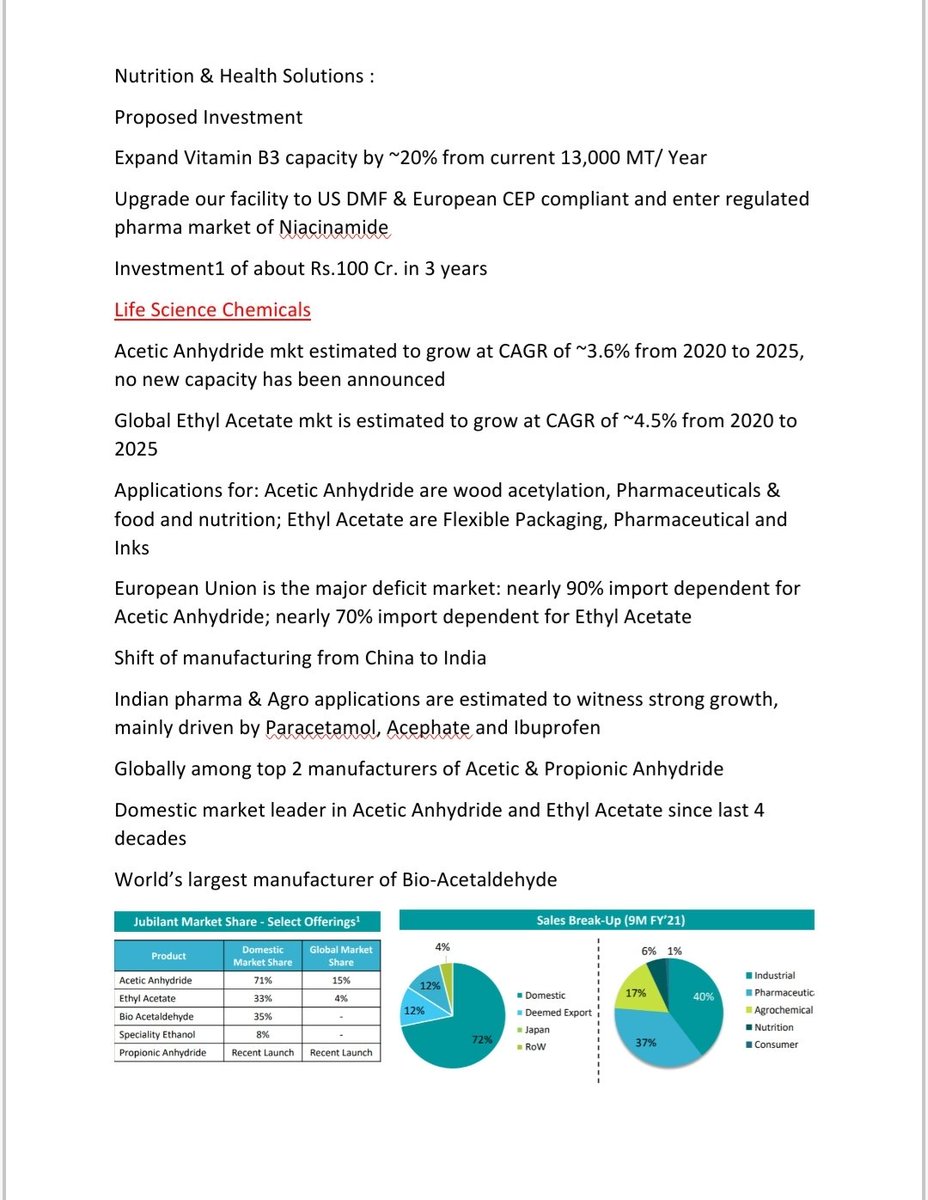

#jubilantingrevia

Extracts from the investor presentation by the company for March 2021

#Q4updates🐝

#Nifty #sensex #stocks #pharma #cdmo #API #specialitychemicals

Extracts from the investor presentation by the company for March 2021

#Q4updates🐝

#Nifty #sensex #stocks #pharma #cdmo #API #specialitychemicals

Extracts from the investor presentation by the company for March 2021

#Q4updates🐝

#jubilantingrevia

Unroll

@threadreaderapp

Compile

@threader_app

#Q4updates🐝

#jubilantingrevia

Unroll

@threadreaderapp

Compile

@threader_app

• • •

Missing some Tweet in this thread? You can try to

force a refresh