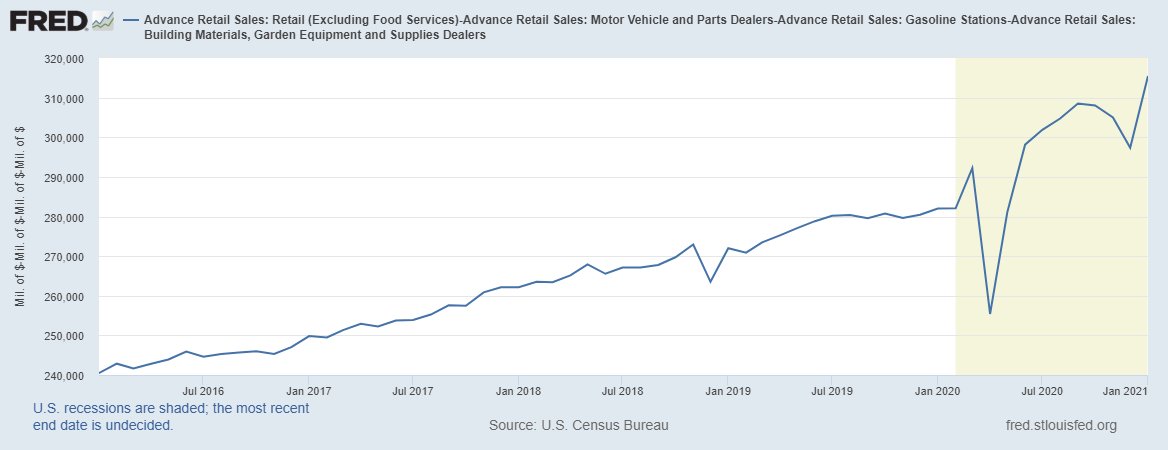

Core Retail Sales:

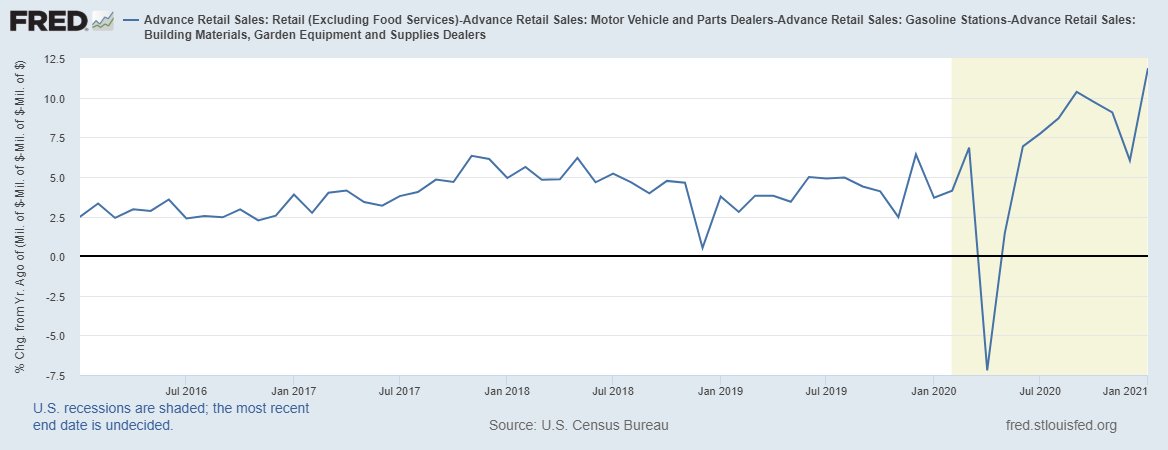

Core Retail Sales Year over Year:

"Real" Core Retail Sales:

"Real" Core Retail Sales Year over Year:

• • •

Missing some Tweet in this thread? You can try to

force a refresh