,

15 tweets,

9 min read

Read on Twitter

1/ Factor Momentum Everywhere (Gupta, Kelly)

"Time series factor momentum benefits investment strategies that employ traditional momentum, value, and other factors. The momentum phenomenon is driven in large part by persistence in common return factors."

papers.ssrn.com/sol3/papers.cf…

"Time series factor momentum benefits investment strategies that employ traditional momentum, value, and other factors. The momentum phenomenon is driven in large part by persistence in common return factors."

papers.ssrn.com/sol3/papers.cf…

2/ AQR starts with a 65 factors defined in a similar fashion as HML. (This paper doesn't present results for a universe containing mid and large caps only, though it will later show the results with hypothetical transaction costs included.)

3/ The authors then show that factors' past returns have tended to predict future returns.

Returns for factors are even "stickier" than returns of the market itself, so if trend following works on stock indices, it should theoretically work for factors as well.

Returns for factors are even "stickier" than returns of the market itself, so if trend following works on stock indices, it should theoretically work for factors as well.

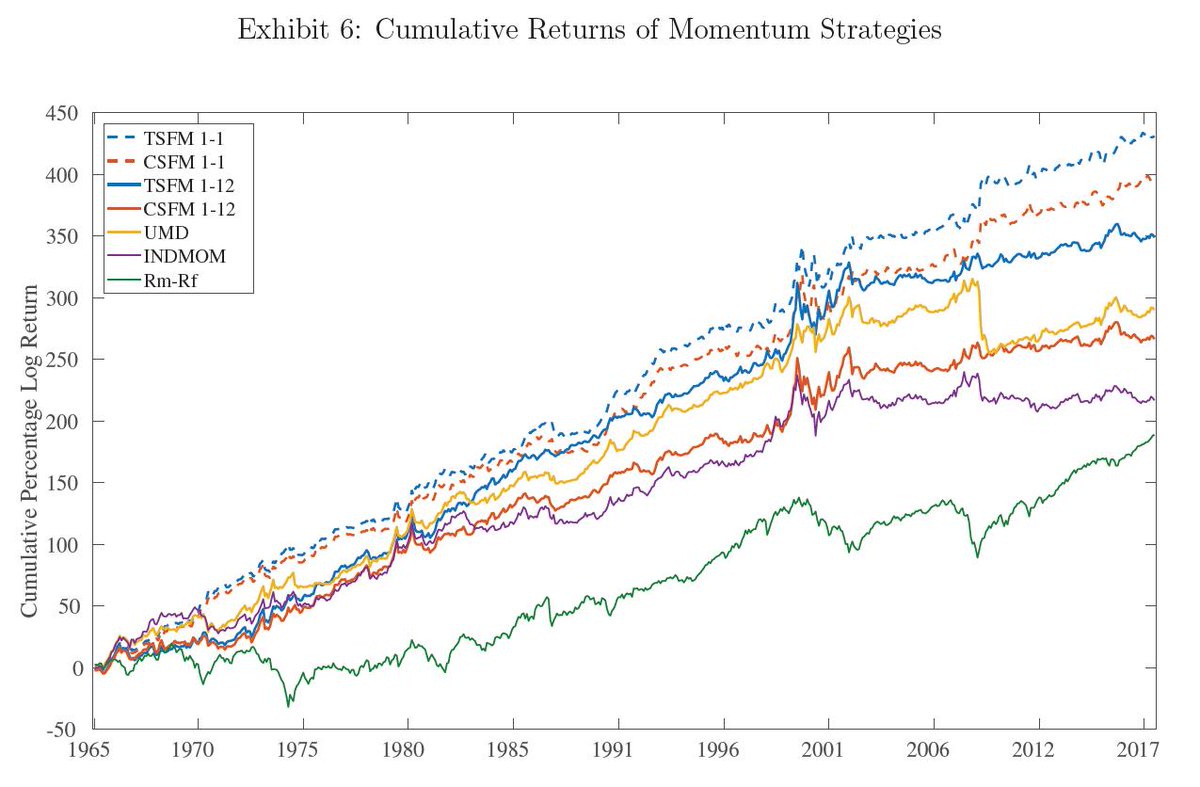

4/ The authors then build a time-series momentum strategy for factors.

Note that it scales factors by recent returns divided by longer-term volatility - a more granular measure than using the sign of the past year's excess returns. Other papers may use different methodologies.

Note that it scales factors by recent returns divided by longer-term volatility - a more granular measure than using the sign of the past year's excess returns. Other papers may use different methodologies.

5/ Time series scaled factors indeed have alpha over the raw ("buy-and-hold") forms of the same factors.

This is similar to what happens when trend following is applied to more traditional assets.

This is similar to what happens when trend following is applied to more traditional assets.

6/ Time-series momentum on factors is strongest using a one-month formation period with no skip-month, so (unlike in stocks), there's no short-term mean reversion.

It also works, though not quite as well, with formation periods of up to five years.

It also works, though not quite as well, with formation periods of up to five years.

7/ The authors also build a cross-sectional factor momentum strategy.

It's similar to the time-series/scaling version just discussed but is always long half of the factors and short the other half. The time-series type, in contrast, can be more long than short and vice versa.

It's similar to the time-series/scaling version just discussed but is always long half of the factors and short the other half. The time-series type, in contrast, can be more long than short and vice versa.

8/ Time-series/scaling and cross-sectional versions are highly correlated.

Because factor momentum has no short-term or long-term reversals, the one-month and long-term versions have low correlations to UMD.

All versions are negatively correlated to short-term reversal.

Because factor momentum has no short-term or long-term reversals, the one-month and long-term versions have low correlations to UMD.

All versions are negatively correlated to short-term reversal.

9/ Time-series factor momentum survives controlling for UMD and industry momentum and gets stronger when controlling for short-term reversal.

Results for the cross-sectional version are weaker, and it has negative alpha after controlling for the time-series version.

Results for the cross-sectional version are weaker, and it has negative alpha after controlling for the time-series version.

10/ Looking backwards, we can see that the one-month and long-term versions of time-series factor momentum add value to a portfolio that already has FF's 5 factors and UMD in it.

The short-term version of factor momentum and short-term reversal in stocks play well together.

The short-term version of factor momentum and short-term reversal in stocks play well together.

11/ Because AQR's HML-Dev doesn't use stale data, it has a strongly negative correlation to UMD.

That tweak changes a lot for the portfolio: looking backward, we now want to own a lot of UMD and HML (and in equal quantities). Short- and long-term factor momentum still look good.

That tweak changes a lot for the portfolio: looking backward, we now want to own a lot of UMD and HML (and in equal quantities). Short- and long-term factor momentum still look good.

12/ This matters because short-term mean reversion's Sharpe ratio goes to zero after transaction costs. (Everything else survives AQR's estimate of transaction costs.)

We need mean-reverting value (like HML-Dev) if we want negative correlations to UMD and factor momentum.

We need mean-reverting value (like HML-Dev) if we want negative correlations to UMD and factor momentum.

13/ Factor returns are autocorrelated outside the U.S. as well.

This confirms the anecdotal observation that factor performance tends to have "regimes," both across time and geography. Value has been >> than momentum in Japan, and factor momentum would have picked up on that.

This confirms the anecdotal observation that factor performance tends to have "regimes," both across time and geography. Value has been >> than momentum in Japan, and factor momentum would have picked up on that.

14/ Results outside the U.S. are similar to those within the U.S.

* Time-series factor momentum > cross-sectional

* Short- and long-term time-series factor momentum is not explained by UMD

* Short-term mean reversion is valuable (but might not be implementable due to costs)

* Time-series factor momentum > cross-sectional

* Short- and long-term time-series factor momentum is not explained by UMD

* Short-term mean reversion is valuable (but might not be implementable due to costs)

15/ The U.S. and international versions of factor momentum also diversify each other.

AQR reproduced the results using six groups of factors (related to value, momentum, and quality).

In short, factor momentum diversifies traditional factors without the reversal issues of UMD.

AQR reproduced the results using six groups of factors (related to value, momentum, and quality).

In short, factor momentum diversifies traditional factors without the reversal issues of UMD.