I'm at the @AnnualReviews/@CFAResearchFndn /@MIT/@nyuniversity ten year review of financial economics since the financial crisis. Taking notes on twitter, if you're here say hi!

"Shadow and standard banking are symbiotic. You kill one, kill the other.

A long standing, large, and permanent transition has taken place.

The panic of 2007-8 showed how the system can morph, but in a longer time horizon than we usually think of."

Gary Gordon @YaleSOM

A long standing, large, and permanent transition has taken place.

The panic of 2007-8 showed how the system can morph, but in a longer time horizon than we usually think of."

Gary Gordon @YaleSOM

Allegations against loan loss reserve accounting:

- too little accrual in good times

- too much in bad times

- procyclical effects

Pecipitated shift to expected loan reserve model.

This front-loads credit loss. Direct hit to income. Likely procyclical.

Ryan @nyuniversity

- too little accrual in good times

- too much in bad times

- procyclical effects

Pecipitated shift to expected loan reserve model.

This front-loads credit loss. Direct hit to income. Likely procyclical.

Ryan @nyuniversity

"If you think banks lend too risky, loan-level disclosure is the appropriate regulatory action, not accounting changes."

Ryan @nyuniversity

Ryan @nyuniversity

- Dodd frank has boosted resiliency but also regulatory burden.

- Diminishing returns to regulation with adequately self insurance.

- Some aspects not cost effective.

- Considerable scope remains to strengthen financial system.

Kim Schoenholtz @nyuniversity

- Diminishing returns to regulation with adequately self insurance.

- Some aspects not cost effective.

- Considerable scope remains to strengthen financial system.

Kim Schoenholtz @nyuniversity

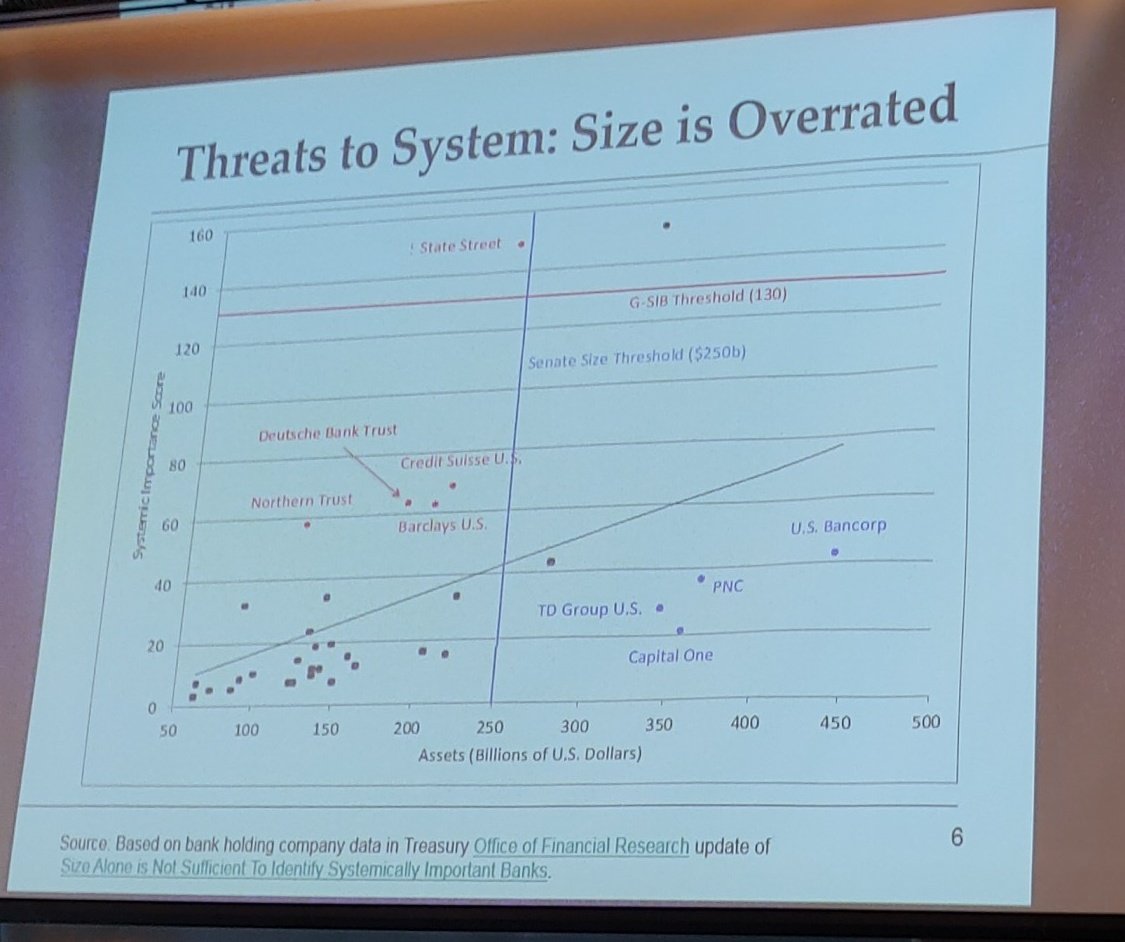

The $250B balance sheet size cutoff for SIFIs misses a lot of systemic risk (esp. Asset managers).

Kim Schoenholtz

+ cc @colinmclean

Kim Schoenholtz

+ cc @colinmclean

Regulatory conclusions (Kim Schoenholtz)

Recent actions overlook a number of opportunities to improve oversight.

Ex:

- UK has 3 regulators

- US has 100+

Operational risk has increased through shift to central clearing. Disclosure needed. And contingency plans.

Recent actions overlook a number of opportunities to improve oversight.

Ex:

- UK has 3 regulators

- US has 100+

Operational risk has increased through shift to central clearing. Disclosure needed. And contingency plans.

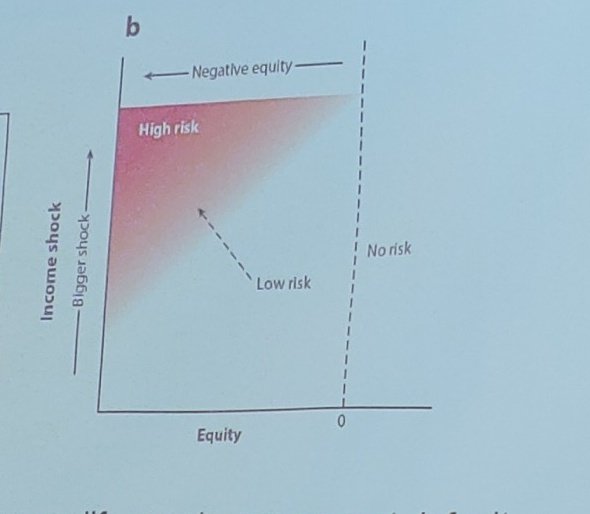

"Defaulting on debt takes low initial equity and an adverse life event."

Modified double trigger model from Foote @BostonFed

Modified double trigger model from Foote @BostonFed

"any anti-foreclosure program is going to have an imperfect information problem."

Chris Foote @BostonFed

Chris Foote @BostonFed

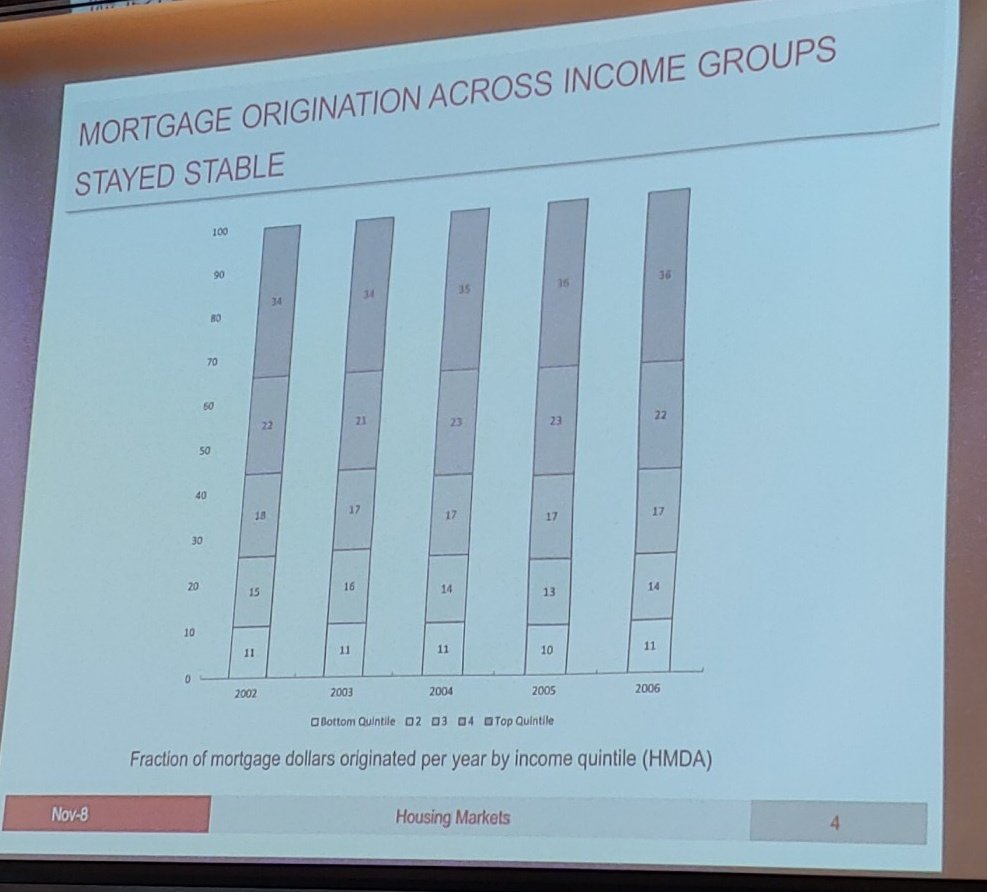

It wasn't a sub-prime crisis.

"There was no unilateral shift of credit allocation towards marginal or sub-prime borrowers."

Antoinette Schoar @MIT

"There was no unilateral shift of credit allocation towards marginal or sub-prime borrowers."

Antoinette Schoar @MIT

The fraction of dollars flowing to sub-prime borrowers stayed constant in the lead up to the crisis.

Antoinette Schoar (cont)

Antoinette Schoar (cont)

Accepted wisdom: "loans that should never have been written caused the crisis"

If that were real, low income homeownership would have expanded.

Didn't happen. Look at the bottom line. Lowest income quintile homeownership fell and fell further all decade.

Schoar (cont)

If that were real, low income homeownership would have expanded.

Didn't happen. Look at the bottom line. Lowest income quintile homeownership fell and fell further all decade.

Schoar (cont)

Wow. Borrowers with FICO scores above 660 held 61% of delinquent mortgages in 2006.

Schoar (cont) #FinancialCrisisReview enfuego.

Schoar (cont) #FinancialCrisisReview enfuego.

#FinancialCrisisReview is back after a break. Andrew Lo interviews Geithner and other goodies coming up.

Now Deborah Lucas on the consequences of bailouts.

"Economists don't spend a lot of time looking at the cost of government actions."

Now Deborah Lucas on the consequences of bailouts.

"Economists don't spend a lot of time looking at the cost of government actions."

"How did it come to be that a AAA company with a trillion dollar balance sheet (AIG) couldn't make collateral payments?

Misplaced faith in large institutions."

- Bob Armstrong, President and CEO of AIG a/o February 2010.

Misplaced faith in large institutions."

- Bob Armstrong, President and CEO of AIG a/o February 2010.

Armstrong cont: "We need more specialized, simpler Institutions in order to improve oversight."

Error earlier. Peter Hancock was speaking, and the former head of AIG. @rbrtrmstrng is moderator.

"I had made the naive assumption when I joined AIG that my counterparty was the government."

Wasn't just one. A sustainable capital structure needed to evolve through cooperation amid chaos. Hancock et al modeled a $13B "peace dividend" to bring parties to. The table.

Wasn't just one. A sustainable capital structure needed to evolve through cooperation amid chaos. Hancock et al modeled a $13B "peace dividend" to bring parties to. The table.

"I'm not sure current risk frameworks look enough at legal enforceability, as opposed to credit risk."

Peter Hancock, former CEO of AIG.

Peter Hancock, former CEO of AIG.

"The cost of crisis protection didn't really rise until the government made the decision to intervene."

- Myron Scholes

- Myron Scholes

Three lessons learned from the financial crisis, per Myron Scholes:

- Do not data mine. No defaults before doesn't mean none coming.

- Correlation structures are not constant.

- There are cheaters out there.

- Do not data mine. No defaults before doesn't mean none coming.

- Correlation structures are not constant.

- There are cheaters out there.

"The scope of the safety net (for making things safer in a crisis) was very narrow. And it was hard to understand the implications of that."

- Tim Geithner

- Tim Geithner

"All of the changes in the structure of the system made it more stable in a broader set of shocks, but also harder to stabilize."

Geithner (cont)

Geithner (cont)

"All the things that conspire against action - complacency, the Minsky stuff, capture - make it really hard to limit a system already running with too much leverage....

You have to design a system that works even if oversight isn't prescient."

- Tim Geithner

You have to design a system that works even if oversight isn't prescient."

- Tim Geithner

I'll never do justice to Tim Geithner's body language.

But picture this. Andrew Lo asks what dealing with the crisis was like for him physically.

Three, then five second pause....

"It was dark, hard, time."

But picture this. Andrew Lo asks what dealing with the crisis was like for him physically.

Three, then five second pause....

"It was dark, hard, time."