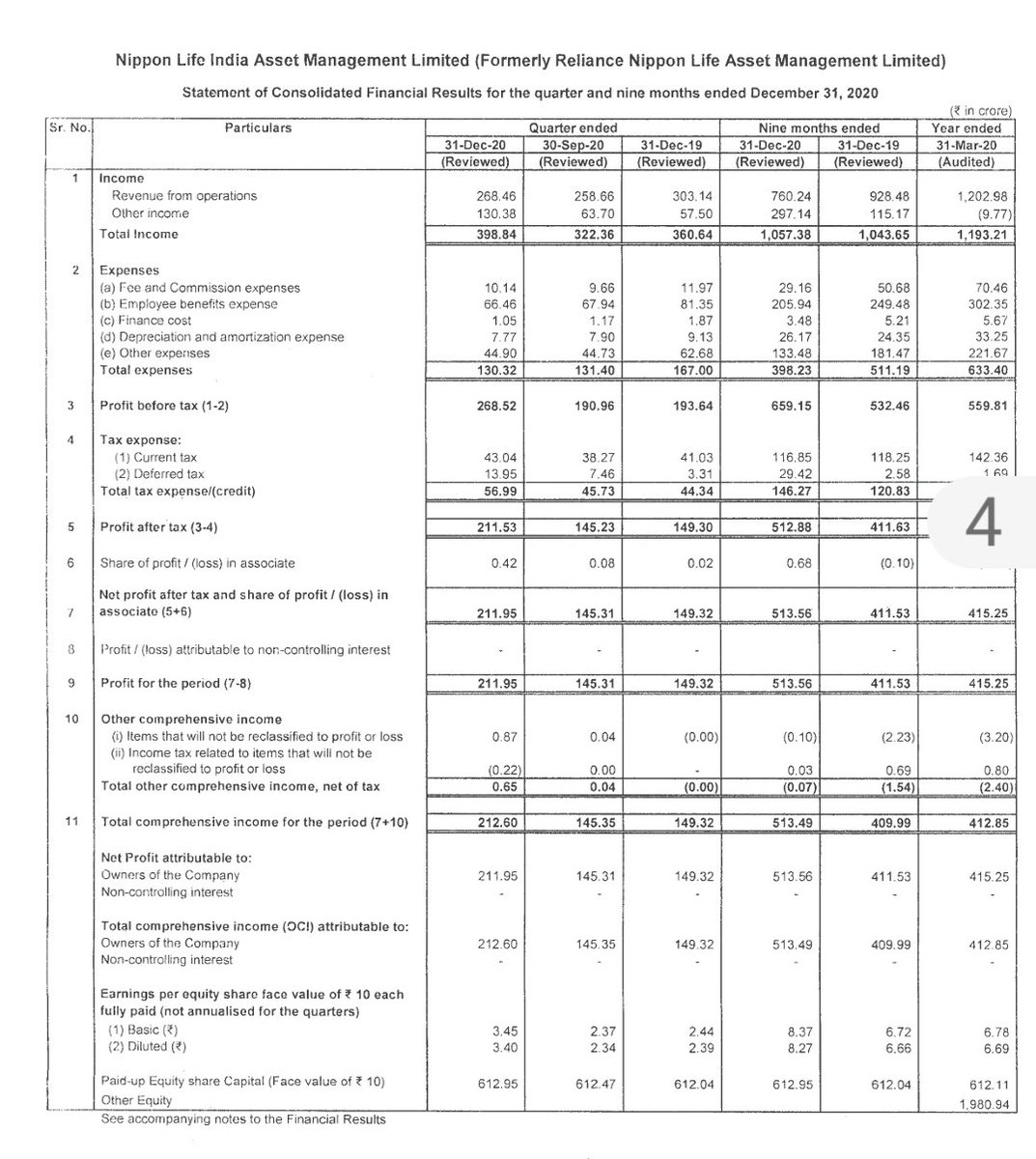

Popular segment sales down 6.7%, led by decline 5.7% in priority states Increased consumer prices, unfav state mix contributed to decline Retail assets 26% to NIMF's AUM

Retail assets 26% to NIMF's AUM 50 % mkt share in structural steel tubes 9mfy21,sales vol CAGR 27% fy11-20

50 % mkt share in structural steel tubes 9mfy21,sales vol CAGR 27% fy11-20 Wires&cables

Wires&cables R&D expenses INR Mn

R&D expenses INR Mn

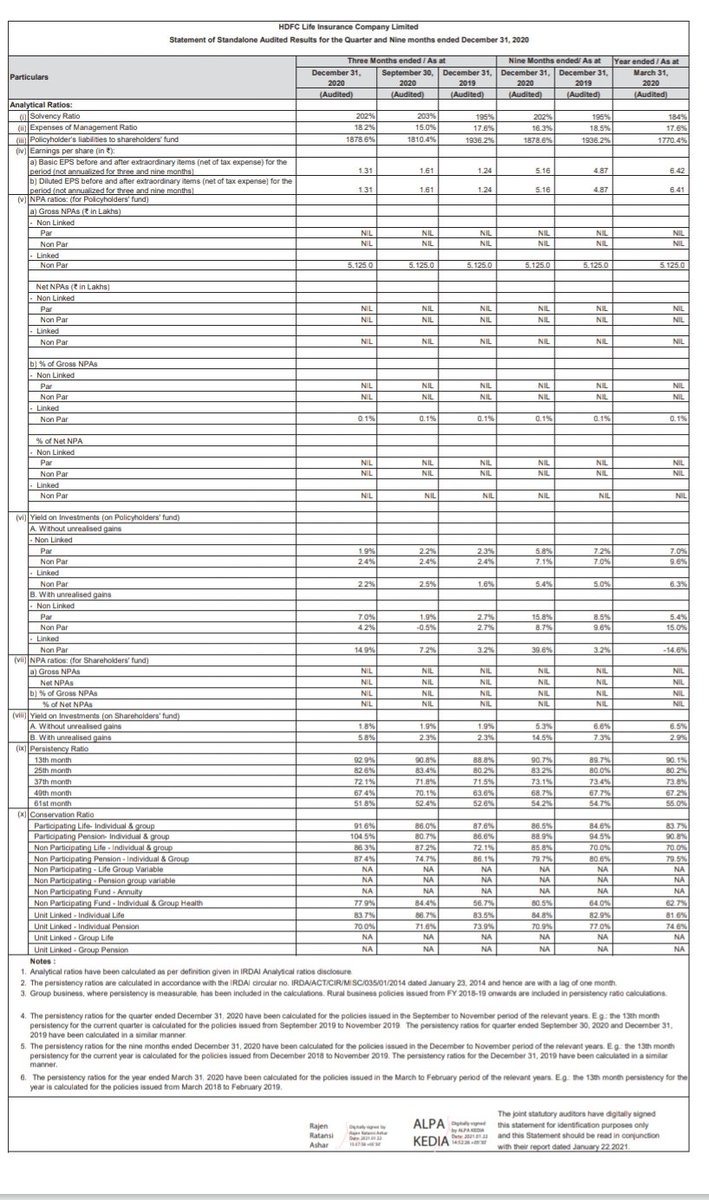

17% growth in Protection (Indl) and 42% growth in Annuity in APE terms

17% growth in Protection (Indl) and 42% growth in Annuity in APE terms

#Q3investorpresentations

#Q3investorpresentations