#copper

“The world’s top copper producer Chile saw output of the red metal fall for the tenth consecutive month in March, government statistics agency INE said on Friday.

Copper output fell 1.3% in March, to 491,720 tonnes, the agency said.”

“The world’s top copper producer Chile saw output of the red metal fall for the tenth consecutive month in March, government statistics agency INE said on Friday.

Copper output fell 1.3% in March, to 491,720 tonnes, the agency said.”

#copper

Chile also introducing new restrictions on movement and commerce following the Southern Hemisphere’s summer holidays. I expect their already bad Covid situation to get worse as they move into their Winter / European Summer.

Chile also introducing new restrictions on movement and commerce following the Southern Hemisphere’s summer holidays. I expect their already bad Covid situation to get worse as they move into their Winter / European Summer.

#copper

As I understand it most mines have had essential workers only on site - very few contractors allowed in. This means essential specialist work and maintenance has not been kept up to date with operating and mining plans.

As I understand it most mines have had essential workers only on site - very few contractors allowed in. This means essential specialist work and maintenance has not been kept up to date with operating and mining plans.

#copper

There are inevitable consequences: mines eat capital and if you do not feed them money production issues always occur. Usually with a 6 to 12 month lag.

There are inevitable consequences: mines eat capital and if you do not feed them money production issues always occur. Usually with a 6 to 12 month lag.

#copper

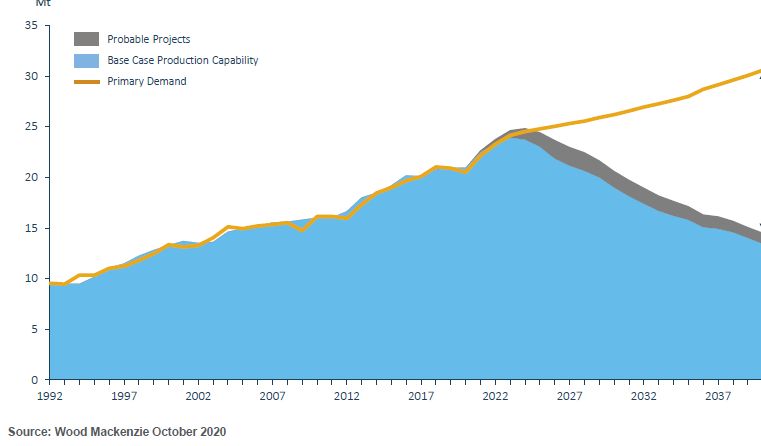

We are one major supply disruption away from an exponential move higher. This is now very likely in H2 In my view.

I remain bullish of copper in the short, medium and long term.

We are one major supply disruption away from an exponential move higher. This is now very likely in H2 In my view.

I remain bullish of copper in the short, medium and long term.

• • •

Missing some Tweet in this thread? You can try to

force a refresh