Global economic growth slowed at the end of 2021 amid rising COVID-19 infection rates linked to #Omicron. However, at 54.3, the Global PMI signals above-trend annualised quarterly global GDP growth of approx. 3.5%.

bit.ly/3F8Ar7j

bit.ly/3F8Ar7j

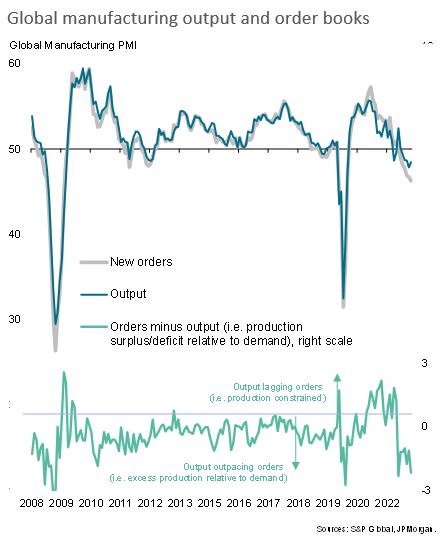

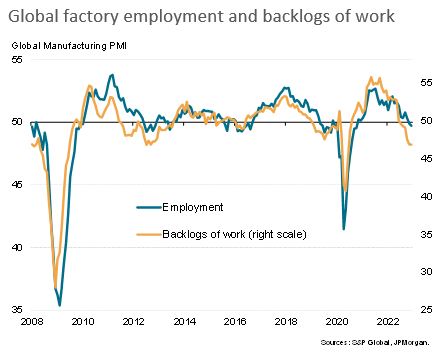

The December global PMI was pulled lower by a slowing of service sector growth, which slipped to the weakest for three months. In contrast, manufacturing growth accelerated to the fastest since July, albeit running behind that of services for the ninth month running.

The widening spread of the Omicron variant led to renewed restrictions (imposed and voluntary) on service sector activity in some economies during December. Manufacturers meanwhile reported that constraints on production had eased, though nonetheless remaining a significant drag.

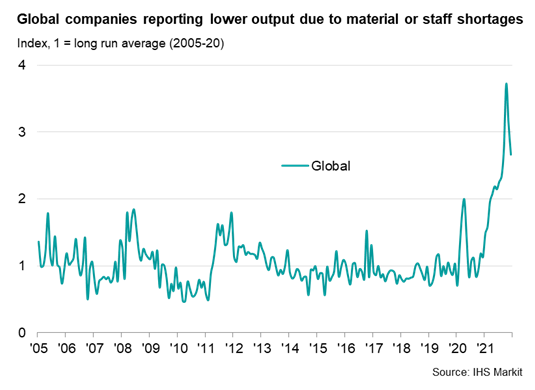

Measured globally, the number of companies reporting that output was constrained by raw material or staff shortages fell for a second month in December, down from an unprecedented peak in October, albeit still running almost three times higher than the long-run average.

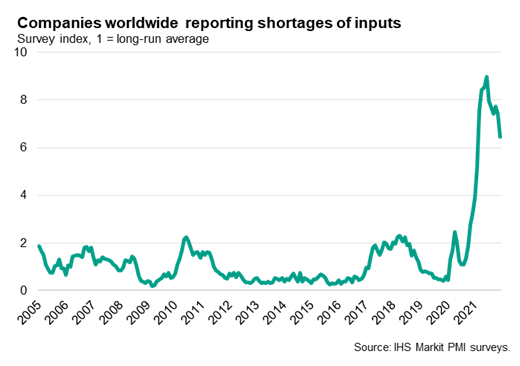

This alleviation of the global supply crunch is underscored by the PMI surveys also showing the number of companies reporting items in short supply to have fallen to the lowest since February, suggesting that shortages peaked back in June.

However, just as the supply crunch is alleviating, Omicron threatens further disruptions to economic activity - especially in the service sector, just at a time when the global demand recovery is fading sharply.

Read more at bit.ly/3F8Ar7j

Read more at bit.ly/3F8Ar7j

• • •

Missing some Tweet in this thread? You can try to

force a refresh