Hey— just checking:

Has *anyone* apologized for tweeting misinformation {see thread} about that crash that the NTSB investigated (where they verified that Elon’s tweet was correct and Autopilot was not at fault)?

Has *anyone* apologized for tweeting misinformation {see thread} about that crash that the NTSB investigated (where they verified that Elon’s tweet was correct and Autopilot was not at fault)?

In Tommy’s $TSLA cash-tagged tweet, he said it “was autopilot all the way.”

Alex said no one was in the driver seat, “because Tesla did not implement a camera-based Driver Monitoring System.”

Russ described it as “a 21st century riddle: A car crashes, killing both occupants — but not the driver.“

Ross and Glenn agreed that autopilot was engaged one second before impact.

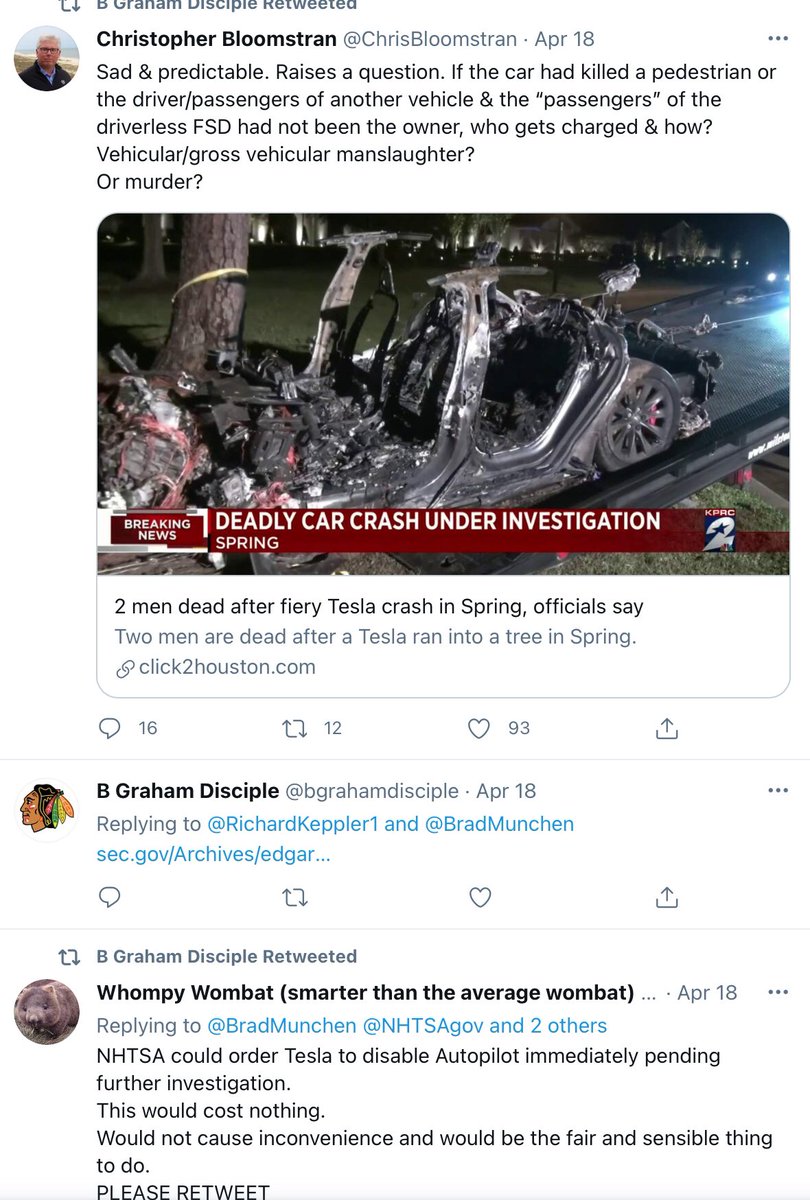

Brad and Billy... well— read it yourself.

Chris and Keef were ready to convict Autopilot without an investigation.

What excellent jurors they would make. 😏

What excellent jurors they would make. 😏

Linette reported that “there was no one in the driver’s seat” and that “men died bc @elonmusk wants to charge people $10K for fancy cruise control”.

TESLAcharts tweeted that “there was nobody in the driver’s seat” “and the car drove itself into a tree and caught fire”.

Mark and Roger joked that Elon was personally responsible for the crash.

Jake sent several unhelpful tweets and posted a video that can only be described as “helpful” to someone wishing to know how to defeat Tesla’s multi-layered driver-awareness monitoring systems.

When I tweeted about the irony of the Consumer Reports safety system defeat tutorial video (that CR accused Tesla of being irresponsible while themselves employing remarkable ingenuity to act irresponsibly), here’s how Lora and Neal reacted/retweeted:

• • •

Missing some Tweet in this thread? You can try to

force a refresh