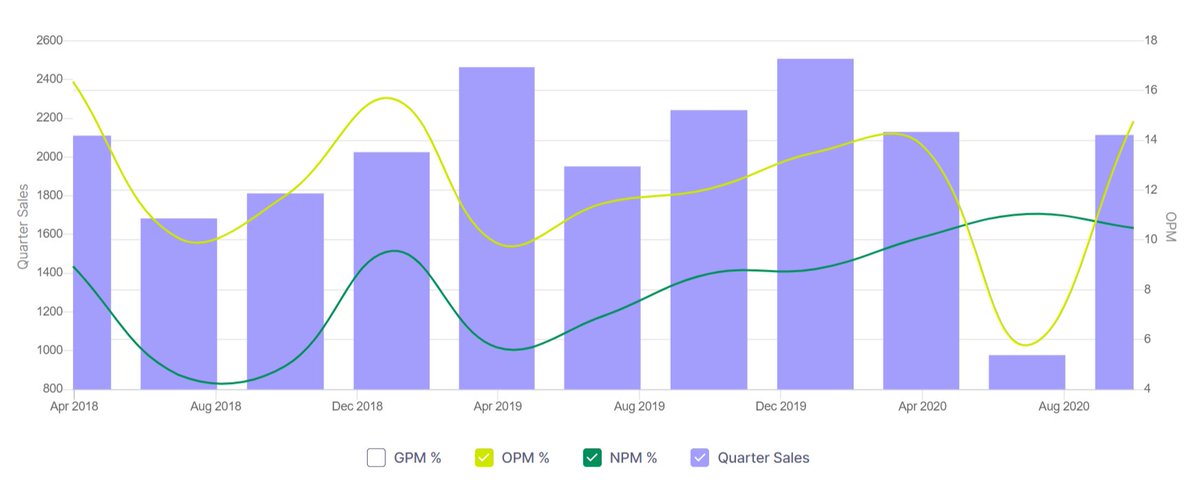

Sales trend :

Profit trend :

Profit growth rate :

Future EPS projection :

2025 EPS : 574rs/share

2030 EPS : 1360rs/share

Even at a median PE of 50x, 2030's CMP of 65k shows that one can expect 4X returns (14% CAGR) from here, but catching it at 11k pre-breakout would have given an additional +5% CAGR cushion.

2025 EPS : 574rs/share

2030 EPS : 1360rs/share

Even at a median PE of 50x, 2030's CMP of 65k shows that one can expect 4X returns (14% CAGR) from here, but catching it at 11k pre-breakout would have given an additional +5% CAGR cushion.

• • •

Missing some Tweet in this thread? You can try to

force a refresh